Assessing Array Digital Infrastructure (AD) Valuation As Analyst Targets Converge With Current Share Price

Array Digital Infrastructure, Inc. AD | 0.00 |

Event context and recent share performance

Array Digital Infrastructure (AD) has shown mixed short-term moves, with a 1-day return of about a 1% decline and a broadly flat week, while the month and past 3 months show modest positive returns.

At the latest share price of $49.30, recent pressure on the share price year to date contrasts with a very strong 1 year and multi year total shareholder return. This suggests sentiment has shifted from short term caution toward a longer term, more optimistic view of Array Digital Infrastructure’s prospects.

If the recent move in AD has you rethinking your watchlist, this could be a good moment to scan other opportunities in AI infrastructure and data centers using the 40 AI infrastructure stocks

With AD trading at $49.30, a value score of 1, and the current share price sitting close to analyst targets, it is fair to ask: is the stock still overlooked, or is the market already pricing in future growth?

Most Popular Narrative: 8.4% Undervalued

At $49.30, the most followed narrative pegs Array Digital Infrastructure’s fair value at about $53.83, setting up an interesting gap between story and market price.

The anticipated mid-2025 closing of the transaction with T-Mobile, subject to regulatory approval, is expected to provide UScellular with significant proceeds, which could impact earnings positively by paying down debt and potentially declaring special dividends. The expansion of UScellular's fiber program, having already expanded its footprint by 30% in the last three years, presents opportunities for future revenue growth as more addresses are delivered and internet penetration increases.

Want to see what sits behind that fair value gap? The narrative focuses on specific revenue paths, margin shifts, and a future earnings multiple that merits closer examination.

Result: Fair Value of $53.83 (UNDERVALUED)

However, this story can shift quickly if the T Mobile deal encounters regulatory delays or if competitive pressure continues to reduce service revenues and profitability.

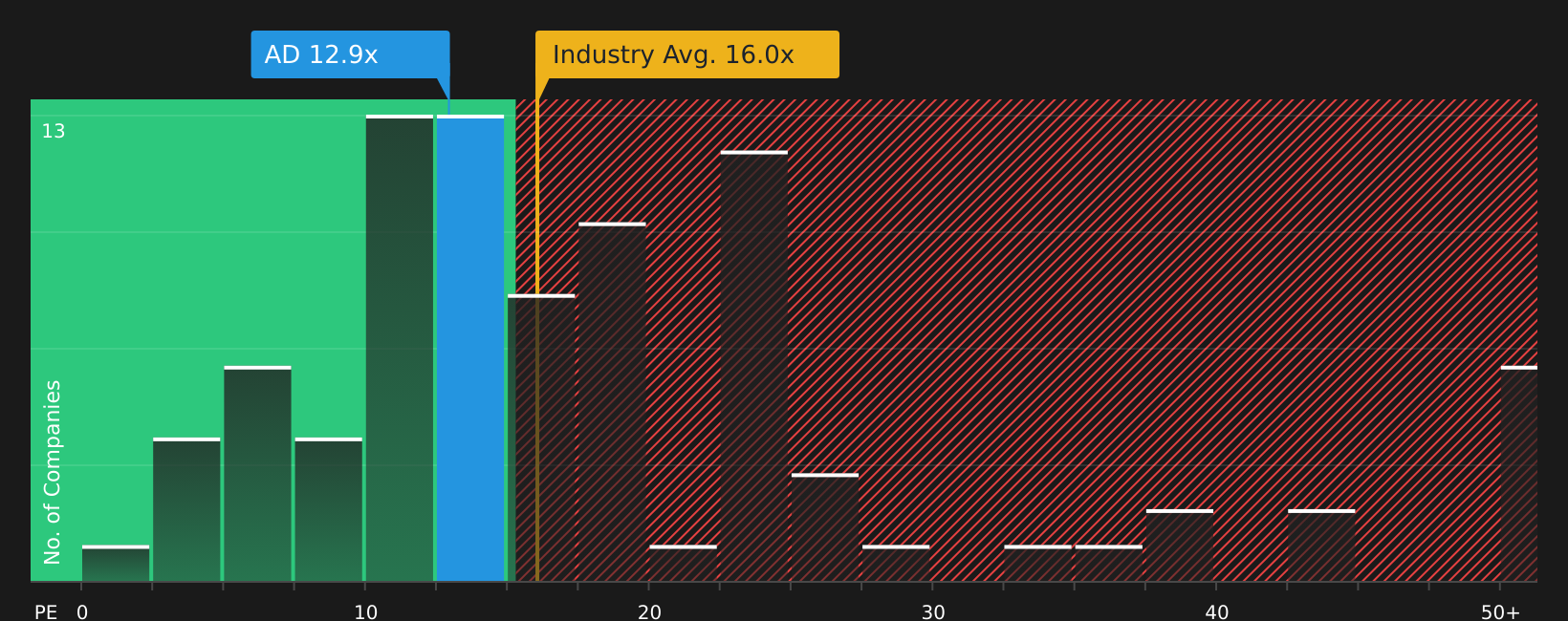

Another angle on valuation

Analysts see AD as about 8% undervalued at $49.30, but the current P/E of 25.1x tells a tougher story. It is richer than the global wireless telecom average of 16.3x and well above a fair ratio of 8.5x, which points to meaningful valuation risk if sentiment cools.

Next Steps

Uncertain whether this mix of potential risks and rewards suits your own comfort level and time horizon? Take a moment to review the numbers, compare them with your expectations, and then weigh the 1 key reward and 2 important warning signs

Looking for more investment ideas?

If AD no longer looks like the only stock worth your attention, broaden your watchlist now using focused screeners built around financial strength and income potential.

- Target stability first by checking companies in the 72 resilient stocks with low risk scores that score well on resilience and risk controls.

- Hunt for better value by reviewing the 51 high quality undervalued stocks that pair solid fundamentals with prices that still look reasonable.

- Put income on your radar by scanning the 12 dividend fortresses that aim to combine higher yields with sturdier business profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.