Assessing Commvault Systems (CVLT) Valuation As Geo Shield Targets Sovereign Cloud And Data Security Demand

Commvault Systems, Inc. CVLT | 79.93 | +1.94% |

Why Commvault Geo Shield Matters for CVLT Shareholders

Commvault Systems (CVLT) has introduced Commvault Geo Shield, a data protection offering aimed at customers that need strict control over data location, operational oversight, and encryption keys in cloud environments.

The launch focuses on organizations with sovereign and compliance-driven requirements, adding options such as local and sovereign hyperscaler regions, partner-operated sovereign services, and private sovereign cloud deployments for sensitive workloads.

At a share price of $87.54, Commvault’s 7 day share price return of 7.07% contrasts with a 30 day share price return decline of 29.50% and a 1 year total shareholder return decline of 50.97%. However, the 3 year total shareholder return of 37.79% and 5 year total shareholder return of 25.99% indicate longer term holders have still seen gains, so recent momentum has been fading despite product updates like Geo Shield drawing fresh attention to the story.

If Geo Shield has you thinking about the broader data and AI opportunity, this could be a good moment to check out 59 profitable AI stocks that aren't just burning cash as a starting list of ideas.

With Geo Shield targeting regulated cloud workloads and Commvault shares trading 39% below the average analyst price target, investors now face a key question: is the recent share price drop a buying opportunity, or is future growth already priced in?

Most Popular Narrative: 38% Undervalued

Commvault Systems most followed narrative pegs fair value at about $140.33 per share compared with the last close at $87.54, setting up a wide valuation gap investors will want to understand.

Analysts have reset their price expectations for Commvault Systems, trimming the fair value estimate from about $175 to roughly $140 as they incorporate lower Street price targets, slightly higher discount rates, modestly softer revenue growth assumptions and a reduced future P/E, partly balanced by higher projected profit margins.

Curious what justifies that gap between price and fair value? The narrative leans heavily on healthier margins, steady revenue growth and a premium future earnings multiple to support its case.

Result: Fair Value of $140.33 (UNDERVALUED)

However, there are clear pressure points here, including reliance on large, lumpy deals, as well as the risk that new customer growth lags expansion within the existing base.

Another Angle On CVLT’s Valuation

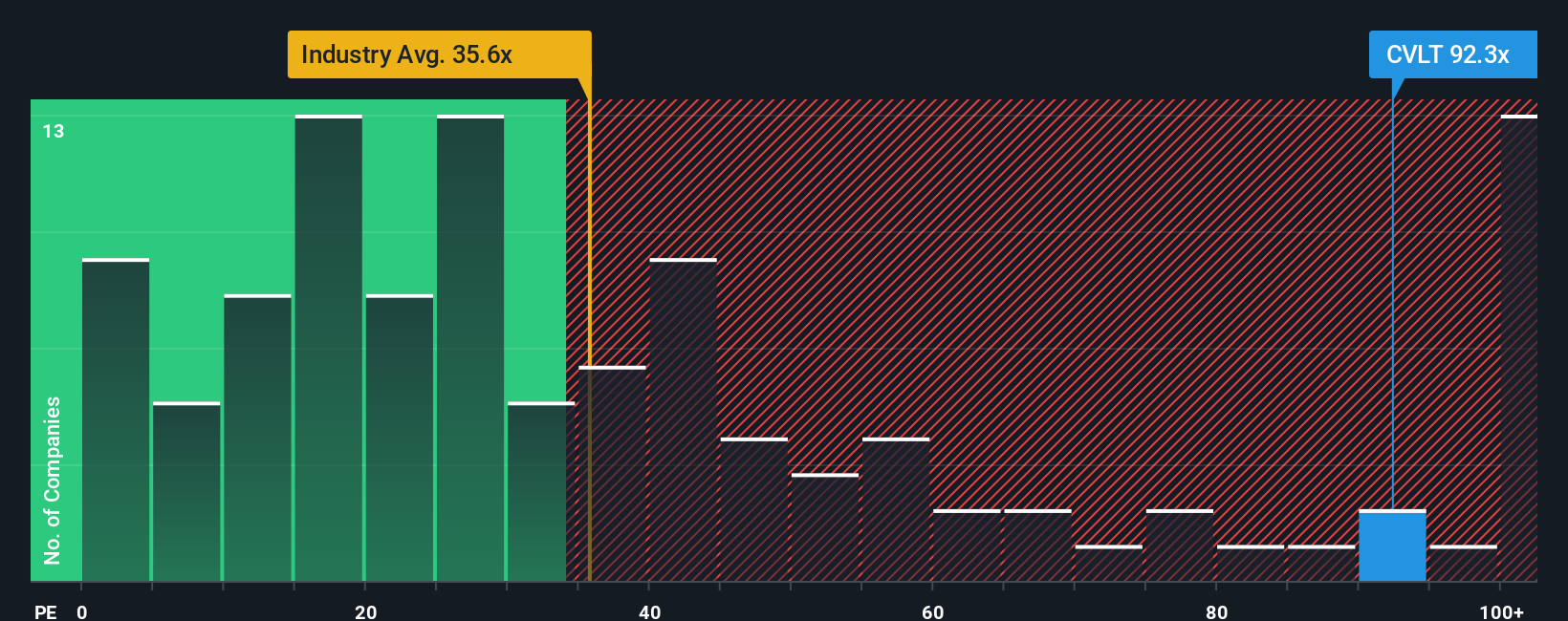

The narrative suggests CVLT is 38% undervalued, but the current P/E of 44.2x tells a different story. That is richer than the US Software industry at 28x, its peer average at 26.5x, and even the fair ratio of 34.1x. This hints at valuation risk if sentiment cools.

Build Your Own Commvault Systems Narrative

If you are not fully on board with this view or simply prefer to rely on your own analysis, you can build a tailored story around the same data in just a few minutes, starting with Do it your way.

A great starting point for your Commvault Systems research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Commvault has sharpened your focus, do not stop here. Broaden your watchlist with other ideas that could fit your style and risk comfort.

- Target value opportunities by reviewing 51 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect them.

- Prioritize resilience by scanning 83 resilient stocks with low risk scores designed to highlight companies with more stable risk profiles.

- Hunt for potential future leaders by checking our screener containing 24 high quality undiscovered gems that many investors may be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.