Assessing Centuri Holdings (CTRI) Valuation After Record Backlog Vision One Plan And Icahn Capital Support

Centuri Holdings, Inc. CTRI | 0.00 |

Centuri Holdings (CTRI) recently filed a shelf registration for up to 3,488,372 common shares, representing about US$110.5 million. This filing puts potential future equity issuance on the radar for current and prospective shareholders.

Despite the shelf registration and recent pullback, with the share price down 9.38% over the last week and 5.47% over the last month, Centuri’s 21.19% year to date share price return and 60.13% 1 year total shareholder return suggest that momentum has built as investors respond to its record backlog, Vision One Centuri plan and increased interest from Icahn Capital.

If this kind of infrastructure story has your attention, it could be a good moment to broaden your search and check out 38 power grid technology and infrastructure stocks

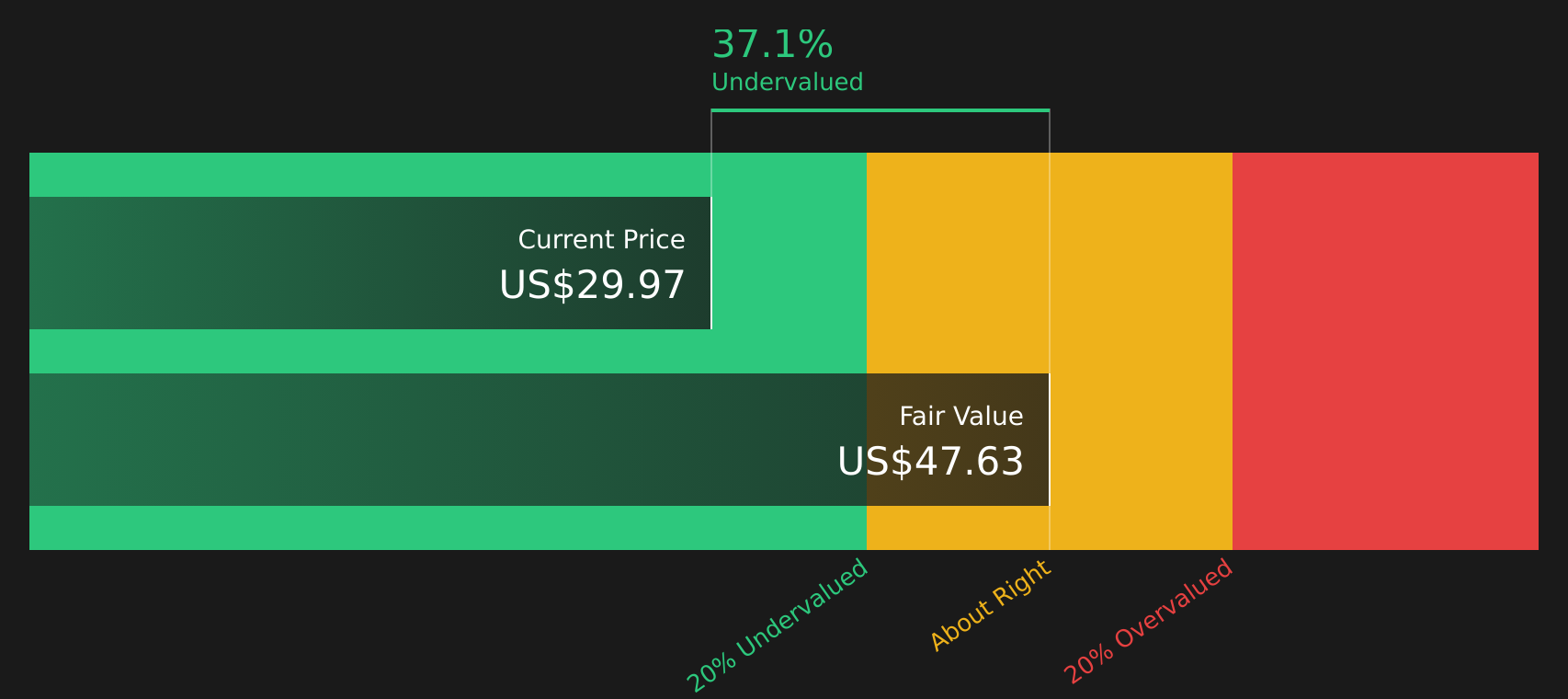

With Centuri trading at US$31.29 and sitting at a discount to both analyst targets and one intrinsic value estimate, the key question is whether this signals an undervalued setup or whether the market already reflects its future growth.

Most Popular Narrative: 28.6% Overvalued

Centuri’s last close at $31.29 sits well above the most followed narrative fair value of $24.33, putting the current price at odds with that framework.

In order for you to agree with the analysts, you'd need to believe that by 2028, revenues will be $3.7 billion, earnings will come to $123.6 million, and it would be trading on a PE ratio of 23.1x, assuming you use a discount rate of 9.7%.

Want to see what sits behind that earnings jump, margin shift and lower future P/E multiple the narrative leans on, without guessing the numbers yourself?

Result: Fair Value of $24.33 (OVERVALUED)

However, if Centuri converts more of its US$5.9b backlog and US$13b pipeline into higher margin work and improves leverage, this overvaluation narrative could face pressure.

Another View: Cash Flows Point a Different Way

While the popular narrative tags Centuri as 28.6% overvalued at a fair value of $24.33, our DCF model points the other way. It shows an estimated future cash flow value of $47.13 versus the current $31.29 share price, which frames the stock as trading at a sizable discount instead.

This kind of gap between an earnings based fair value and a cash flow based fair value raises a clear question: which yardstick do you think better fits a utility infrastructure business like Centuri?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Centuri Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals between fair value estimates and strong recent share price performance, it makes sense to move quickly and test the data for yourself. To weigh up both the concerns and the potential upside in one place, start with these 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Centuri has sharpened your focus, do not stop here. Use the screener to spot other stocks that fit your style before those opportunities move away.

- Target quality at a discount by reviewing companies flagged in 50 high quality undervalued stocks that pair appealing prices with solid underlying metrics.

- Prioritize resilience by scanning 66 resilient stocks with low risk scores for stocks that score well on financial strength and risk controls.

- Hunt for potential future standouts using the screener containing 22 high quality undiscovered gems that most investors may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.