Assessing Ball’s Valuation After Deutsche Bank’s Positive Coverage On Ball (NYSE:BALL)

Ball Corporation BALL | 0.00 |

Deutsche Bank coverage puts Ball (BALL) in focus

Deutsche Bank’s fresh coverage on Ball (BALL) with a positive rating has put the packaging group back on investors’ radar, prompting a closer look at its fundamentals, recent share performance, and valuation signals.

The Deutsche Bank upgrade comes after a period of mixed momentum, with a 12.4% year to date share price return and a 25.2% 1 year total shareholder return contrasting with weaker 5 year total shareholder returns. This suggests that interest has recently picked up again.

If this kind of renewed interest in individual names has your attention, it could be a good moment to broaden your search with the 20 top founder-led companies

With Ball trading at $59.97, at a 17% discount to the average analyst target and a 41% gap to one intrinsic value estimate, the question is simple: is there real upside left here, or is the market already pricing in future growth?

Most Popular Narrative: 14.6% Undervalued

Ball's most followed narrative pins fair value at $70.25, above the last close of $59.97, which helps explain why fresh coverage is leaning positive.

Post-divestiture focus on core aluminum packaging and disciplined cost control initiatives are driving operational efficiency and capital allocation improvements, supporting higher net margins and accelerating comparable diluted EPS growth targets (12% to 15%) in the near to medium term. Increasing contract coverage (over 90% of 2026 volumes under contract in North America) paired with long-standing customer relationships provides revenue and earnings visibility, mitigating downside risks and enabling further stability in free cash flow and earnings trajectory.

Curious what earnings path and profit profile are baked into that fair value. The narrative leans heavily on steady growth assumptions and a higher future earnings multiple. Want to see which specific revenue, margin and valuation inputs pull that $70.25 figure together.

Result: Fair Value of $70.25 (UNDERVALUED)

However, you still need to weigh up concentration risk in South America and ongoing input cost volatility, either of which could quickly challenge the idea that the stock is underpriced.

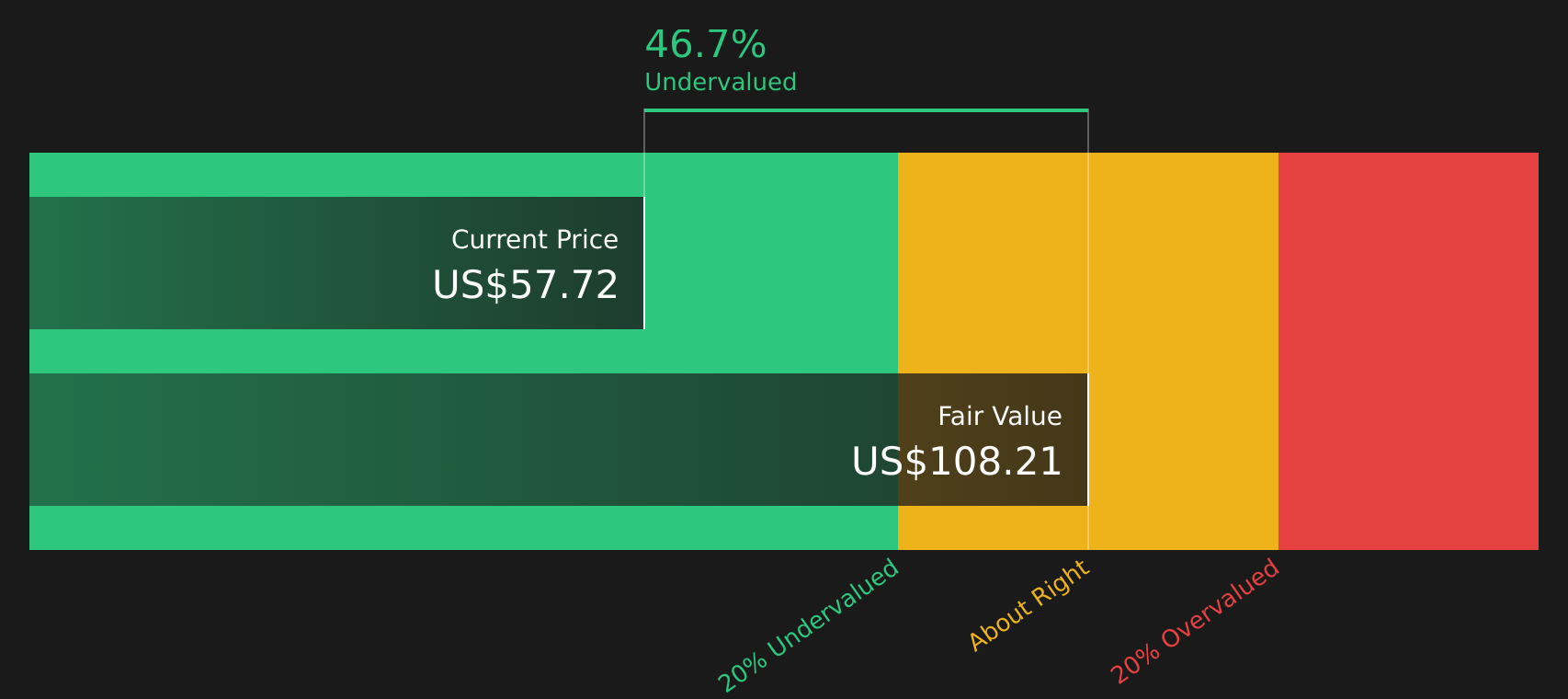

Another Way To Look At Valuation

The DCF view presents Ball as clearly cheap, with the SWS DCF model placing fair value at $101 compared with the current $59.97. That is a wide gap for a packaging business with forecast earnings growth of 8.4% a year, so the real question is whether you trust the cash flow assumptions behind it.

Next Steps

With sentiment split between opportunity and caution, now is a good time to review the numbers yourself, weigh both sides, and see the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop at one stock. Use these focused stock ideas to compare different return profiles, diversify your watchlist, and spot opportunities you might otherwise miss.

- Target dependable cash generators by checking companies offering resilient income profiles through the 13 dividend fortresses

- Hunt for potential mispricings by scanning companies flagged as potentially trading below their estimated worth with the 59 high quality undervalued stocks

- Strengthen your downside protection by focusing on companies flagged for more resilient profiles using the 68 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.