Assessing Bloom Energy’s Valuation After New Brookfield Deal And Data Center Growth Plans

BLOOM ENERGY CORP BE | 176.67 203.43 | +5.98% +15.15% Pre |

Bloom Energy (BE) is back in focus after securing a multibillion dollar partnership with Brookfield Asset Management, expanding ties with hyperscale operators, and planning to double annual production capacity by 2026.

Those data center partnerships and guidance for US$3.1b to US$3.3b in 2026 revenue sit against a share price of US$139.74, with a 90 day share price return of 28.28% and a very large 1 year total shareholder return. This signals strong but volatile momentum following recent single month share price weakness.

If Bloom Energy’s surge has you looking at the wider power and data infrastructure theme, it could be worth scanning 24 power grid technology and infrastructure stocks as a starting list of related names to research next.

After a very large 1 year return, a US$20b backlog and revenue guidance above US$3b, Bloom already carries big expectations, so the key question is whether there is still an opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 25.7% Overvalued

Against a fair value estimate of about $111.18, Bloom Energy’s last close at $139.74 sits well above what the most followed narrative models out, putting the spotlight on the assumptions behind that gap.

The analysts have a consensus price target of $34.57 for Bloom Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $48.0, and the most bearish reporting a price target of just $10.0.

Want to see what kind of revenue run rate, margin expansion and future earnings multiple are being baked into that fair value? The narrative leans on fast compounding top line, a step change in profitability, and a richer earnings rating than the wider electrical space. Curious which assumptions matter most for closing the gap between $111 and $139?

That fair value of roughly $111 per share is built using a 9.28% discount rate and a detailed set of long term cash flow and profitability forecasts, then compared with today’s $139.74 price where the market is trading. The narrative blends expectations for strong revenue growth, rising profit margins and a higher future P/E multiple than the wider US Electrical industry to arrive at its estimate.

Result: Fair Value of $111.18 (OVERVALUED)

However, the narrative could be knocked off course if natural gas reliance weighs on adoption, or if the planned manufacturing expansion fails to match actual demand.

Another View: Sales Multiple Paints A Richer Picture

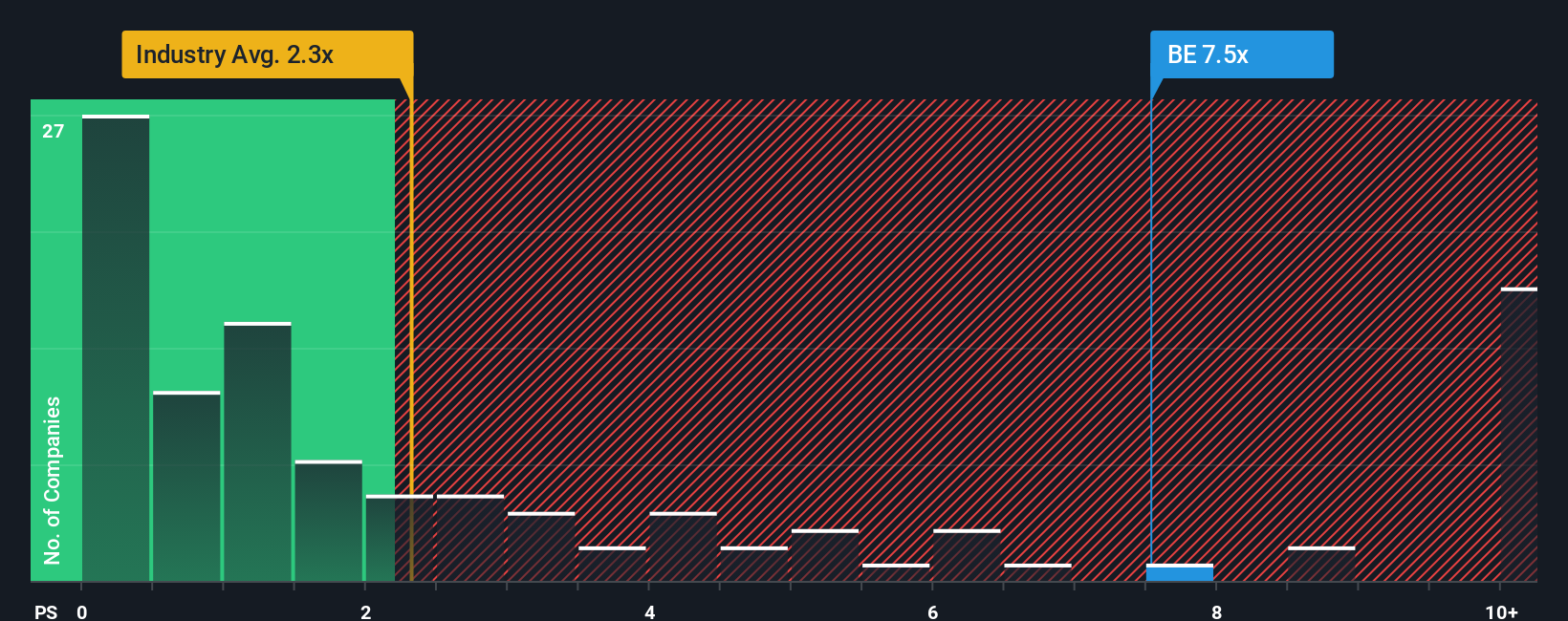

While the narrative fair value of about $111.18 suggests Bloom Energy looks overvalued at $139.74, its P/S of 19.4x adds a second angle. That is slightly below peer companies at 20.3x, yet far above the US Electrical industry at 2.5x and the fair ratio of 10.3x, which indicates meaningful valuation risk if sentiment cools.

Next Steps

With all this in mind, does the current story feel too hot or still interesting to you, and are you ready to move quickly and test your own thesis against the data, including our breakdown of 1 key reward and 2 important warning signs?

Looking for more investment ideas?

If Bloom Energy has raised your interest, do not stop here. Use the screener to spot other opportunities that might fit your style before they move without you.

- Target quality at a discount by reviewing 55 high quality undervalued stocks, a focused set of companies that our filters flag as trading below their assessed worth.

- Prioritise resilience by scanning 81 resilient stocks with low risk scores, highlighting businesses with lower risk scores that may suit investors who want fewer surprises.

- Get ahead of the crowd by checking our screener containing 24 high quality undiscovered gems, a collection of under the radar names with fundamentals that stand out in the data.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.