Assessing CNH Industrial (NYSE:CNH) Valuation As The Pune Plant Spotlight Shapes Its Growth Story

CNH Industrial NV CNH | 10.65 | -3.36% |

Pune plant spotlight and why it matters for CNH Industrial (NYSE:CNH) shareholders

CNH Industrial (NYSE:CNH) recently put its Pune, India manufacturing plant in the spotlight, underscoring its farm mechanisation capabilities, tailored equipment for local conditions, and contribution to skill development and environmentally aligned operations.

The facility’s role in supplying agricultural machinery to both Indian and international markets adds useful context if you are weighing CNH’s global footprint against its recent share performance and current earnings profile.

At a share price of $12.75, CNH Industrial’s recent Pune spotlight comes as the stock has shown strong short term momentum, with a 30 day share price return of 17.73% and a 1 year total shareholder return of 1.39%. However, the 3 year total shareholder return of a 16.85% decline highlights that longer term holders have had a very different experience.

If this focus on farm equipment and manufacturing has your attention, it could be a good moment to broaden your watchlist with 25 power grid technology and infrastructure stocks as another way to look at infrastructure exposed businesses.

So with CNH shares up sharply over the past quarter and trading close to the average analyst target of $12.87, is the recent momentum still leaving room for upside, or is the market already pricing in future growth?

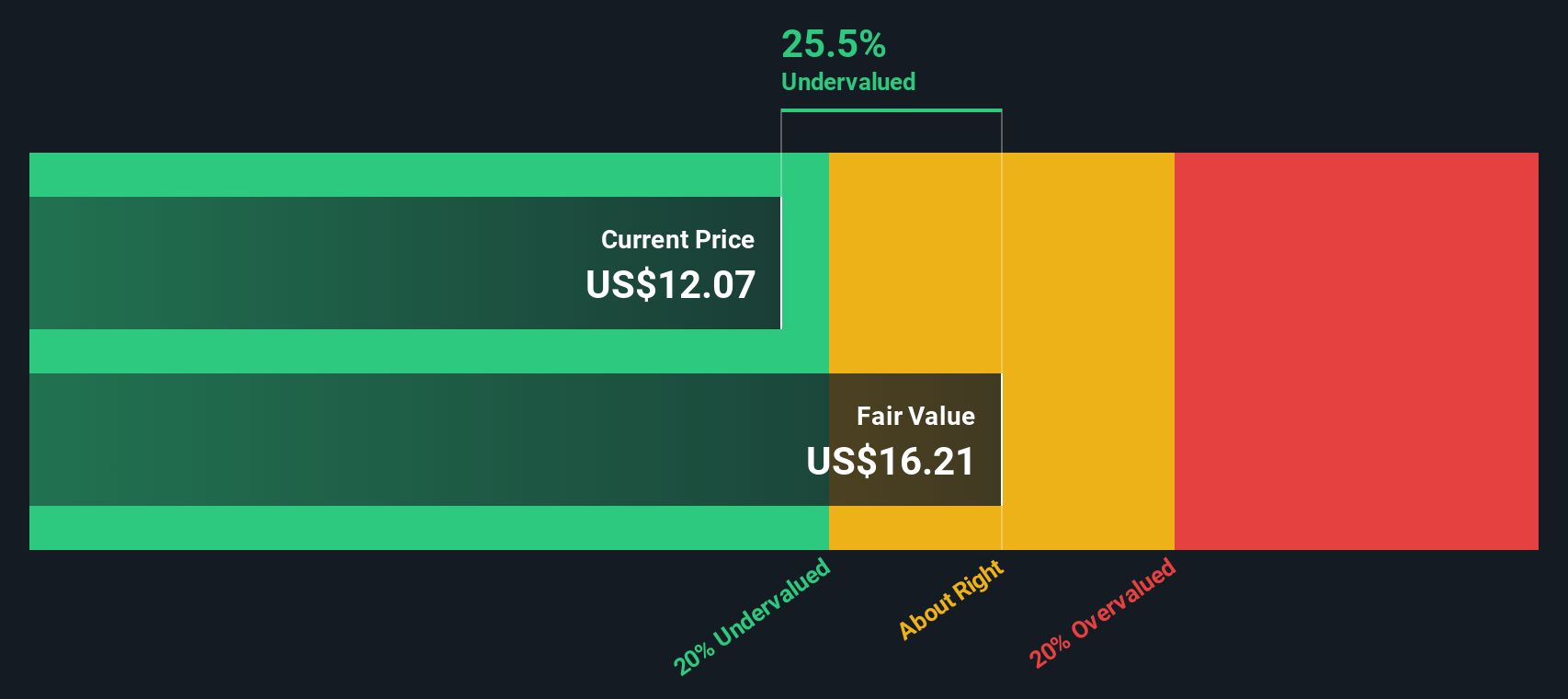

Most Popular Narrative: 0.5% Undervalued

CNH Industrial’s most followed narrative pegs fair value at $12.81, almost in line with the latest close at $12.75, which puts extra focus on the assumptions behind that small discount.

The integration of advanced connectivity and precision technologies (e.g., the Starlink partnership, FieldOps platform, in house tech stack) positions CNH to capture greater recurring, higher margin revenue streams from software, data, and tech enabled services, supporting net margin and long term earnings growth.

Read the complete narrative. Read the complete narrative.

Want to see what is behind that almost one to one fair value call? The narrative leans on steadier top line assumptions, thicker margins, and a future earnings profile that needs only a modest change in the P/E multiple to line up with today’s price.

Result: Fair Value of $12.81 (ABOUT RIGHT)

However, there are still clear pressure points, with tariff uncertainty and weaker North American agriculture exposing CNH’s earnings and margins to bumps that could challenge this fair value story.

Another view: earnings growth potential versus DCF caution

While the popular narrative points to CNH Industrial trading roughly in line with a $12.81 fair value, our DCF model presents a very different picture, with an estimate of $5.89. That gap raises a simple question for you: are earnings forecasts too optimistic, or is the cash flow model too strict?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CNH Industrial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own CNH Industrial Narrative

If you feel the market story here does not quite line up with your own view, you can review the same data, test different assumptions, and build a version that fits your thinking in just a few minutes, then Do it your way.

A great starting point for your CNH Industrial research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If CNH has sharpened your thinking, do not stop here. A few targeted stock ideas from focused lists could quickly broaden the opportunities on your radar.

- Target potential mispricings by reviewing companies on our 53 high quality undervalued stocks and see which names line up with your own expectations.

- Strengthen your income shortlist by checking out 13 dividend fortresses that might fit a more regular cash return mindset.

- Prioritise resilience by scanning 85 resilient stocks with low risk scores that put balance sheet strength and risk controls front and center.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.