Assessing Booking Holdings (BKNG) Valuation After Agoda AI Chatbot Launch And Vietnam Travel Interest

Booking Holdings Inc. BKNG | 4194.31 | +0.23% |

Interest in Booking Holdings (BKNG) is being shaped by two Agoda updates: the launch of its AI-powered Booking Form Bot to support travelers at checkout, and reported growth in family travel searches for Vietnam.

At a share price of $5,391.52, Booking Holdings has had a relatively steady year, with a 6.11% 90 day share price return and a 13.66% 1 year total shareholder return. These figures suggest momentum has been building over time as investors reassess growth potential and risks around travel and AI adoption.

If Agoda’s AI tools and rising interest in Asian travel have caught your attention, it could be a good moment to broaden your search and check out high growth tech and AI stocks.

With the share price at US$5,391.52, solid recent returns, and an implied discount to both analyst targets and intrinsic value metrics, is Booking Holdings still offering mispriced upside, or is the market already baking in future growth?

Most Popular Narrative: 13.2% Undervalued

With Booking Holdings last closing at US$5,391.52 and the most followed narrative pointing to fair value around US$6,213, the gap centers on earnings power and AI driven travel demand.

Booking Holdings is incorporating AI technology across its platforms to improve operations, streamline traveler experiences, and enhance supplier partnerships, which is expected to drive future revenue growth and margin improvement. The company's focus on increasing alternative accommodations and expanding its Genius loyalty program aims to strengthen customer retention and capture a broader market, potentially boosting revenue and net margins.

Curious what kind of revenue path, margin profile and valuation multiple are needed to support that higher fair value, all discounted back at 8.61%? The narrative lays out a detailed glide path for earnings and profitability that is more optimistic than recent headline numbers suggest, and leans on a future P/E closer to quality compounders than traditional travel names.

Result: Fair Value of $6,213 (UNDERVALUED)

However, you still need to weigh the risk that weaker travel demand or higher customer acquisition costs could pressure revenue, shrink margins, and challenge today’s AI-driven optimism.

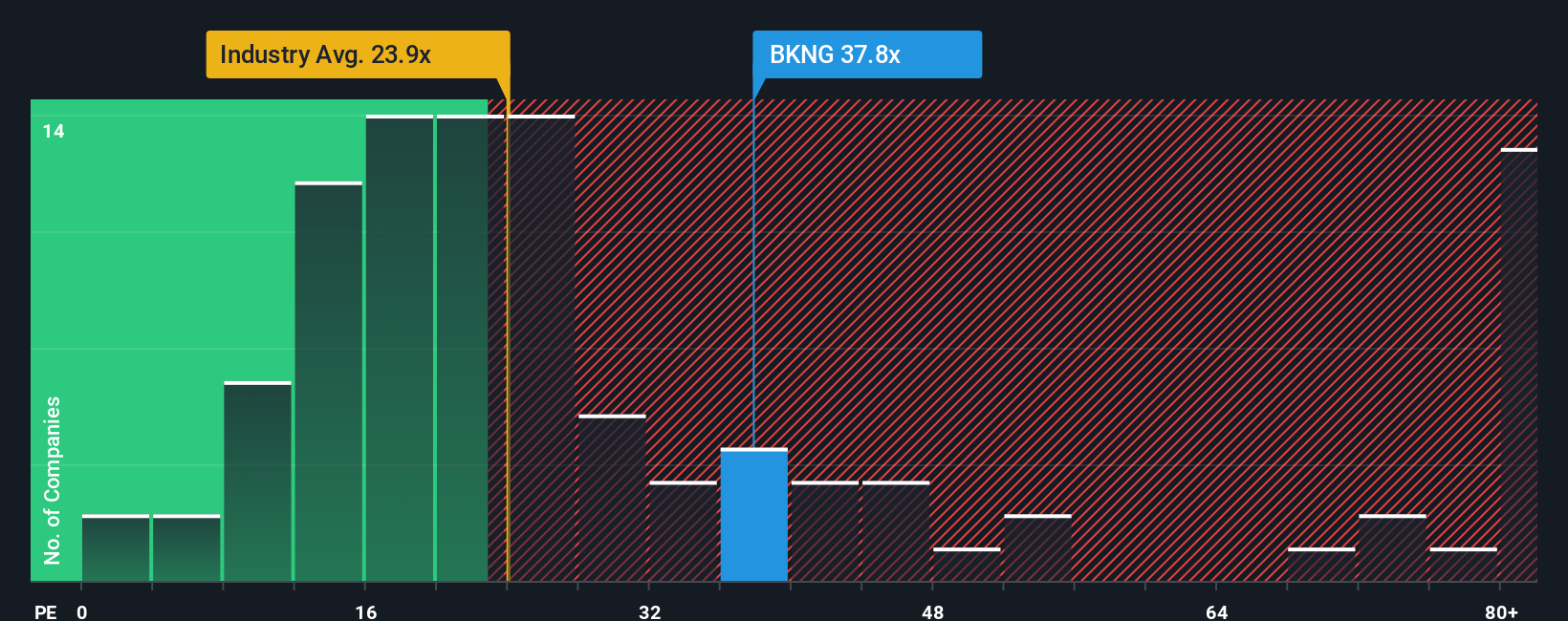

Another Angle: Expensive On P/E

The AI narrative points to around 13% upside to fair value, yet the current P/E of 34.5x tells a different story. That multiple sits above the peer average of 31.8x and well above the US Hospitality industry at 21.9x, while our fair ratio sits even higher at 39.1x.

So you have a stock that screens costly against its sector, but still below the fair ratio that the numbers point to. Is the market being cautious about future execution, or is this a case where a quality premium could stick around longer than many expect?

Build Your Own Booking Holdings Narrative

If you see the numbers differently or want to test your own assumptions, you can build a custom Booking Holdings view in just a few minutes. Do it your way

A great starting point for your Booking Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If Booking Holdings has sharpened your thinking, do not stop here. Broaden your watchlist with focused stock ideas that match how you like to invest.

- Target potential growth at lower price points by scanning these 3537 penny stocks with strong financials that pair smaller market caps with stronger fundamentals than many expect.

- Ride AI driven trends by checking out these 26 AI penny stocks where companies are working on automation, machine learning tools, and data heavy products.

- Hunt for pricing gaps by reviewing these 880 undervalued stocks based on cash flows that appear cheap relative to their cash flow profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.