Assessing Assurant (AIZ) Valuation After Recent Momentum And Recurring Revenue Narrative

Assurant, Inc. AIZ | 224.01 224.01 | +0.78% 0.00% Pre |

Assurant stock: event driven snapshot

Assurant (AIZ) shares recently attracted investor attention after a period of steady trading, with the stock closing at $243.31 as the company reports annual revenue of $12.57b and net income of $848.8m.

That latest move in Assurant’s share price sits on top of a steady build in momentum, with a 90 day share price return of 8.47% and a 5 year total shareholder return of 107.08% pointing to meaningful long term value creation for holders.

If Assurant’s trend has you thinking about where else capital might work hard, you can broaden your search with our list of 22 top founder-led companies.

With Assurant trading at $243.31, sitting below an average analyst target of $259.33 and an intrinsic value estimate that suggests a wider discount, you have to ask: is this a genuine opening, or is the market already baking in future growth?

Most Popular Narrative: 6.2% Undervalued

Assurant’s most followed narrative sets a fair value of $259.33 against the last close of $243.31, framing a modest valuation gap that hinges on future earnings power and cash returns.

Growing preference for embedded insurance and "as-a-service" protection models, reflected in new and renewed B2B2C partnerships with leading OEMs, carriers, dealers, and financial institutions, boosts client retention and recurring premiums, further supporting revenue stability and net margin improvement.

Curious how this recurring revenue story translates into that fair value range? The narrative leans heavily on steady top line expansion, rising margins and a future earnings multiple that implies investors keep paying up for those cash flows. The full breakdown shows how these pieces fit together, and which assumptions really carry the model.

Result: Fair Value of $259.33 (UNDERVALUED)

However, the story could shift if regulatory pressure on lender placed insurance increases, or if bigger tech and insurtech players squeeze margins in mobile protection.

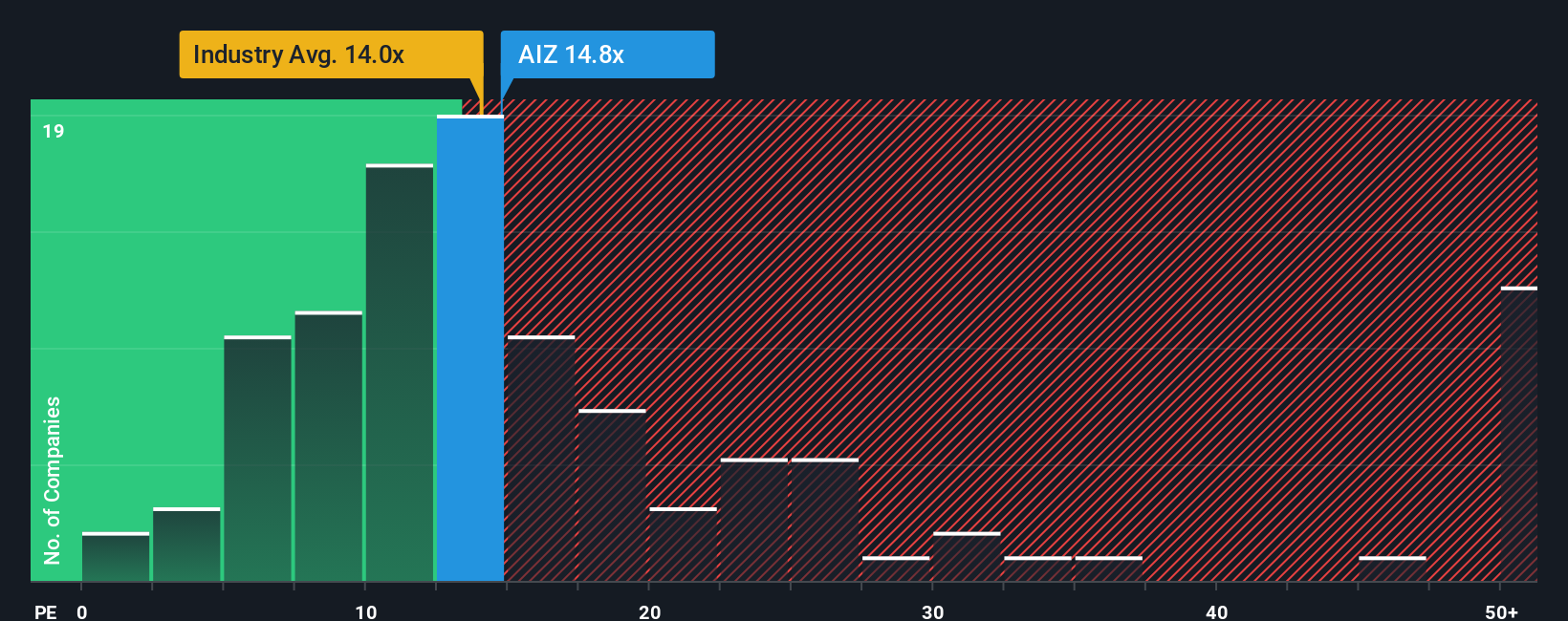

Another View: What The P/E Is Saying

The story looks different when you focus on the P/E. At 14.4x, Assurant trades above both the US Insurance industry at 12.9x and its peer group at 12.7x, yet sits slightly below a fair ratio of 14.9x. So is this a comfort zone or a valuation tightrope?

Build Your Own Assurant Narrative

If parts of this story do not line up with your own view, that is a feature not a flaw. You can stress test the numbers yourself, tweak the assumptions and Do it your way in under three minutes.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Assurant.

Looking for more investment ideas?

If this Assurant story has sparked ideas, do not stop here. Widen your opportunity set with a few curated lists that surface very different types of stocks.

- Go after value by scanning 53 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect what the businesses offer.

- Prioritize resilience by checking out 86 resilient stocks with low risk scores, focusing on companies that score well on stability and risk metrics.

- Hunt for under followed opportunities with our screener containing 24 high quality undiscovered gems, where quieter names might suit investors willing to do extra research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.