Assessing Cognizant Technology Solutions (CTSH) Valuation After Guidance Raise And 3Cloud Acquisition

Cognizant Technology Solutions Corporation Class A CTSH | 62.54 | +2.11% |

Cognizant Technology Solutions (CTSH) raised its full year profit and revenue guidance after consistent earnings beats and strong Q3 results, with investors now watching upcoming Q4 numbers and the 3Cloud acquisition for further clarity.

The recent guidance upgrade and 3Cloud acquisition sit against a share price of US$85.26, with a 90 day share price return of 28.52% and a 1 year total shareholder return of 15.03%. This suggests momentum has been building around Cognizant’s AI and cloud focused story.

If Cognizant’s AI push has your attention, it could be a good moment to widen your watchlist with high growth tech and AI stocks that are also leaning into digital infrastructure.

With the shares at US$85.26 and only a small discount to the average analyst target, the key question now is whether Cognizant still trades below its estimated intrinsic value, or if the market is already pricing in future growth.

Most Popular Narrative: 0% Overvalued

With Cognizant shares at US$85.26 against a widely followed fair value near US$85.22, the current price sits very close to that narrative anchor, putting the spotlight on the earnings and multiple assumptions behind it.

The accelerating shift toward digital transformation, particularly cloud migration, agentic automation, and AI-driven process redesign, is expanding Cognizant's total addressable market as enterprises seek partners for end-to-end modernization, supporting both top-line revenue growth and gross margin expansion.

Curious what growth path and profit mix need to hold for that valuation to stack up? The story leans heavily on steadier revenue gains, firmer margins, and a future earnings multiple that sits below many large US IT peers yet still assumes meaningful progress from today.

Result: Fair Value of $85.22 (ABOUT RIGHT)

However, there is still a real chance that AI automates parts of Cognizant’s traditional outsourcing model, or that wage and visa pressures squeeze margins more than expected.

Another View: Earnings Multiple Signals Room To Move

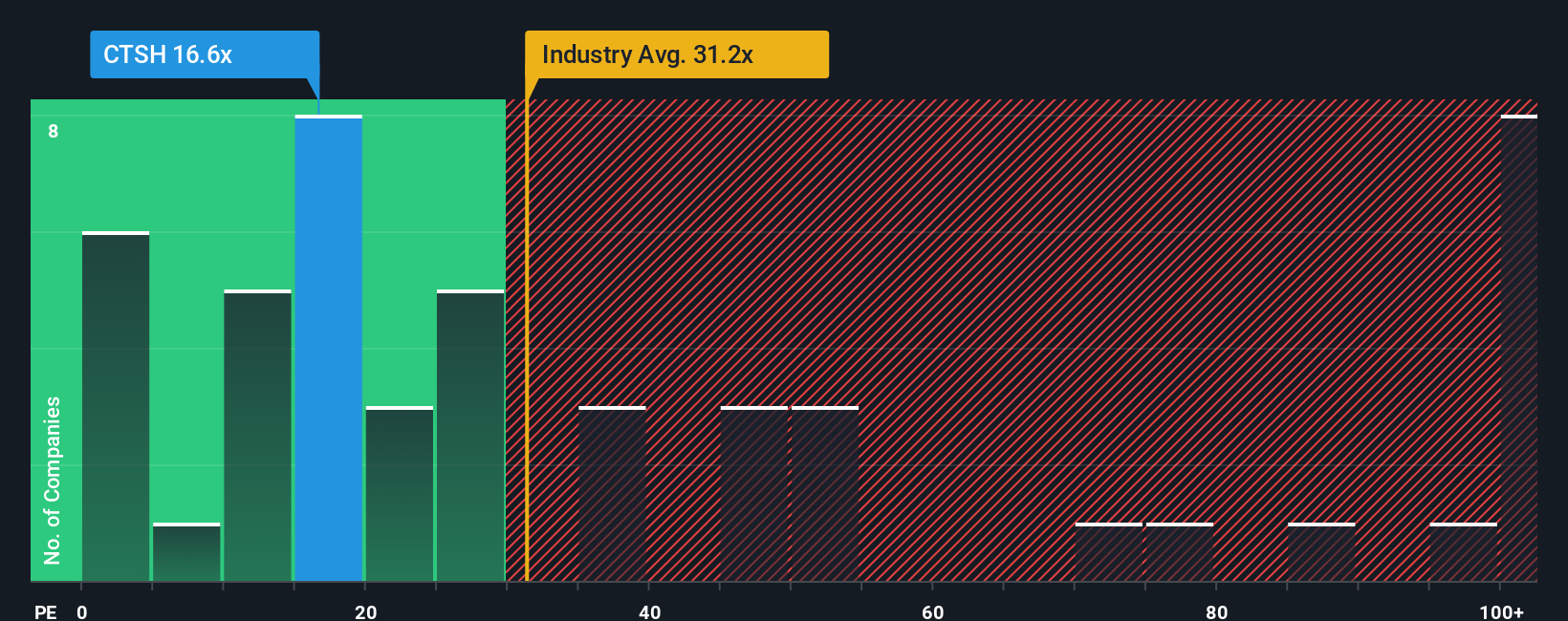

If you focus on the simple earnings multiple, the story looks different. Cognizant trades on a P/E of 19.3x, while the US IT industry sits at 30.9x and close peers average 25.7x. Our fair ratio points to 33x, which is much higher than where the shares are now.

That gap suggests the market is still cautious on Cognizant even after recent momentum. The real question is whether current AI and cloud execution will be enough to close some of that distance, or if this lower multiple sticks around.

Build Your Own Cognizant Technology Solutions Narrative

If you interpret the numbers differently or want to stress test your own assumptions, you can build a custom view in just a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Cognizant Technology Solutions.

Looking for more investment ideas?

If Cognizant is already on your radar, do not stop there. Use the screener to line up fresh ideas now so potential opportunities do not slip past you.

- Spot potential mispricing by scanning these 880 undervalued stocks based on cash flows that align with your own expectations for cash flows and business quality.

- Target next wave AI names by checking out these 28 AI penny stocks that are already tying their business models to real world use cases.

- Position for potential income and growth by reviewing these 12 dividend stocks with yields > 3% that balance yield with fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.