Assessing BioMarin (BMRN) Valuation As Shares Show Recent Weakness And DCF Signals Deep Discount

BioMarin Pharmaceutical Inc. BMRN | 0.00 |

Recent performance snapshot

BioMarin Pharmaceutical (BMRN) has drawn fresh attention after recent trading, with the share price at US$54.06 and returns showing a 0.3% move over the past day and 1.7% over the past week.

Over the past month, the stock shows a 5.6% decline and about a 4.4% decline over the past 3 months. This has prompted some investors to reassess the company’s current valuation against its fundamentals.

Set against a weaker year, with a 1 year total shareholder return of 12.85% decline and a 3 year total shareholder return of 44.05% decline, the recent 1 week share price gain suggests that earlier negative momentum may be easing as investors reassess risk and potential around BioMarin’s rare disease portfolio.

If you are weighing BioMarin against other opportunities in healthcare, this can be a useful moment to scan for fresh ideas using our screener of 33 healthcare AI stocks

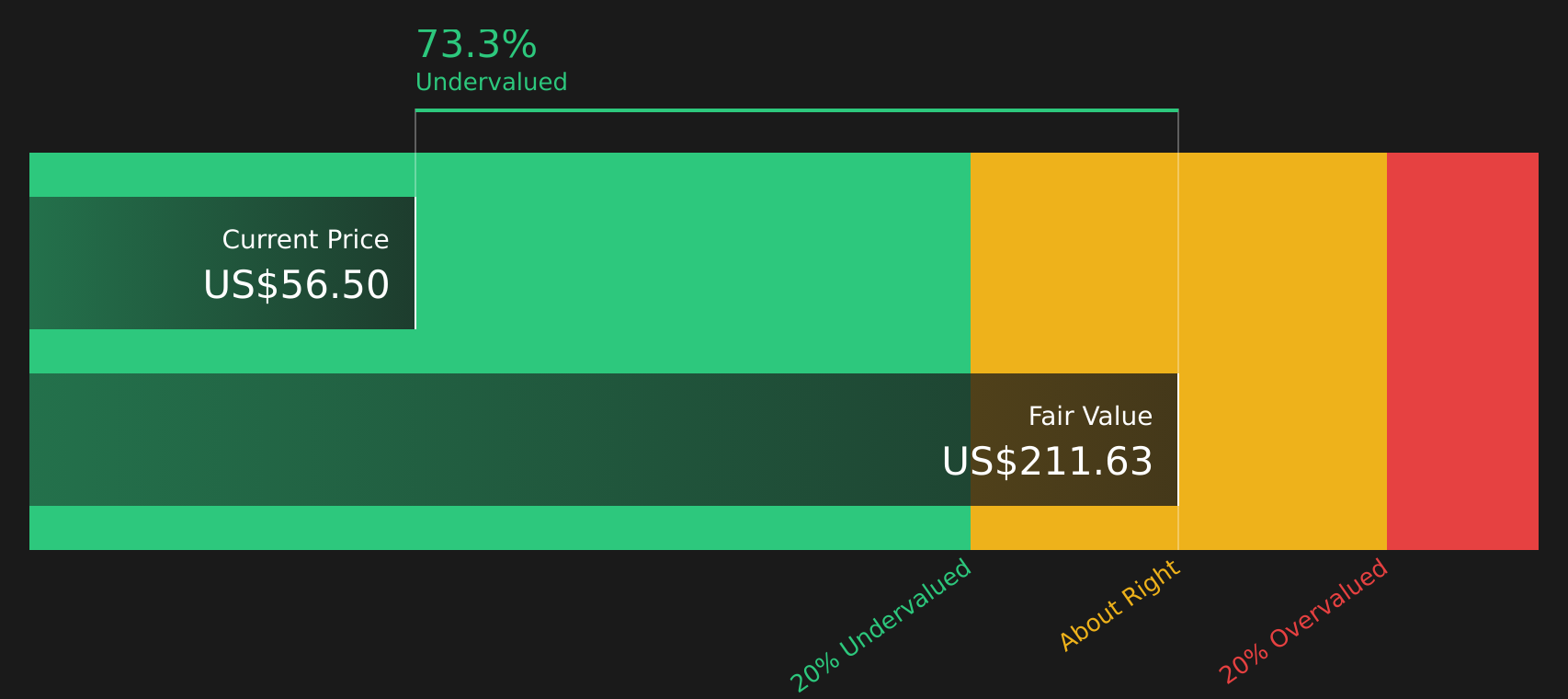

So with BioMarin trading at US$54.06, showing an intrinsic discount of about 71% and a large gap to the average analyst price target, is this a genuine entry point, or is the market already pricing in future growth?

Most Popular Narrative: 39.2% Undervalued

BioMarin’s most followed narrative places fair value at about $88.87 per share versus the recent $54.06 close, framing the stock as trading at a steep discount in that model.

Recent acquisition of Inozyme and ongoing business development initiatives broaden BioMarin's enzyme therapy portfolio and introduce new high-value therapies targeting severe unmet needs, enhancing diversification and durability of revenue streams over the long term.

Curious what underpins that gap between price and fair value? The narrative focuses on faster earnings growth, expanding margins, and a richer mix of therapies over time.

Result: Fair Value of $88.87 (UNDERVALUED)

However, there are clear pressure points, including heavier R&D and SG&A spending around the Inozyme deal, as well as Voxzogo facing competition that could challenge current revenue expectations.

Another view on valuation

The SWS DCF model points to a fair value of about $189.78 per share, which is far above the recent $54.06 price and implies BioMarin is deeply undervalued using that approach. That sits in clear tension with its current 29.9x P/E, which looks expensive versus industry peers. Which signal do you trust more right now: the cash flow model or the market multiple?

Next Steps

The mix of pressure points and potential rewards around BioMarin will not stay under the radar for long. Check the numbers yourself and weigh both sides with 2 key rewards and 2 important warning signs

Looking for more investment ideas?

Before moving on, you can explore fresh opportunities across sectors by checking out targeted stock lists built from consistent rules and up to date data.

- Explore potentially more stable profiles by scanning 67 resilient stocks with low risk scores which focuses on companies with lower risk scores and steadier characteristics.

- Look for quality at a lower price through screener containing 25 high quality undiscovered gems where smaller, less-followed businesses may offer solid fundamentals.

- Emphasize financial strength with solid balance sheet and fundamentals stocks screener (45 results), highlighting companies that combine balance sheet support with fundamental stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.