Assessing Clover Health Investments (CLOV) Valuation After Its Recent Share Price Momentum

Clover Health CLOV | 0.00 |

Clover Health Investments (CLOV) has recently drawn attention after a strong share price move, with the stock up 16% over the past week and about 58% over the past month.

That sharp 16.43% 1 day share price return and 58.33% 30 day share price return come on top of a 73.44% year to date share price return and a very large 3 year total shareholder return. This pattern suggests momentum has been building recently as investors reassess growth potential and risk.

If Clover Health’s surge has you thinking about where else capital is moving in healthcare, it could be a good moment to scout other potential opportunities in 35 healthcare AI stocks

With the stock trading at US$4.18 against an average analyst price target of US$3.15 and an estimated intrinsic value gap of about 87%, the key question is whether there is still a buying opportunity or if markets are already pricing in potential future growth.

Most Popular Narrative: 48.4% Overvalued

With Clover Health Investments at $4.18 against a narrative fair value of $2.82, the gap is hard to ignore and it raises questions about how much optimism is already in the price.

The analysts have a consensus price target of $2.82 for Clover Health Investments based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $3.2, and the most bearish reporting a price target of just $2.5.

Curious what kind of revenue ramp, margin shift and future earnings multiple need to line up to justify that fair value, plus the discount rate behind it.

Result: Fair Value of $2.82 (OVERVALUED)

However, there are still clear watchpoints, including rising medical and pharmacy utilization that could pressure margins, and ongoing GAAP net losses that keep the path to profitability uncertain.

Another Way To Look At The Valuation

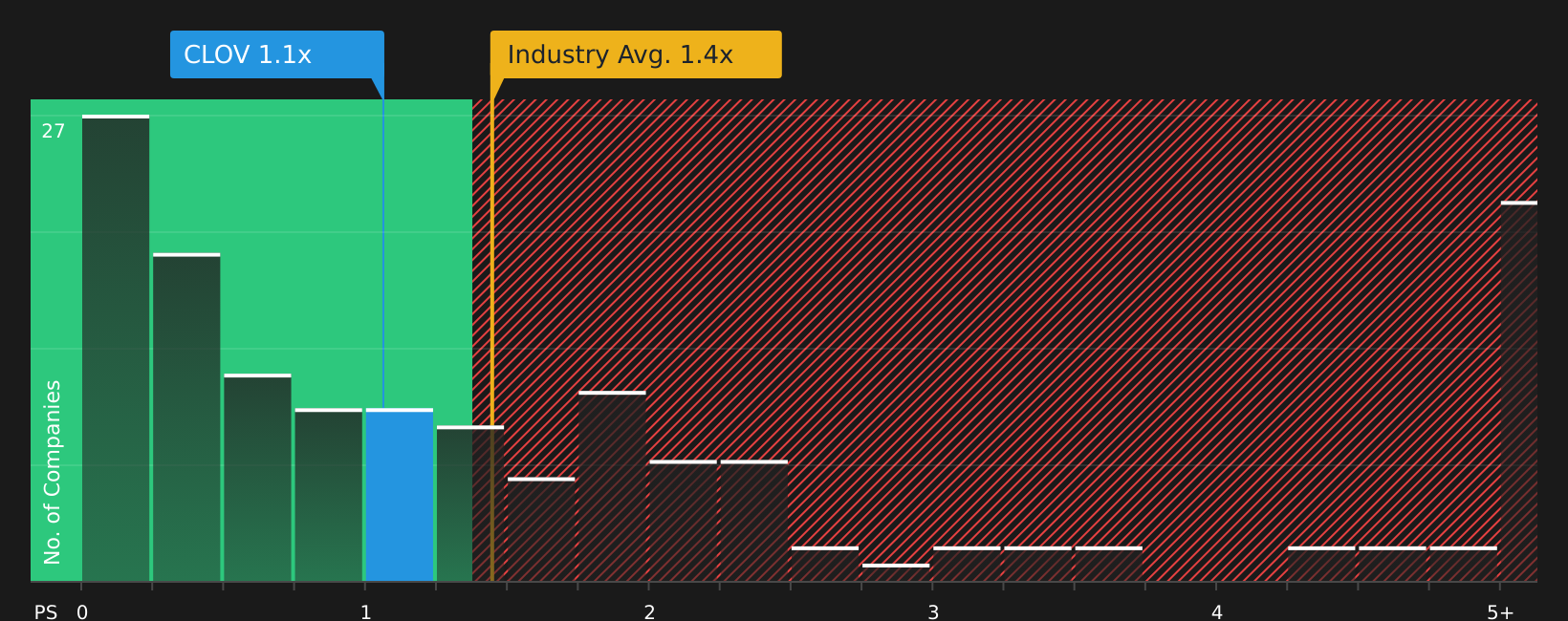

The analyst narrative flags Clover Health Investments as about 48.4% overvalued against a fair value of US$2.82. Yet the stock trades on a P/S ratio of roughly 1x compared with 1.2x for the US Healthcare sector and 2.1x for peers, while sitting near its own fair ratio of 1x. The key question is whether the real tension lies between sentiment around future profits and what current sales already justify.

Next Steps

With sentiment clearly split between risks and rewards, this is a good moment to look through the data yourself and decide what feels justified for your portfolio, then weigh up the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If Clover Health has sharpened your focus, do not stop here. Widen your watchlist now so you are not late to the next opportunity.

- Spot potential value early by scanning 23 elite penny stocks with strong financials that combine smaller market caps with stronger financial profiles than many would expect.

- Target quality at a reasonable price by reviewing the 46 high quality undervalued stocks that already pair healthier cash flows with sturdier balance sheets.

- Prioritize resilience by checking 64 resilient stocks with low risk scores where companies score better on financial strength and risk metrics than the wider market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.