Assessing Aura Minerals (NasdaqGS:AUGO) Valuation After Growth Plans Highlighted In Recent Investor Presentation

Aura Minerals AUGO | 0.00 |

Aura Minerals (AUGO) put its growth plans in front of investors during a Renmark virtual non deal roadshow on May 25, outlining recent production gains, new assets and progress on development projects.

The Renmark roadshow comes after a mixed stretch for the stock, with a 1-day share price return of 1.83% and 7-day share price return of 6.46%. However, the 30-day share price return fell 5.95%, while a year-to-date share price return of 54.54% and a 1-year total shareholder return above 200% point to strong longer term momentum.

If this kind of move in a gold and copper producer has your attention, it might be a good time to widen your search with the 33 elite gold producer stocks

With Aura Minerals trading at $77.27 against an analyst price target of $101.34 and an estimated intrinsic value gap, the key consideration is whether this represents a potential buying opportunity or whether the market is already fully reflecting expectations for future growth.

Most Popular Narrative: 72.2% Overvalued

The most followed valuation narrative for Aura Minerals pegs fair value at $44.88 per share, which sits well below the latest close at $77.27. That gap rests on a specific growth blueprint.

The planned development of Era Dorada and either Matupa or Guatemala, with relatively contained initial capital requirements, positions the portfolio for multi-year volume growth. This may improve earnings durability and return on invested capital.

It is worth examining what earnings ramp, margin profile and valuation multiple are incorporated into that fair value estimate. The projections rely on ambitious volume assumptions and a richer profit mix. Investors may want to understand which growth path and profitability targets would need to be met for Aura to align with the $44.88 figure.

Result: Fair Value of $44.88 (OVERVALUED)

However, this overvalued view could be challenged if production ramp ups such as Borborema and efficiency gains at MSG materially lift earnings and cash generation versus current expectations.

Another View: Cash Flows Paint a Different Picture

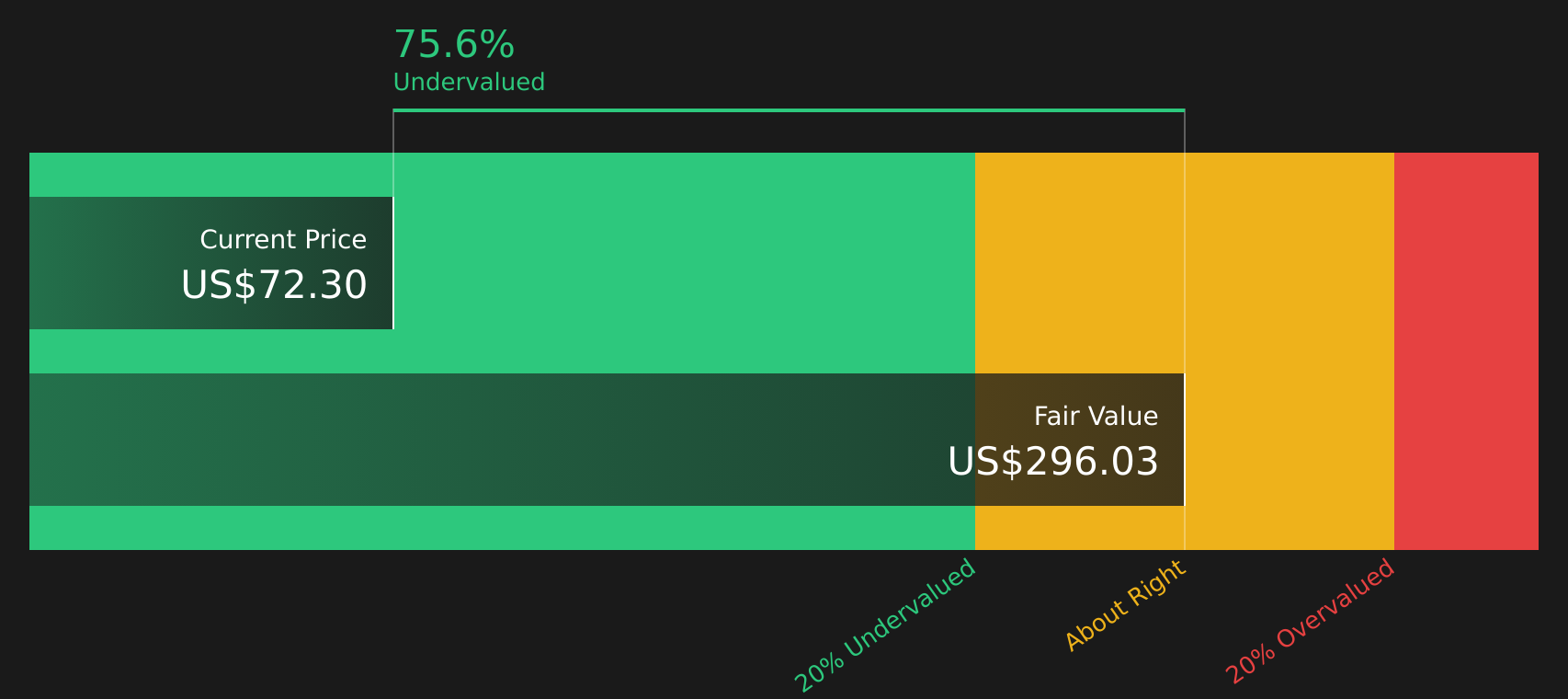

The narrative led with a fair value of $44.88 per share, which frames Aura Minerals as overvalued against the current $77.27 price. Yet Simply Wall St's own DCF model points the other way, with an estimate of future cash flow value at $295.94 per share, suggesting a very different risk reward trade off.

For anyone weighing which story to lean on, it is worth seeing how the cash flow assumptions stack up against the earnings based narrative, and what would need to change for the two views to converge: Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Aura Minerals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The split between overvaluation concerns and upside potential makes the story interesting, so review the key figures yourself and use the 3 key rewards and 4 important warning signs

Looking for more investment ideas?

If Aura Minerals has sparked fresh questions, do not stop here. Broaden your watchlist with other focused ideas that could help sharpen your overall portfolio decisions.

- Target dependable income by scanning companies we classify as 10 dividend fortresses that may appeal if you prioritise regular cash returns.

- Hunt for quality at a reasonable price through the 46 high quality undervalued stocks to spot stocks where fundamentals and valuation appear out of sync.

- Secure peace of mind by checking the 64 resilient stocks with low risk scores for companies that our models view as having more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.