Assessing Bit Digital (BTBT) Valuation After Earnings Loss And New Investor Relations Hire

Bit Digital, Inc. BTBT | 0.00 |

Bit Digital (BTBT) is back on investors' radar after first quarter results showed revenue of US$27.92 million and a net loss of US$146.67 million, alongside the appointment of a new Head of Investor Relations.

At a share price of US$1.94, Bit Digital has seen a 10.23% 1 day share price return and an 18.29% 90 day share price return, yet its 1 year total shareholder return is still down 22.40%. This suggests recent momentum is picking up after a weaker longer term experience as investors reassess the earnings result and new investor relations leadership.

If this mix of crypto infrastructure and AI exposure has caught your eye, it could be a good moment to look at other cryptocurrency and blockchain related opportunities through the 22 cryptocurrency and blockchain stocks

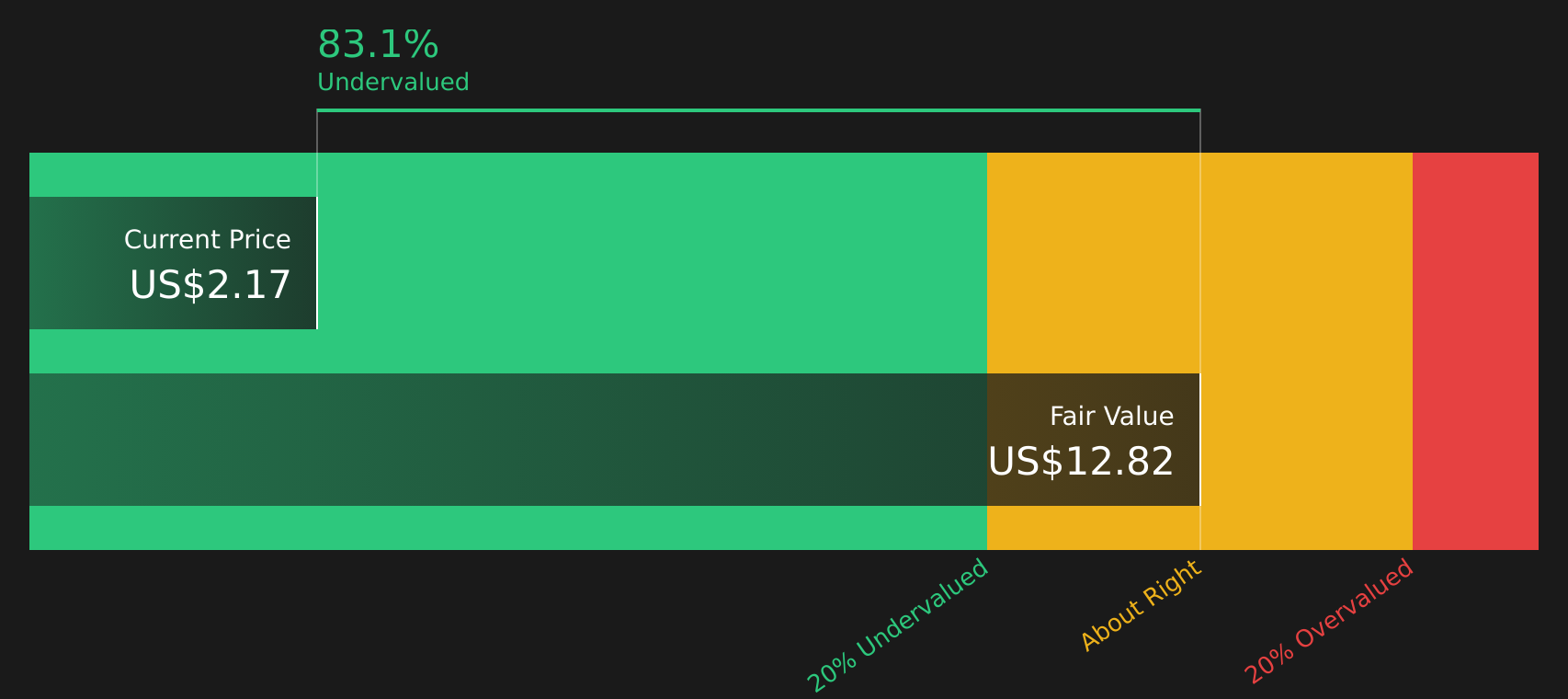

With Bit Digital posting a larger quarterly loss yet trading at US$1.94 alongside an analyst price target of US$4.60, investors now face the question of whether this stock is undervalued or already pricing in future growth.

Most Popular Narrative: 62.1% Undervalued

Bit Digital's most followed narrative points to a fair value of $5.13 per share versus the recent $1.94 close, framing a wide gap that hinges on its Ethereum focused pivot and high performance computing exposure.

The company's structural pivot to become a dedicated Ethereum treasury and staking platform positions it to capitalize on the growing acceptance of Ethereum among institutional investors and asset managers, expected to drive future revenue growth through larger scale ETH holdings and increased staking yields.

Curious what assumptions justify that valuation gap? The narrative leans heavily on rapid revenue expansion, margin rebuild, and a richer future earnings multiple. The exact mix might surprise you.

Result: Fair Value of $5.13 (UNDERVALUED)

However, you still need to weigh real pressure points, including heavy reliance on Ethereum related income and the potential for equity dilution if further capital raises are required.

Another Way To Look At Value

The SWS DCF model paints a very different picture, with an estimated future cash flow value of $12.73 per share versus the current $1.94 price, which flags Bit Digital as heavily undervalued on this approach. When one model sees room and another signals risk, which do you trust more?

Next Steps

Mixed signals on value and risk so far? Use the data, sentiment and valuation work as a starting point. Then pressure test the 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

If Bit Digital has sharpened your interest, do not stop here, broaden your watchlist with other focused ideas that could suit your risk, income, and quality preferences.

- Chase higher potential by reviewing carefully selected 28 elite penny stocks with strong financials that pair smaller market caps with stronger balance sheets and fundamentals than many typical micro caps.

- Target value opportunities by scanning 53 high quality undervalued stocks that combine quality cash flows with balance sheet strength, so you are not relying only on sentiment.

- Prioritize resilience by assessing 66 resilient stocks with low risk scores that score well on financial health and business risk, helping you avoid fragile situations that can surprise investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.