Assessing Bruker (BRKR) Valuation After Recent Share Price Weakness

Bruker Corporation BRKR | 36.76 | +1.88% |

Why Bruker Stock Is On Investors’ Radar Today

Bruker (BRKR) is back in focus after recent trading left the shares with a 1 day return of about a 2% decline and a roughly 4% decline over the past week, prompting fresh interest in its fundamentals.

At a share price of US$47.67, Bruker’s short term momentum looks softer after a 1 day share price return of about 2% decline and a 7 day share price return of roughly 4% decline. However, the 90 day share price return of 26.31% contrasts with a 1 year total shareholder return of 14.62% decline, which hints that sentiment has cooled over the longer stretch even as more recent trading has been stronger.

If Bruker’s recent swings have you reassessing your watchlist, this could be a good moment to scan other healthcare names using the healthcare stocks as a starting point.

With Bruker trading at US$47.67, carrying a value score of 3 and sitting at a roughly 14% discount to the average analyst price target, it is worth asking whether this reflects a genuine mispricing or whether the market is already factoring in future growth.

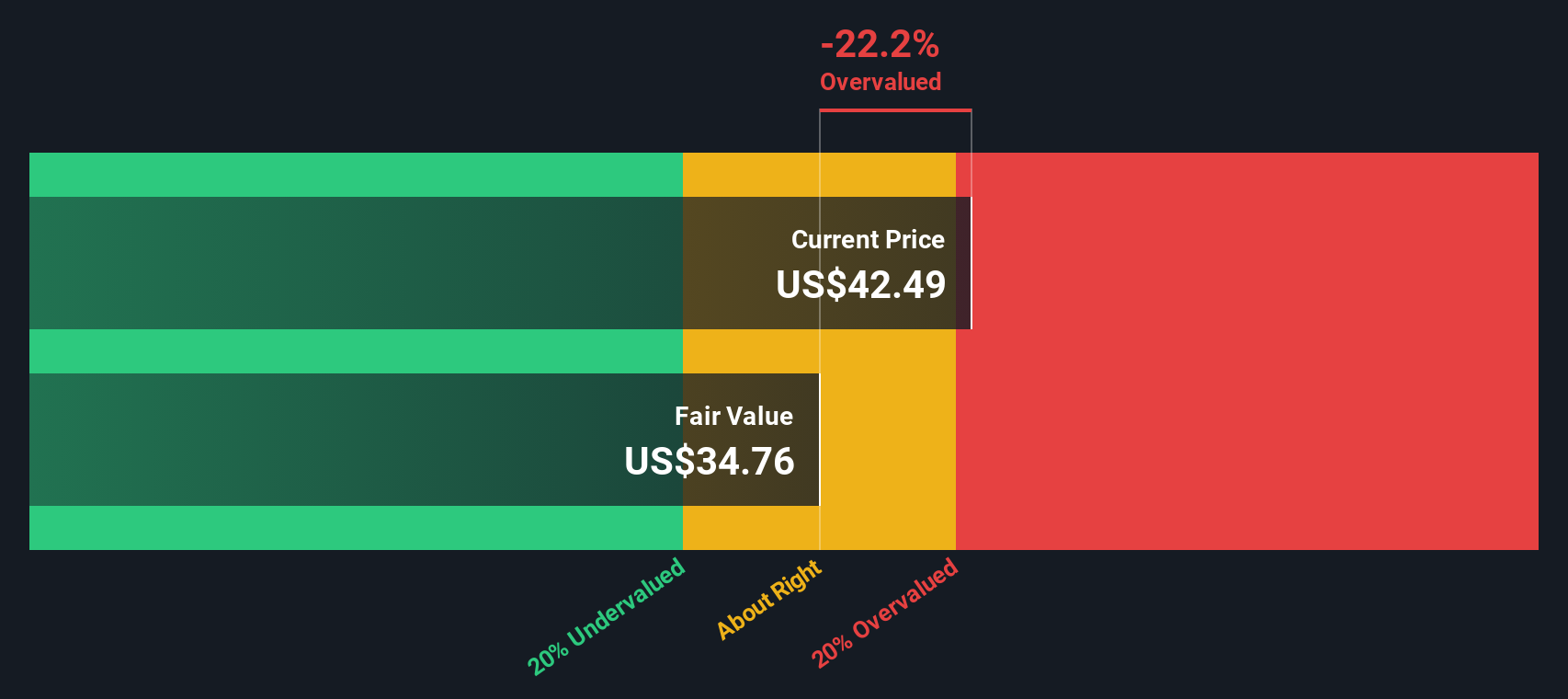

Most Popular Narrative: 11.8% Undervalued

Bruker’s most followed narrative points to a fair value of about $54.07 per share versus the latest close at $47.67, suggesting room between price and modelled worth.

The expected stabilization and eventual recovery of research and biopharma funding in both the US and China, along with global settlements on tariffs, could trigger a rebound in demand for Bruker's advanced life science and drug discovery instruments, supporting renewed top-line revenue growth post-2025.

The company's pipeline of recent innovations (e.g., next-generation tims mass spectrometry, spatial biology, automated diagnostics) positions it to benefit from sustained investment in personalized medicine, genomics, and high-throughput scientific R&D, supporting both future revenue expansion and favorable product mix improvements.

Want to see how modest revenue growth, a step up in margins, and a lower future P/E are stitched together into that fair value? The narrative sets specific hurdles for earnings, cash flows, and the discount rate that need to line up almost perfectly. If you are curious which of those assumptions does the heavy lifting, the full story makes it very clear without leaving much to guesswork.

The fair value output of about $54.07 is built using a discount rate of roughly 8.39%, along with detailed expectations for Bruker’s revenue, profit margins and future earnings profile. That narrative also weighs analyst views on how much investors might be willing to pay for those earnings in a few years via a future P/E multiple, then brings everything back to today’s dollars.

Result: Fair Value of $54.07 (UNDERVALUED)

However, persistent funding headwinds in key research markets, along with a heavier reliance on cost cuts rather than organic growth, could quickly challenge that underappreciated upside story.

Another View: Cash Flows Paint A Tougher Picture

While the popular narrative points to a fair value of about $54.07 and labels Bruker as undervalued, our DCF model lands closer to $36.69 per share, which implies the stock is overvalued on that framework. With two models pulling in opposite directions, which one lines up better with your own expectations?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bruker for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 872 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bruker Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a custom view in just a few minutes using Do it your way.

A great starting point for your Bruker research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Bruker has you thinking harder about where to put your money to work, do not stop here. Your next strong idea could be one smart screener away.

- Spot potential value plays early by scanning these 872 undervalued stocks based on cash flows that may trade below what their cash flows suggest.

- Tap into the growth story around artificial intelligence through these 24 AI penny stocks that are directly tied to this theme.

- Hunt for income opportunities using these 13 dividend stocks with yields > 3% that already offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.