Assessing Cactus (WHD) Valuation After A Strong Short Term Share Price Run

Cactus, Inc. Class A WHD | 47.79 | +1.75% |

Why Cactus Stock Is On Investors’ Radar Today

Cactus (WHD) has recently caught investor attention after a period of mixed share performance, with a monthly gain alongside a negative 1-year total return. This divergence has prompted closer scrutiny of its current valuation.

At a share price of US$53.47, Cactus has seen strong near term momentum, with a 30 day share price return of 16.21% and a 90 day gain of 34.18%. This comes as the 1 year total shareholder return of 14.55% contrasts with a 5 year total shareholder return of 114.92%, suggesting longer term holders have still seen meaningful value creation.

If recent moves in Cactus have you looking beyond a single name, this could be a useful moment to check out fast growing stocks with high insider ownership.

With Cactus trading at US$53.47, sitting above the average analyst price target yet showing an implied intrinsic discount of around 33%, investors are left with a key question: is this a genuine mispricing, or is the market already factoring in expectations for future growth?

Most Popular Narrative: 10% Overvalued

With Cactus closing at $53.47 against a narrative fair value of $48.63, the most followed view sees the current price sitting ahead of its calculated worth, built on specific growth and profitability assumptions.

The acquisition of a majority interest in Baker Hughes' Surface Pressure Control business will significantly expand Cactus' geographic footprint and customer base into the Middle East, an area poised for long-term energy infrastructure investment and supply security; this is likely to drive sustained revenue growth and higher earnings resiliency.

Curious what revenue path and profit profile support that fair value, and how a higher future earnings multiple ties it all together? The full narrative lays out the step by step forecasts behind this valuation call, including how margin trends and share count assumptions feed into the model.

Result: Fair Value of $48.63 (OVERVALUED)

However, you still need to weigh risks such as weaker U.S. drilling activity and acquisition integration issues that could challenge those revenue and margin assumptions.

Another Angle On Cactus’ Valuation

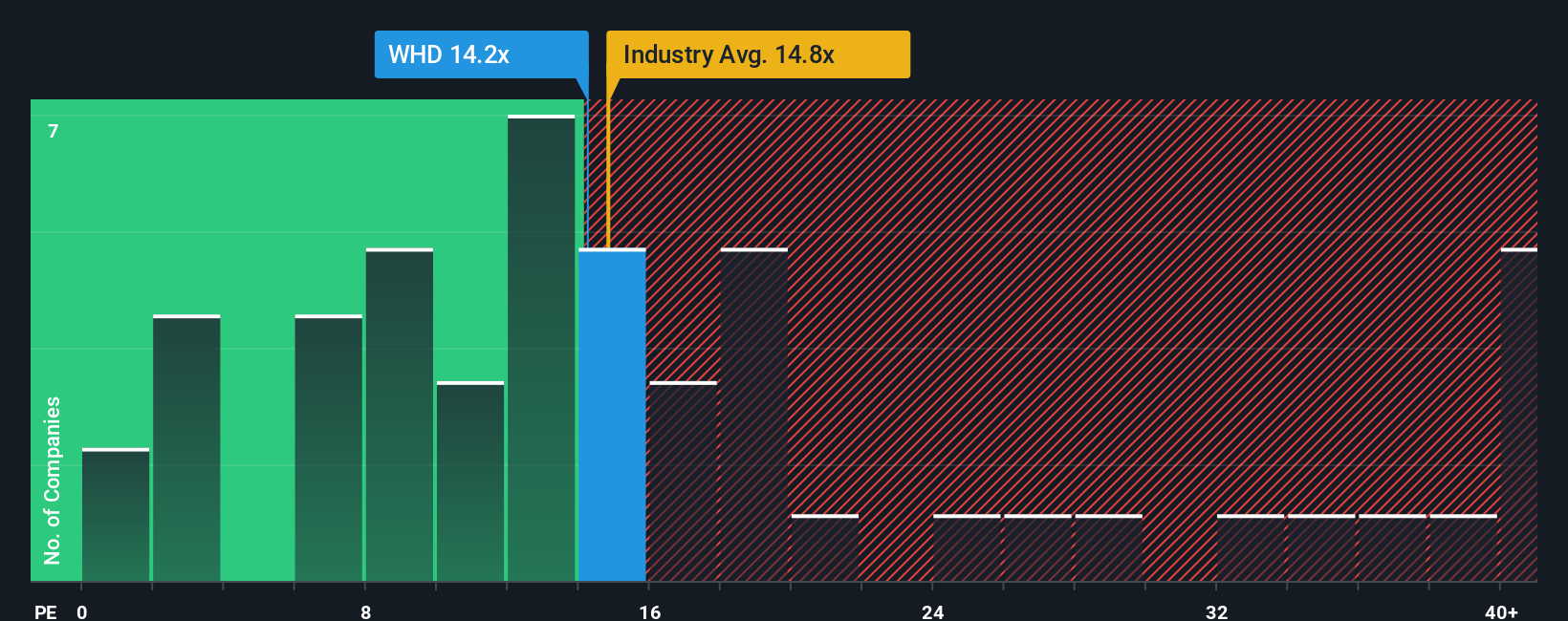

While the narrative fair value of $48.63 suggests Cactus is about 10% overvalued, the current P/E of 21.3x tells a slightly different story. It sits below the US Energy Services industry at 22.2x and well under peers at 43.3x, yet above the 17.6x fair ratio our model points to.

In practice, that mix hints at some valuation risk if sentiment cools. It also shows the share price is not stretched compared with many peers. The question is which signal carries more weight: the peer gap, or the move toward the fair ratio the market could head for next?

Build Your Own Cactus Narrative

If you see the numbers differently or prefer to rely on your own work, you can quickly build a custom view using Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Cactus.

Looking for more investment ideas?

If Cactus has sharpened your focus, do not stop with a single stock; broaden your watchlist with targeted ideas that match how you like to invest.

- Spot potential value entries by checking out these 872 undervalued stocks based on cash flows that line up with your approach to fundamentals and pricing discipline.

- Tap into structural shifts in technology by scanning these 23 AI penny stocks that are tied to real businesses and measurable results.

- Strengthen your income focus by reviewing these 13 dividend stocks with yields > 3% that can complement growth names in your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.