Assessing Bank Of America (BAC) Valuation As Credit Card Overhaul And Dividends Draw Investor Focus

Bank of America Corp BAC | 49.38 | +0.22% |

Why this credit card overhaul matters for Bank of America (BAC) shareholders

Bank of America (BAC) is reworking its credit card business with new incentives and heavier use of artificial intelligence, while reaffirming regular dividends, a combination that is pulling fresh attention to the stock.

Recent moves around the credit card revamp, a fresh round of fixed income offerings, preferred stock redemptions and regular dividends come as Bank of America’s share price sits at US$56.53, with a 7 day share price return of 6.26% and a 1 year total shareholder return of 22.02%. This points to momentum that has been supported over longer periods too, with total shareholder returns of 71.89% over 3 years and 91.15% over 5 years.

If news around Bank of America’s credit card push has you thinking more broadly about financials, it could be a good moment to widen your search with 22 top founder-led companies.

With BAC trading at US$56.53 and sitting roughly 10% below the average analyst price target, plus an estimated 14% intrinsic discount, you have to ask: is there still mispricing here, or is the market already baking in its future growth?

Most Popular Narrative: 30% Overvalued

Compared with Bank of America’s last close at $56.53, the most followed narrative pegs fair value closer to the low $40s. This creates a clear gap investors will want to understand.

Bank of America (BofA) exceeded Q4 2024 expectations by reporting net interest income (NII) of $14.5 billion, surpassing estimates by $170 million. Higher interest rates and an increase in commercial and consumer loan volumes drove this growth. The latest results confirm the original assumption that elevated interest rates would benefit BAC’s NII. The strong loan growth and positive NII outlook align with my narrative that BAC’s conservative loan book and strong balance sheet would support its financial performance.

Curious how a bank with growing net interest income, firm margins and ongoing buybacks still lands on a lower fair value? The narrative’s long term earnings path, revenue mix assumptions and profit conversion all feed into that $43.34 figure. The full story connects those moving parts into one valuation spine.

Result: Fair Value of $43.34 (OVERVALUED)

However, there are still pressure points to watch, including any sharp shift in interest rates or a deeper Buffett exit, either of which could quickly change sentiment around BAC.

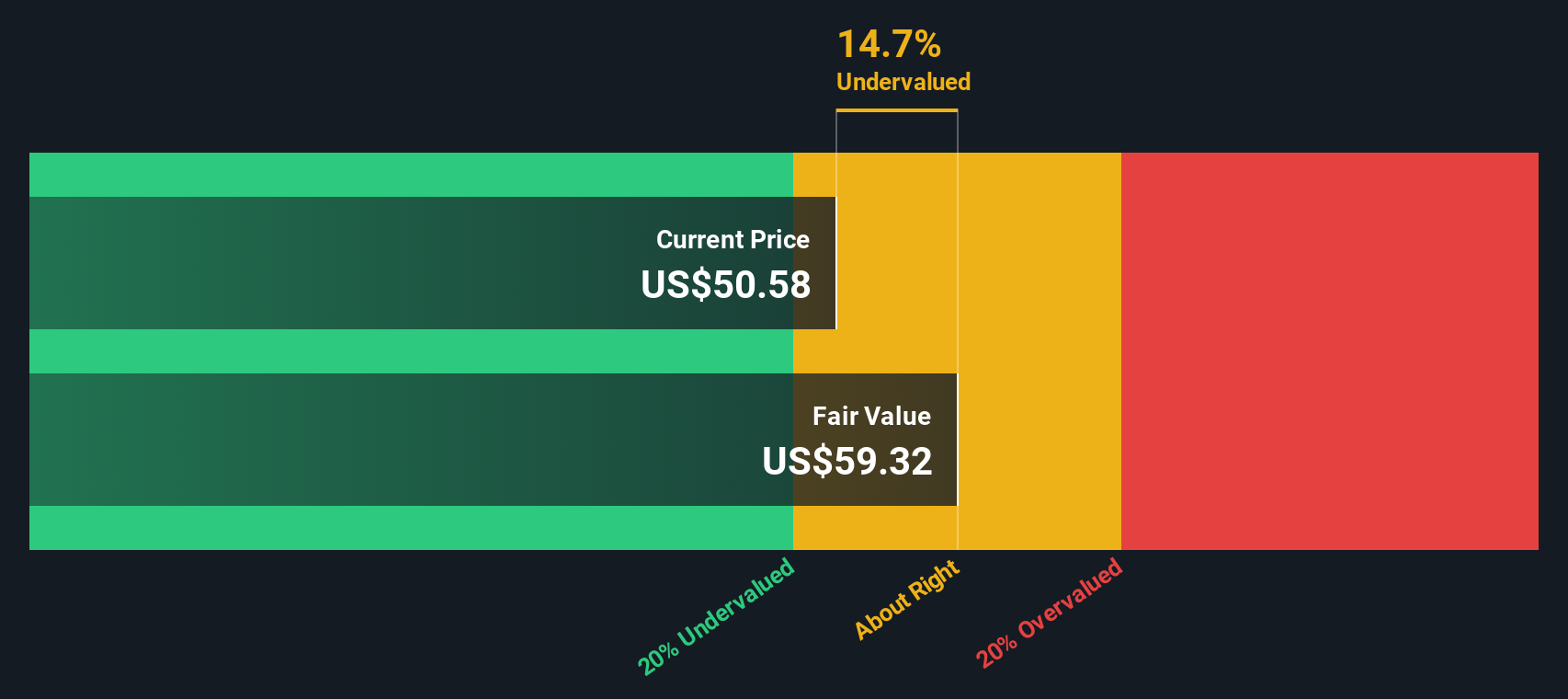

Another View: Cash Flows Point to Undervaluation

The popular narrative describes Bank of America as about 30% overvalued at a fair value of $43.34, but our DCF model tells a different story. Based on our calculations, BAC at $56.53 trades roughly 14% below an estimated future cash flow value of $65.77. Which set of assumptions do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bank of America for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bank of America Narrative

If you are not convinced by any single view or prefer to rely on your own work, you can pull the numbers, stress test the assumptions and Do it your way in less than 3 minutes.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Bank of America.

Looking for more investment ideas?

Once you have a view on Bank of America, do not stop there. Fresh opportunities often show up where you least expect them.

- Target dependable income by reviewing companies in our list of 14 dividend fortresses that focus on robust payouts to shareholders.

- Zero in on quality at a reasonable price with our collection of screener containing 24 high quality undiscovered gems that many investors may be overlooking.

- Prioritize resilience by scanning companies in the 86 resilient stocks with low risk scores that aim to keep risk profiles relatively contained.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.