Assessing CAVA Group (CAVA) Valuation As Short Interest Climbs And Sentiment Shifts

CAVA Group, Inc. CAVA | 79.63 | -0.64% |

Short interest in CAVA Group (CAVA) has risen, with 16.79% of the float now sold short, an 8.46% move since the last report. This level puts the stock above many peers on this metric.

The latest share price of US$67.37 comes after a 39.77% 90 day share price return, even though the 1 year total shareholder return is a 48.30% loss. This suggests that recent momentum contrasts with the longer term picture as short interest builds.

If CAVA's sharp swings have you thinking about where else growth stories might emerge, this is a good moment to broaden your search with our list of 22 top founder-led companies.

With short interest climbing and the share price sitting around US$67.37 after a sharp 90 day rebound, you have to ask: is CAVA still mispriced, or is the market already baking in most of the growth story?

Most Popular Narrative: 5.4% Undervalued

With CAVA Group’s fair value estimate at $71.20 versus a last close of $67.37, the most followed narrative sees some upside still on the table.

Rapid geographic expansion into new and underserved markets, supported by strong new unit performance and a robust target of at least 1,000 restaurants by 2032, is likely to accelerate systemwide sales and drive higher topline revenue growth.

Read the complete narrative. Read the complete narrative.

Curious what kind of revenue ramp, profit margins, and future earnings multiple have to line up to justify that fair value gap and the current P/E? The full narrative lays out those moving parts in detail, including how fast the top line would need to grow and how much profitability could compress while still supporting today’s price.

Result: Fair Value of $71.20 (UNDERVALUED)

However, the story can change quickly if aggressive expansion toward 1,000 locations strains returns, or if softer same restaurant sales and margin pressure persist longer than expected.

Another View: Rich P/E Sends a Different Signal

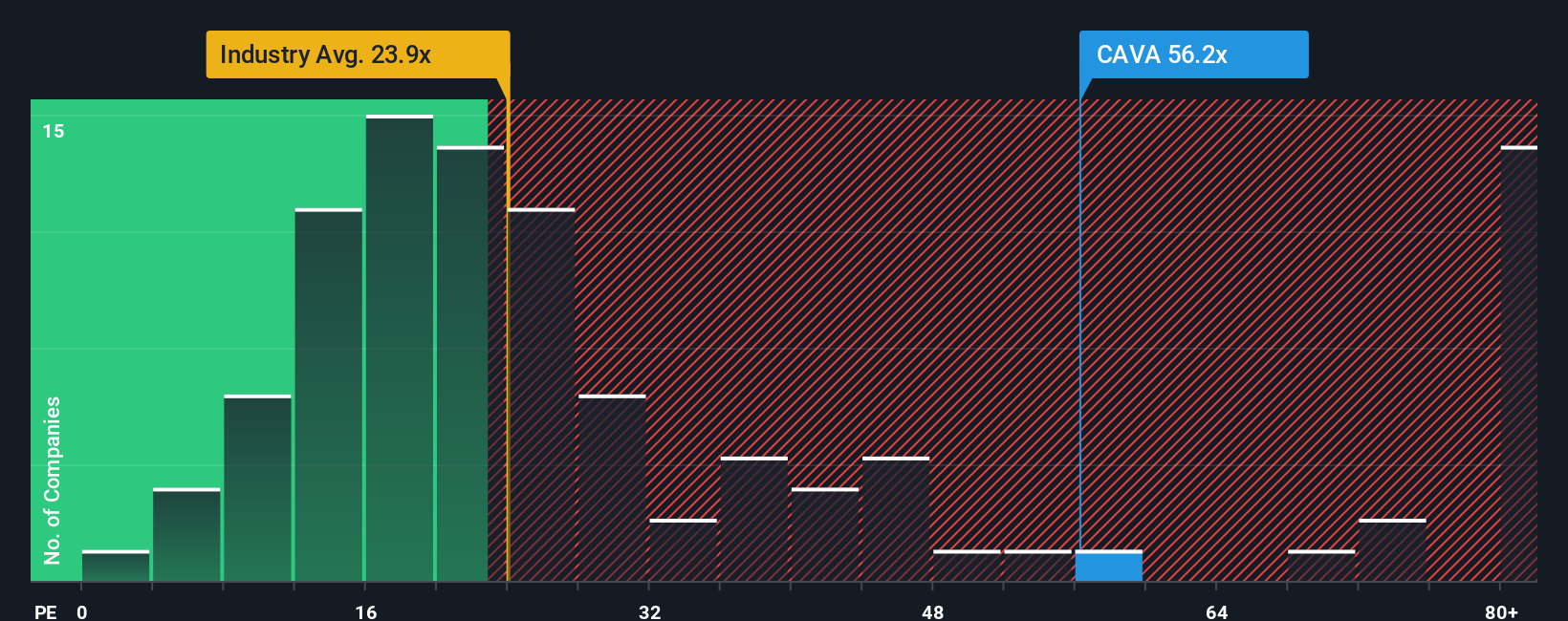

That 5.4% gap between fair value of $71.20 and the current $67.37 sounds modestly supportive, but the current P/E of 56.9x tells a tougher story. It sits well above the US Hospitality average of 21.7x, the peer average of 49.8x, and a fair ratio of 19.5x. This points to a lot of optimism already in the price and raises the question of how much upside is really left if sentiment cools.

Build Your Own CAVA Group Narrative

If this version of the story does not quite fit how you see CAVA, you can stress test the same data yourself and build a fresh view in just a few minutes, then Do it your way.

A great starting point for your CAVA Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready to hunt for your next idea?

If CAVA has you thinking more broadly about where to put fresh capital to work, do not stop here. Widen your search and compare multiple angles.

- Target potential value opportunities by scanning our list of 51 high quality undervalued stocks that combine solid fundamentals with prices that may sit below their estimated fair value.

- Prioritise durability by checking out a solid balance sheet and fundamentals stocks screener (45 results) so you can focus on companies with stronger financial footing and fewer balance sheet red flags.

- Spot early stage stories with punch by reviewing a curated set of 28 elite penny stocks with strong financials that already show healthier financial characteristics than many low priced names.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.