Assessing Concentra Group Holdings Parent (CON) Valuation After Renewed Focus On Occupational Health Scale And Stability

Concentra Group Holdings Parent, Inc. CON | 20.89 | -1.60% |

Why Concentra Group Holdings Parent (CON) is Back on Investor Radars

Concentra Group Holdings Parent (CON) is drawing fresh attention after management underlined its role in treating about one in four U.S. workplace injuries and operating more than 1,000 locations with stable, employer driven pricing.

At a latest share price of US$20.61, Concentra has seen a 6.18% year to date share price return, with a 5.91% 7 day move suggesting interest has picked up recently even as 1 year total shareholder return sits at 1.06%.

If Concentra has you looking closer at occupational health, this could be a good moment to broaden your research with healthcare stocks that are shaping the sector.

With Concentra reporting US$2.09b in revenue, US$151.47m in net income and trading at US$20.61 with an indicated 10.56% intrinsic discount, the real question is whether you see a mispricing here or a market already banking on future growth?

Most Popular Narrative: 26.7% Undervalued

With Concentra last closing at US$20.61 and the most followed narrative pointing to fair value above that level, the valuation debate is squarely about future earnings power.

The increasing proportion of older Americans is strengthening demand for occupational health, rehabilitation, and preventative services, supporting consistent visit growth and higher revenue per visit, which should sustain long-term revenue and EBITDA growth as aging workforce trends accelerate.

Curious what sits behind this valuation gap? The narrative leans on steady top line expansion, rising profit margins and a future earnings multiple that has to compress to make the math work. Want to see exactly how those moving parts stack up to reach the implied fair value?

Result: Fair Value of $28.13 (UNDERVALUED)

However, there are pressure points to watch, including high leverage at 3.8x net debt to EBITDA and the risk that organic visit growth remains stubbornly low.

Another Angle on Valuation

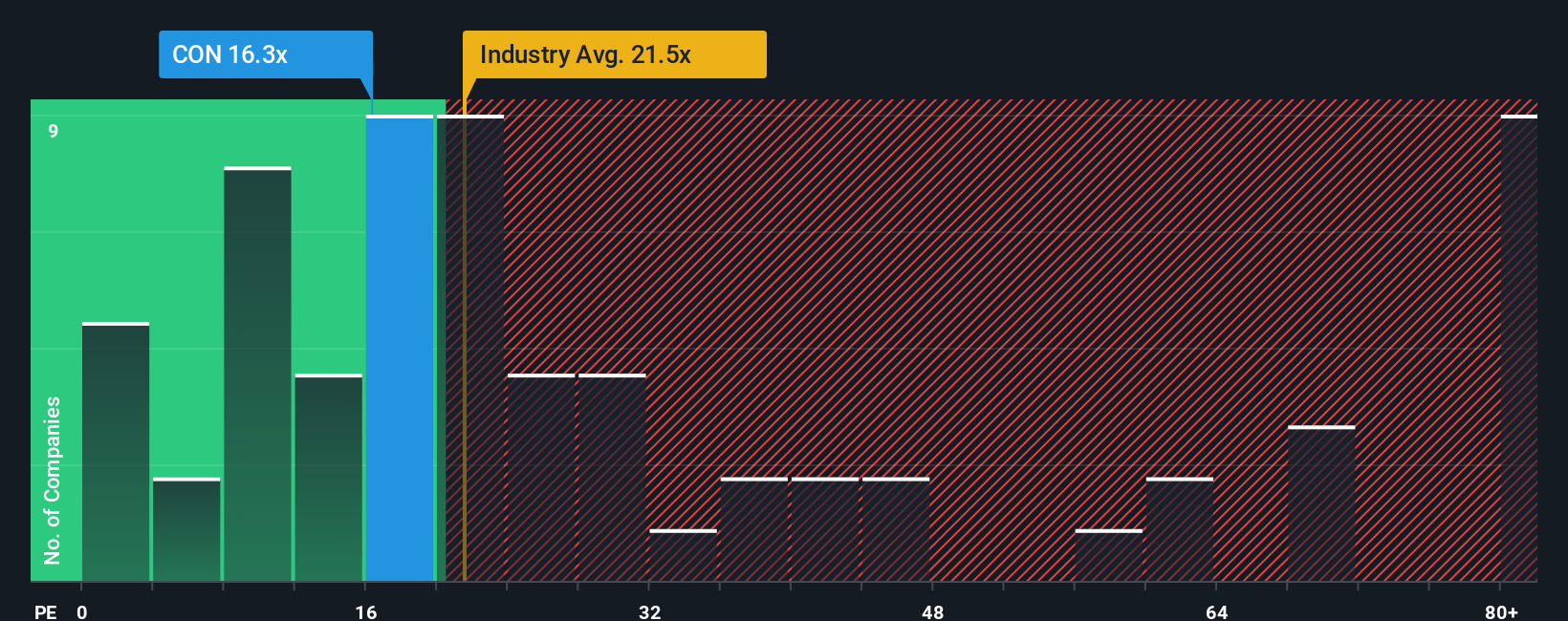

The first narrative leans on future earnings and a fair value of US$28.13, yet the current P/E of 17.4x tells a slightly different story. It sits below the US Healthcare average of 22.9x, but above peer levels at 14.5x and under a fair ratio of 22.3x.

That mix of a lower P/E than the wider industry, a higher P/E than peers and a fair ratio pointing higher suggests both room for re rating and the risk that expectations are already baked in. Which part of that trade off matters more to you at today’s price?

Build Your Own Concentra Group Holdings Parent Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own view against the data, you can build a complete narrative for Concentra in just a few minutes with Do it your way.

A great starting point for your Concentra Group Holdings Parent research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Concentra has sharpened your focus, do not stop here. Broaden your watchlist with targeted ideas so you are not missing opportunities elsewhere.

- Spot potential value by checking out these 881 undervalued stocks based on cash flows that may be trading below what their cash flows imply.

- Zero in on income potential through these 12 dividend stocks with yields > 3% that offer yields above 3%.

- Ride emerging tech themes with these 26 AI penny stocks that sit at the intersection of artificial intelligence and market growth themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.