Assessing Coterra Energy (CTRA) Valuation After Recent Share Price Moves

Coterra Energy CTRA | 0.00 |

Why Coterra Energy is on investors’ radar today

Coterra Energy (CTRA) is drawing fresh attention after recent share price moves, with the stock showing a mix of gains over the past 3 months and some pullback over the past month.

At a share price of US$33.65, Coterra’s recent 2.2% 1 day share price return and 5.3% 7 day share price return contrast with a 3.9% 30 day share price decline. The 1 year total shareholder return of 36.7% and 5 year total shareholder return of 155.99% point to momentum that has built over time but cooled slightly in the very short term.

If this kind of move in an energy name has caught your eye, it can be a good moment to broaden your search and check out 91 nuclear energy infrastructure stocks

Those past returns, recent revenue and profit growth, and a value score of 4 with a reported intrinsic discount of around 64% all raise the same question: Is Coterra still undervalued or is the market already pricing in future growth?

Most Popular Narrative: 31.7% Overvalued

Bejgal’s narrative pegs Coterra Energy’s fair value at $25.55, which sits well below the recent $33.65 close, setting up a clear valuation gap to unpack.

In 3 years, Coterra is likely to solidify its position as a leading energy producer with enhanced capital efficiency and diversified revenue streams. By 5 years, the company could see robust earnings growth driven by the LNG market and efficient oil production. Over 10 years, its extensive inventory and focus on innovation position it for sustainable long-term growth.

Curious how a single LNG driven revenue story, layered with rising margins and a richer earnings multiple, adds up to that fair value gap? The key assumptions sit inside this narrative, including how fast sales might build, how profitability could evolve and what kind of future P/E is being used to justify that price. The details are all laid out if you want to see what is doing the heavy lifting.

Result: Fair Value of $25.55 (OVERVALUED)

However, LNG demand shifts or tighter environmental rules in key regions could quickly challenge the growth story that underpins Bejgal’s higher margin and earnings assumptions.

Another View: Cash Flows Tell a Different Story

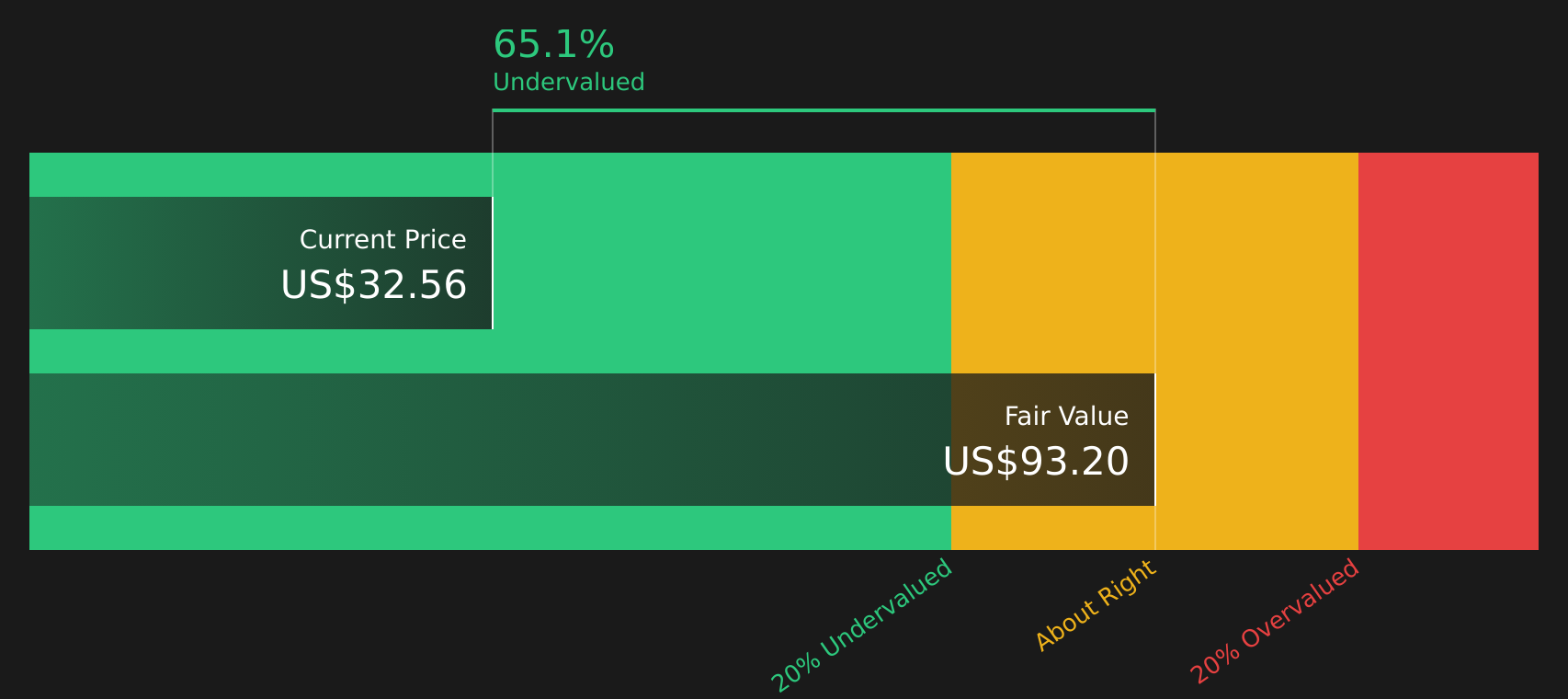

Bejgal’s narrative suggests Coterra looks 31.7% overvalued at a fair value of $25.55, but the SWS DCF model points in the opposite direction. On that cash flow based view, Coterra at $33.65 is trading below an estimated future cash flow value of $93.85, implying the shares are undervalued. For you as an investor, that split between earnings based assumptions and long term cash flow estimates raises a simple question: which number feels more realistic?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Coterra Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 54 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of signals around Coterra can feel split, so it helps to move quickly, review the numbers yourself and weigh up the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Coterra has your attention, do not stop there. Broaden your watchlist with a few focused stock ideas that match the way you like to invest.

- Target income potential by reviewing companies in the 13 dividend fortresses that may appeal if you want yields with a clear focus on payouts.

- Hunt for quality at a fair price by scanning the 54 high quality undervalued stocks and see which names currently line up with your value checklist.

- Prioritise resilience by checking the 74 resilient stocks with low risk scores so you do not miss companies that aim to pair stability with controlled downside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.