Assessing Bank First (BFC) Valuation After Recent Share Price Softness

Bank First BFC | 0.00 |

Why Bank First stock is catching investor attention

Bank First (BFC) has drawn fresh interest after recent share moves, with the stock down 2.6% over the past month but still showing gains over the past 3 months and year to date.

Short term momentum has softened, with the 7 day share price return down 2.01% and the 30 day share price return down 2.62%. However, the year to date share price return of 15.25% and 1 year total shareholder return of 22.75% still point to stronger longer term performance.

If you are comparing Bank First with other opportunities in financials and beyond, this could be a good moment to broaden your watchlist with 20 top founder-led companies

With Bank First trading at $139.02 against an analyst price target of $165, and an intrinsic value estimate close to the current share price, should you see a genuine mispricing here, or is the market already counting on future growth?

Price-to-Earnings of 21.3x: Is it justified?

Bank First is trading on a P/E of 21.3x, which places the stock at a richer valuation compared with both its own estimated fair level and banking peers.

The P/E ratio compares the current share price with earnings per share, so a higher figure usually means investors are paying more today for each dollar of current earnings. For a bank like Bank First, a higher P/E can signal that the market is factoring in stronger profit growth or a higher quality earnings profile than is typical for the sector.

Here, the current P/E of 21.3x sits above the estimated fair P/E of 19.6x and well above the US Banks industry average of 11.5x, as well as the peer average of 14.3x. That gap suggests investors are currently paying a clear premium relative to both the broader industry and similar companies, and it indicates a level that could move closer to the fair P/E if expectations and reality converge over time.

Result: Price-to-Earnings of 21.3x (OVERVALUED)

However, investors also need to watch for a potential reset in lofty expectations if earnings growth slows or if banking sector sentiment turns against premium valued stocks.

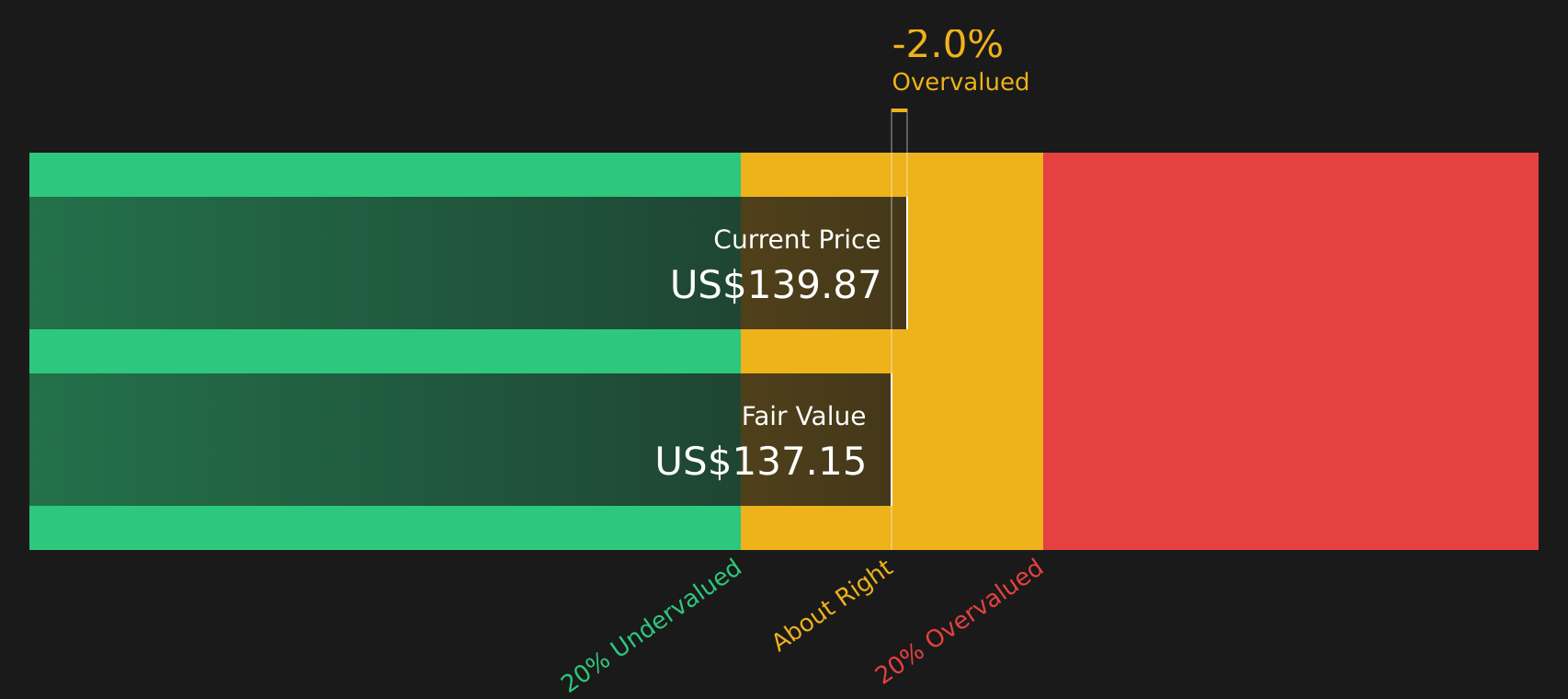

Another way to look at value

While the P/E of 21.3x suggests a premium, the SWS DCF model tells a slightly different story. On this view, Bank First at $139.02 sits just above an estimated future cash flow value of $137.15, implying a small degree of overvaluation rather than a large disconnect. Which signal should matter more to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bank First for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment in this article mixed, this is a good time to look through the numbers yourself and decide whether the optimism around certain rewards really holds up. To see what is driving that optimism, take a closer look at the 3 key rewards.

Looking for more investment ideas?

If Bank First is already on your radar, do not stop there. Use this moment to widen your opportunity set and pressure test your current watchlist.

- Target quality at a discount by scanning 46 high quality undervalued stocks that combine solid fundamentals with pricing that may not fully reflect their underlying metrics.

- Prioritise resilience by checking 64 resilient stocks with low risk scores that score well on financial stability and volatility, so you can focus on steadier business profiles.

- Get ahead of the crowd by reviewing the screener containing 22 high quality undiscovered gems that meet strict quality filters yet still sit off most investors' radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.