Assessing Citigroup (C) Valuation As Jane Fraser’s Pay Rise Follows Record Revenue And Peer Outperformance

Citigroup Inc. C | 129.58 129.58 | +2.61% 0.00% Post |

Why Jane Fraser’s pay rise matters for Citigroup (C) shareholders

Citigroup (C) has drawn fresh investor attention after lifting CEO Jane Fraser’s compensation to $42 million for 2025, a move the board links directly to record revenue and a 13% rise in net income.

The decision, which brings Fraser’s pay close to that of top peers at rival banks, puts a spotlight on how Citi is tying leadership rewards to market performance and recent financial achievements.

Citigroup’s 7 day share price return of 9.6% decline and year to date share price return of 6.6% decline contrast with a 90 day share price return of 10.5% and a 1 year total shareholder return of 34.4%. This suggests longer term momentum remains stronger even as recent news on regulation, capital actions and CEO pay has coincided with some near term volatility around the current US$110.86 share price.

If Citi’s recent swings have you thinking about where capital might work harder, you may want to scan our screener of 23 top founder-led companies as a fresh source of ideas.

With Citi trading around US$110.86, sitting at a 36% discount to one intrinsic value estimate and about 21% below the average analyst target, the key question is whether this gap signals an opportunity or if the market is already factoring in future growth.

Most Popular Narrative: 4.4% Undervalued

At $110.86, Citi sits a little below the most followed fair value estimate of $116, which is built on long term earnings and margin assumptions rather than short term sentiment.

Investment and momentum in wealth management, especially in high growth regions and with affluent clients, is expanding the fee based revenue stream and improving return on equity, as evidenced by double digit growth in revenues, net new assets, and margins in recent quarters.

Curious what supports that $116 figure? The narrative leans heavily on steady revenue gains, firmer margins and a valuation multiple that assumes Citi keeps compounding those improvements.

Result: Fair Value of $116 (UNDERVALUED)

However, this depends on Citi keeping pace with digital competitors and managing ongoing regulatory and restructuring costs, which could pressure margins and weaken the current undervaluation case.

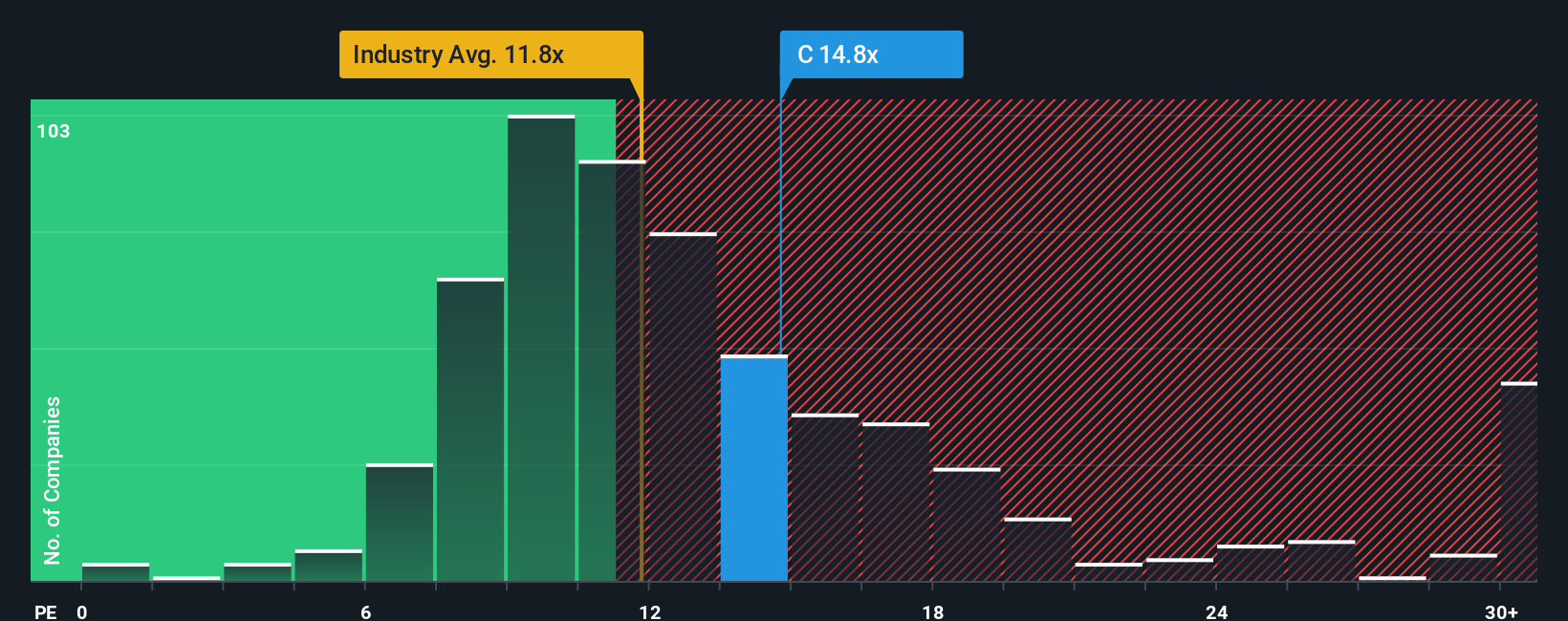

Another Take: P/E Raises a Question Mark

Those fair value estimates leaning toward undervaluation run into a reality check when you look at Citi’s P/E of 14.9x. That sits above both the US Banks industry at 11.9x and its peer average of 13.1x, even though our fair ratio suggests the market could settle closer to 17.2x.

In practical terms, you are paying a premium to the sector and peers today, while still sitting below the fair ratio. That mix of upside potential and valuation risk puts the onus back on you. Do you think Citi’s earnings quality and progress justify paying more than the typical bank?

Build Your Own Citigroup Narrative

If you are not fully on board with this view, or simply prefer to test the numbers yourself, you can build a personalised thesis in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Citigroup.

Looking for more investment ideas?

If Citi has sharpened your focus on where your next dollar should go, do not stop here. Broaden your watchlist with ideas that fit your style.

- Target value first, using our screener of 53 high quality undervalued stocks that combines quality fundamentals with prices that may not fully reflect them.

- Prioritise resilience, with a filter pinpointing 85 resilient stocks with low risk scores that may suit investors who want a calmer ride.

- Hunt for tomorrow’s standouts, by scanning a screener containing 23 high quality undiscovered gems that the crowd may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.