Assessing CareTrust REIT (CTRE) Valuation After Strong Long Term Gains And Recent Price Choppiness

CareTrust REIT, Inc. CTRE | 0.00 |

Recent performance context

CareTrust REIT (CTRE) has attracted fresh attention after recent trading left the stock around $39.34, with returns roughly flat over the past month and slightly lower over the past 3 months.

Recent moves have been choppy, with the share price down 3.63% on the day and 4.38% over the past week. The year to date share price return of 8.34% sits alongside a 1 year total shareholder return of 41.48%, which suggests that while recent momentum may have cooled, longer term holders have still seen strong value from price gains and distributions.

If CareTrust REIT’s performance has you reassessing your watchlist, this is a good moment to broaden your search and check out 20 top founder-led companies

With CareTrust REIT trading at $39.34, a value score of 4, and an implied discount both to analyst targets and some intrinsic estimates, the key question is whether this signals a buying opportunity or whether markets are already pricing in future growth.

Price-to-Earnings of 27.7x: Is it justified?

On a P/E of 27.7x, CareTrust REIT sits at a level that suggests investors are already paying a premium for each dollar of current earnings compared with some peers, even though the stock sits below some fair value estimates.

The P/E ratio compares the current share price with earnings per share and is widely used for profitable, income focused real estate companies like CareTrust REIT. With earnings growth of 106.7% over the past year and a 5 year earnings growth rate of 47% per year, a higher multiple can sometimes indicate that the market is willing to pay up for what it sees as quality or consistency in earnings rather than just current income.

Relative to its peers, the picture is mixed. CareTrust REIT trades on a P/E of 27.7x, which is below the peer average of 53.3x cited in one comparison, yet above the Global Health Care REITs industry average of 21.5x in another. Against an estimated fair P/E of 38x, the current 27.7x level sits well under the ratio that regression analysis suggests the stock could move toward if market views aligned with that fair benchmark.

Result: Price-to-Earnings of 27.7x (UNDERVALUED)

However, you also need to weigh tenant health and sector specific policy or reimbursement changes, which could quickly challenge the current valuation story.

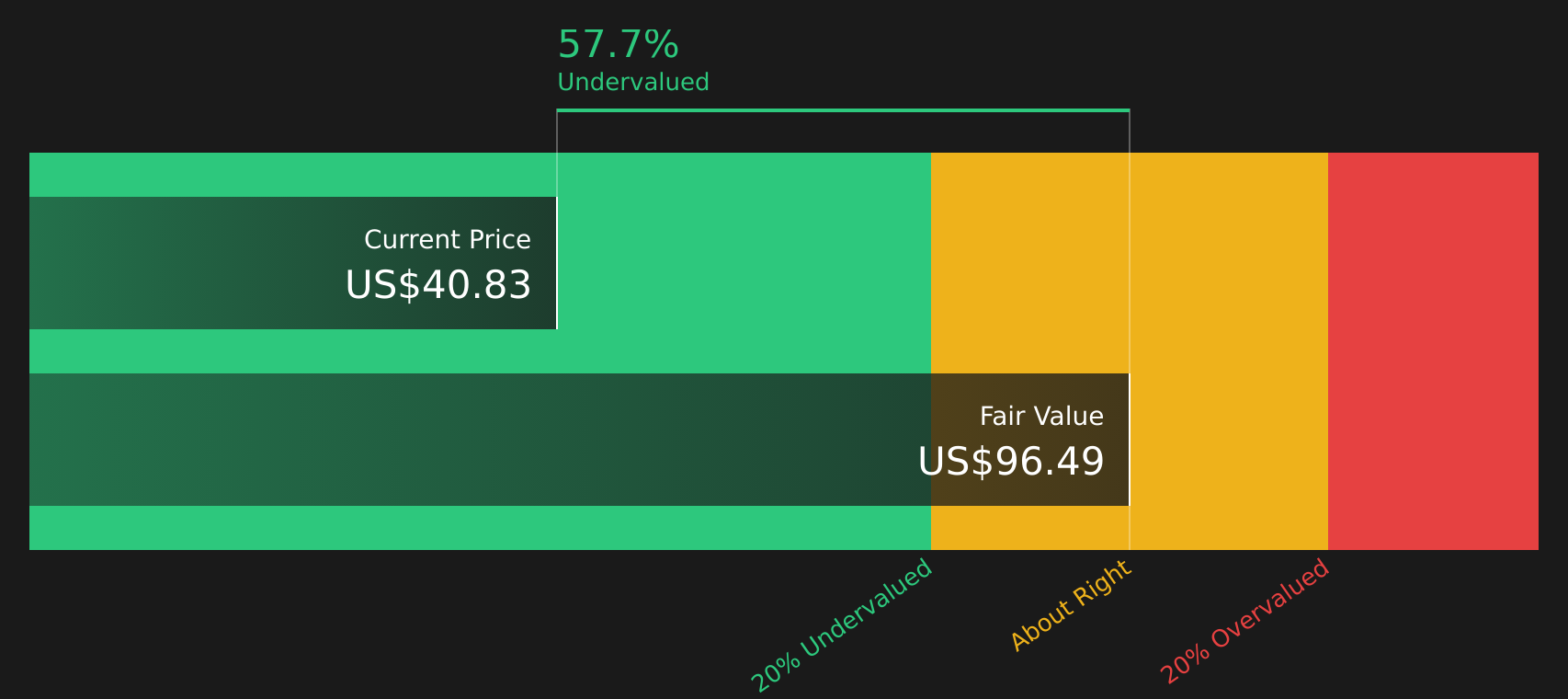

Another view: Cash flows paint a different picture

While the P/E of 27.7x points to potential undervaluation against some benchmarks, the SWS DCF model suggests a much larger gap, with an estimated future cash flow value of $83.18 compared with the current $39.34 share price. That signals a very wide margin, but it is important to consider how comfortable you are with the assumptions behind it.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CareTrust REIT for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Does this mix of potential upside and flagged concerns line up with your own view, or raise new questions for you as an investor? Take a closer look at the underlying data, move quickly to test your thesis, and ground your stance in the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If CareTrust REIT has sharpened your focus, do not stop here. Broaden your opportunity set now so you are not relying on just one stock story.

- Target potential mispricings by scanning companies that combine quality with attractive valuations through the 47 high quality undervalued stocks

- Lock in potential income ideas by reviewing stocks with higher yields using the 10 dividend fortresses

- Prioritise resilience by searching companies with stronger financial footing via the solid balance sheet and fundamentals stocks screener (45 results)

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.