Assessing Bruker (BRKR) Valuation After Recent Share Price Weakness And Loss-Making Results

Bruker Corporation BRKR | 36.76 | +1.88% |

Bruker stock performance snapshot and recent context

Bruker (BRKR) has recently drawn investor attention after a month return of about a 22% decline, extending a softer pattern over the past year, even as the company reports annual revenue of US$3.4b and a net loss of US$23.7m.

At a latest share price of US$41.04, Bruker’s recent 30 day share price return of a 22.08% decline and 1 year total shareholder return of a 26.38% loss point to fading momentum, despite a slightly positive 90 day share price return.

If Bruker’s pullback has you reassessing opportunities in medical technology and diagnostics, it could be a good moment to broaden your watchlist with 25 healthcare AI stocks.

With Bruker posting US$3.4b in revenue, a net loss of US$23.7m and trading at US$41.04, should you view the recent weakness as a potential mispricing to monitor, or assume that the market is already factoring in the company’s future growth potential?

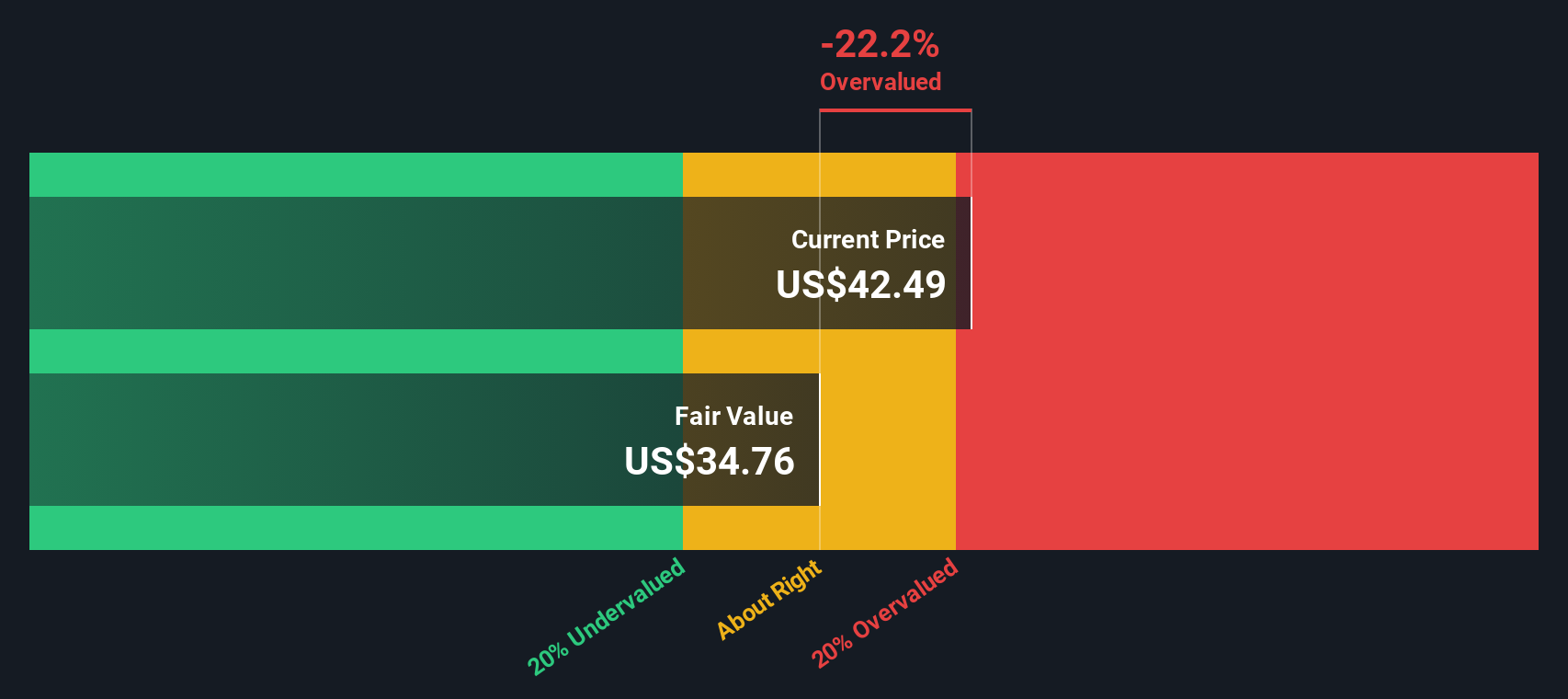

Most Popular Narrative: 24.6% Undervalued

Bruker’s most followed narrative sets a fair value of $54.43 per share, above the last close at $41.04, which frames the stock as materially discounted in that framework.

The expected stabilization and eventual recovery of research and biopharma funding in both the US and China, along with global settlements on tariffs, could trigger a rebound in demand for Bruker's advanced life science and drug discovery instruments, supporting renewed top-line revenue growth post-2025.

Bruker's expanded cost reduction program (targeting $100 to $120 million of annualized savings, mainly realized in FY26) is set to drive at least 300 basis points of operating margin expansion and double-digit EPS growth even in a flat to muted revenue environment, improving net margins and earnings quality.

Curious how a company that is currently loss making is modeled to support this higher value per share? Revenue trends, margin reset, and the earnings multiple all pull in different directions, and the narrative stitches those moving parts into a single number you can benchmark against the current price.

Result: Fair Value of $54.43 (UNDERVALUED)

However, this depends on research funding trends and demand recovering as expected, and on cost cuts not masking weaker organic growth or pressure on Bruker’s core markets.

Another take using our DCF model

While the most popular narrative points to a fair value of $54.43 per share, our DCF model comes in lower, at $36.90. On that view, Bruker’s current price of $41.04 screens as overvalued. This raises a simple question for you: do you place more weight on the cash flow math or on the narrative earnings path?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bruker for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bruker Narrative

If you see the data differently or prefer to test your own assumptions, you can build a complete Bruker story in minutes by starting with Do it your way.

A great starting point for your Bruker research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Bruker is already on your radar, do not stop there. Widen your search with focused stock ideas that match how you like to build a portfolio.

- Target potential value opportunities by scanning our list of 55 high quality undervalued stocks that pair solid fundamentals with prices that may sit below their estimated worth.

- Strengthen your income focus by reviewing 15 dividend fortresses that prioritize reliable cash returns alongside capital preservation.

- Prioritize resilience by checking 81 resilient stocks with low risk scores that score well on our risk framework and may help you sleep better through market swings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.