Assessing CNH Industrial (CNH) Valuation After Tweedy Browne’s 52% Stake Increase

CNH Industrial NV CNH | 10.65 | -3.36% |

Tweedy Browne’s nearly 52% increase in its CNH Industrial (CNH) position in the fourth quarter of 2025 is putting fresh attention on the stock, as investors consider what heavier institutional ownership might indicate.

That buying activity has coincided with strong recent momentum in CNH Industrial’s share price, with a 1-day share price return of 6.6% and a 30-day share price return of 23.9%. At the same time, the 1-year total shareholder return is a 3.1% decline, which suggests sentiment has improved in the short term while longer term holders have seen more modest results.

If Tweedy Browne’s move has you thinking beyond a single name, this could be a good moment to scan other auto and machinery names through auto manufacturers.

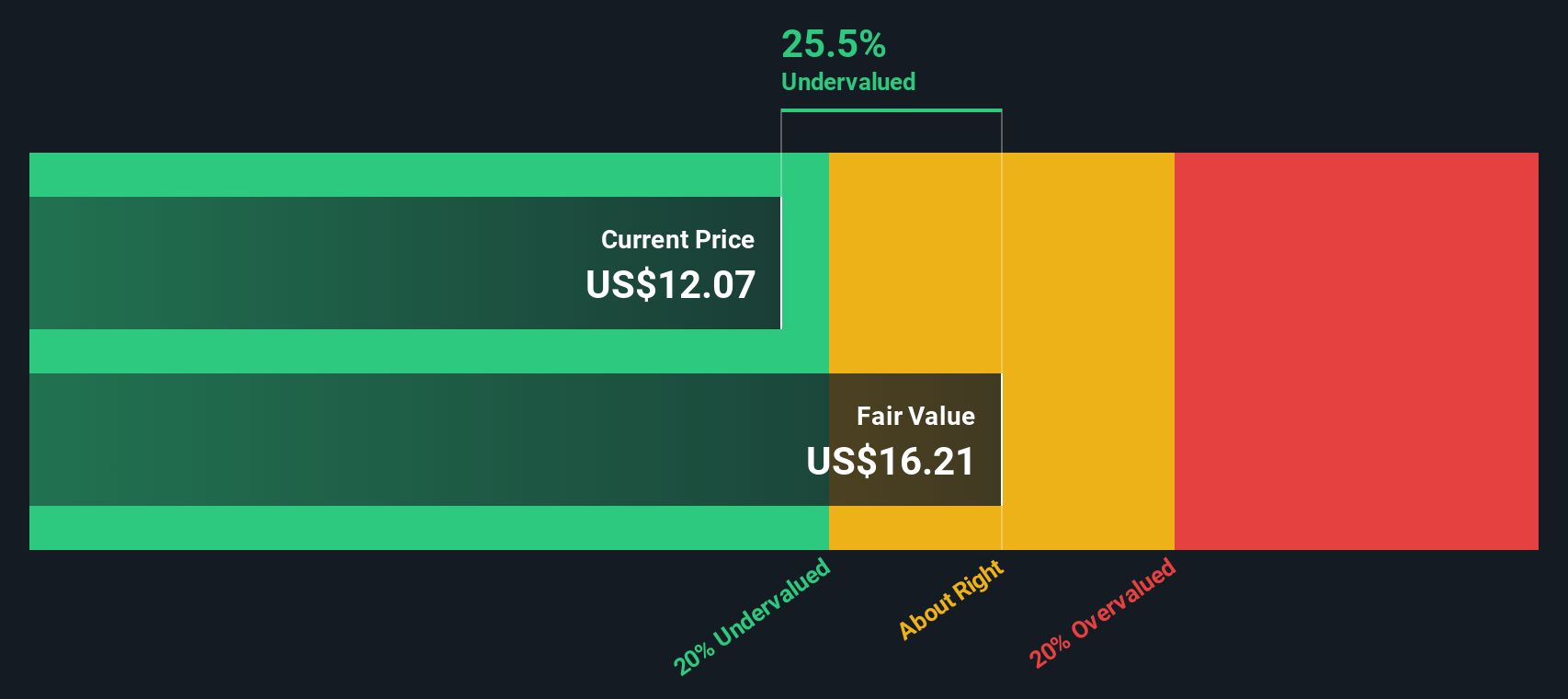

With CNH Industrial trading at US$11.96 against an average analyst price target of US$12.81 and a mixed return profile, you have to ask yourself: is there real value left here, or is the market already pricing in future growth?

Most Popular Narrative: 6.6% Undervalued

CNH Industrial’s fair value in the most followed narrative sits at $12.81, slightly above the last close at $11.96, which frames the current debate.

The integration of advanced connectivity and precision technologies (e.g., the Starlink partnership, FieldOps platform, in-house tech stack) positions CNH to capture greater recurring, higher-margin revenue streams from software, data, and tech-enabled services, supporting net margin and long-term earnings growth.

Curious how modest top line assumptions, rising margins and a re rated profit multiple combine into that fair value? The full narrative walks through the earnings bridge step by step.

Result: Fair Value of $12.81 (UNDERVALUED)

However, the bullish case still faces real pressure from tariff costs and a heavy reliance on a soft North American agricultural market. Both factors could keep margins under strain.

Another View: Cash Flows Paint A Tougher Picture

While the most followed narrative points to CNH Industrial trading about 6.6% below a fair value of $12.81, our DCF model tells a different story. On that cash flow view, CNH screens as overvalued at $11.96 versus an estimated value of about $6.30.

The gap between these two methods raises a practical question for you as an investor: do you lean more on earnings based targets that look closer to the current price, or on cash flow assumptions that suggest a wider margin of valuation risk?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CNH Industrial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 859 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own CNH Industrial Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can build a custom view in just a few minutes with Do it your way.

A great starting point for your CNH Industrial research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If CNH Industrial has sharpened your thinking, do not stop here. Broaden your watchlist with focused stock ideas that match the themes you care about most.

- Target reliable income by checking out these 11 dividend stocks with yields > 3% that may suit a portfolio built around regular cash payouts.

- Spot potential growth stories early by reviewing these 3535 penny stocks with strong financials that still trade at lower share prices but have stronger financial footing.

- Lean into long term tech trends by scanning these 29 AI penny stocks that are connected to artificial intelligence themes across different industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.