Assessing Avista (AVA) Valuation As New Microgrid Project Highlights Its Energy Resilience Focus

Avista Corporation AVA | 0.00 |

Avista (AVA) is drawing fresh attention after Avista Utilities started operating a community-based microgrid at Spokane’s Dr. Martin Luther King Jr. Family Outreach Center. The project combines solar, battery storage, and natural gas to support energy resilience.

At a share price of $41.16, Avista has delivered a 6.30% year to date share price return, while the 1 year total shareholder return of 11.34% suggests interest has been building around its recent earnings, dividend affirmation and microgrid rollout.

If this kind of grid and resilience story interests you, it can be worth looking at other power and infrastructure stocks, starting with our 38 power grid technology and infrastructure stocks

With Avista trading close to the average analyst price target and an intrinsic value estimate that sits above the current share price, the key question is whether this steady utility stock is still mispriced or whether the market already reflects its future growth potential.

Most Popular Narrative: 3.8% Undervalued

With a fair value estimate of $42.80 set against Avista's last close at $41.16, the prevailing narrative sees modest upside supported by regulated growth and clean energy investment plans.

Robust, multi-year capital investment plans approaching $3 billion (2025 to 2029), with additional upside from grid expansion projects and new generation needs tied to large load requests, position Avista to earn regulated returns and drive long-term earnings expansion.

Want the full story behind that valuation gap? Revenue growth assumptions, margin shifts, and future earnings multiples all play a part. The projections are precise, not punchy guesses. The details might challenge your own expectations.

Result: Fair Value of $42.80 (UNDERVALUED)

However, the story can shift quickly if wildfire and weather risks raise costs, or if regulatory decisions limit Avista's ability to recover substantial grid spending.

Another Angle: Cash Flows Say Something Different

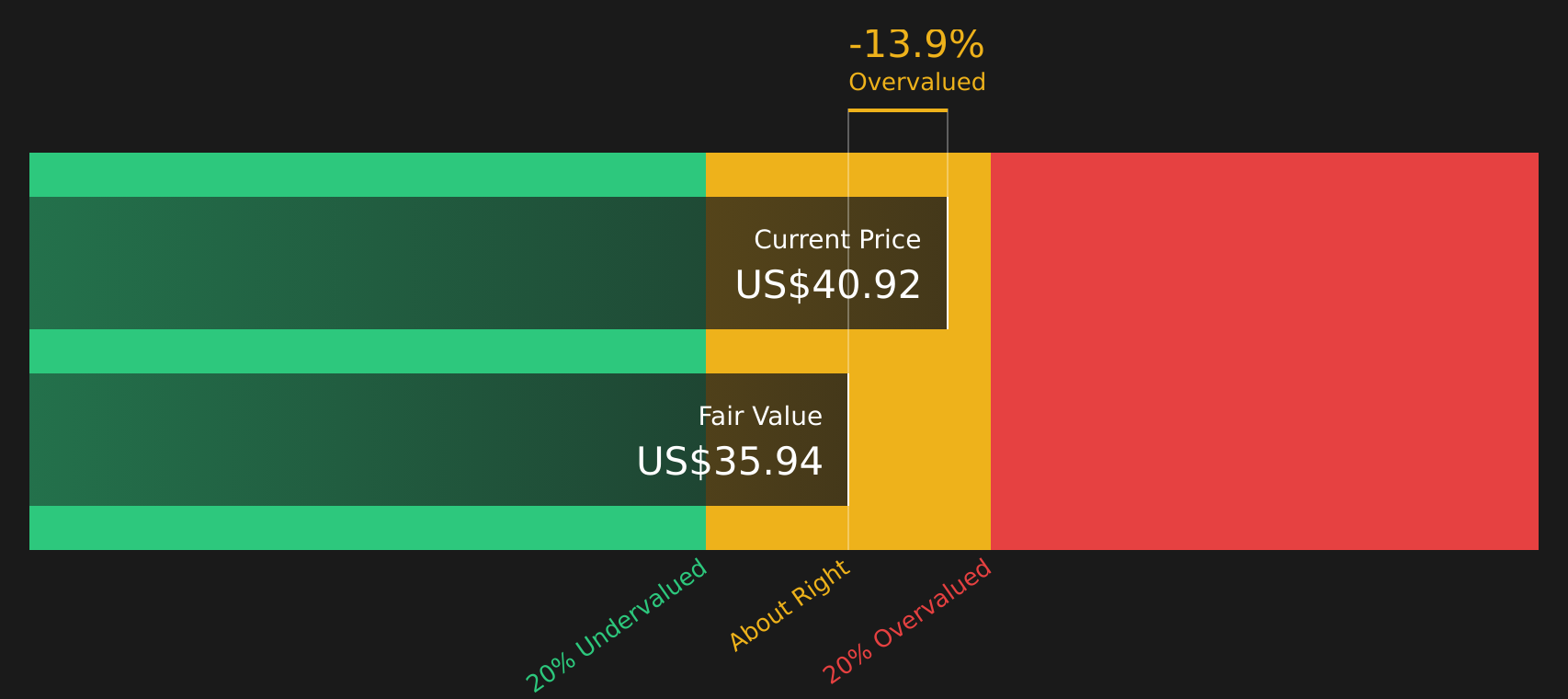

While the fair value narrative pegs Avista at $42.80 and suggests a 3.8% undervaluation, our DCF model points the other way. On that view, the stock at $41.16 sits above an estimated future cash flow value of $35.94, which implies less room for error. Which story do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Avista for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With opinions split between modest upside and tighter cash flow assumptions, now is a good time to review the details yourself, weigh the trade off between concerns and potential, and decide where you stand using our 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If Avista has your attention, do not stop here. Broaden your watchlist with other stocks that match clear fundamentals, income potential and risk filters.

- Spot opportunities that look mispriced on quality and value by running the 48 high quality undervalued stocks.

- Strengthen your income stream by checking out the 13 dividend fortresses.

- Sleep easier at night by focusing on companies in the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.