Assessing Bunge Global (BG) Valuation After Earnings Lift Sales But Pressure Profitability

Bunge Global SA BG | 129.42 | +0.86% |

Why Bunge Global (BG) Is Back in Focus After Its Latest Earnings

Bunge Global (BG) is back on investors’ radar after its latest earnings, reporting fourth quarter sales of US$23,762 million and net income of US$95 million, compared with US$602 million a year earlier.

The latest earnings release appears to have reset expectations, yet the share price has still built momentum, with a 30 day share price return of 18.66% and a 1 year total shareholder return of 77.56% indicating strong recent and longer term gains.

If Bunge Global’s move has you thinking about what else is working in the market, this could be a good moment to broaden your search with 22 top founder-led companies.

With earnings per share moving from US$7.99 for 2024 to US$4.91 for 2025, and the share price surging over the past year, is Bunge Global trading at a discount, or is the market already pricing in future growth potential?

Most Popular Narrative: 7% Overvalued

With Bunge Global last closing at $118.65 against a narrative fair value of about $110.90, the most followed view sees the current price as a premium and ties that to long term earnings potential driven by corporate actions and capital returns.

Analysts now set their price target for Bunge Global at about US$110.90, up from roughly US$110.10, citing small tweaks to the discount rate, long term revenue and margin assumptions, as well as a slightly higher expected future P/E multiple.

Curious what is sitting under that fair value bump? The narrative leans on heavier assumed revenues, firm margins and a richer earnings multiple tied to future execution. The key question is how those moving parts interact over time.

Based on this narrative, Bunge Global is valued using a 6.99% discount rate, higher projected revenues and modestly lower net profit margins, with an earnings multiple that sits above its own assumed starting point but below some broader industry figures.

The result is a fair value estimate just below the current share price, so readers comparing $118.65 to $110.90 can see how tightly the narrative links operational assumptions, capital allocation and valuation.

Result: Fair Value of $110.90 (OVERVALUED)

However, there are still pressure points, including biofuel policy changes and Viterra integration risks, that could challenge those revenue, margin and P/E assumptions.

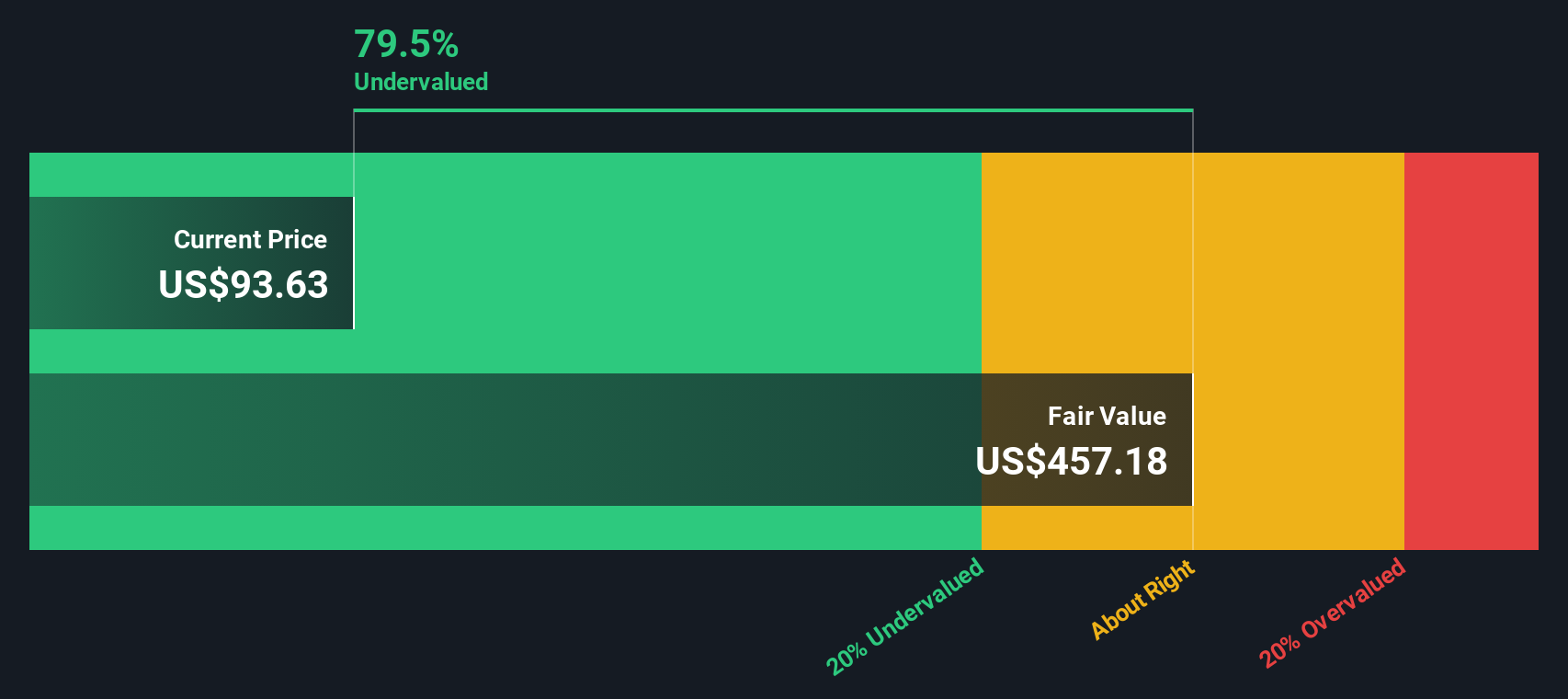

Another View: Cash Flows Tell a Different Story

While the popular narrative pins Bunge Global at a fair value of about $110.90 and labels the stock as slightly overvalued, our DCF model suggests something very different. On this view, the current price of $118.65 sits roughly 76% below an estimated future cash flow value of $491.34. This raises the question of which set of assumptions you find more convincing.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bunge Global for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bunge Global Narrative

If you see the numbers differently, or prefer to test your own assumptions, you can build a tailored view in just a few minutes with Do it your way.

A great starting point for your Bunge Global research is our analysis highlighting 2 key rewards and 5 important warning signs that could impact your investment decision.

Ready For More Investment Ideas?

If Bunge Global has sharpened your thinking, do not stop here. The wider market is full of other opportunities that could fit your plan even better.

- Target resilient income by scanning companies with solid payouts and balance sheets using our list of 14 dividend fortresses.

- Spot potential mispricings quickly by reviewing companies that screen as 52 high quality undervalued stocks based on quality and fundamentals.

- Get ahead of the crowd by checking our screener containing 24 high quality undiscovered gems that still fly under most investors' radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.