Assessing Credo Technology Group Holding (CRDO) Valuation After AI Growth Momentum And Blue Heron Launch

Credo Technology Group Holding Ltd. CRDO | 101.45 | +5.77% |

Blue Heron launch puts Credo’s AI connectivity story in focus

Credo Technology Group Holding (CRDO) has introduced its Blue Heron 224G AI scale-up retimer, a multiprotocol chip built on a 3nm process to support demanding connectivity requirements inside AI data centers.

The product is designed to recover 40+dB 224G links across extended cable and backplane distances using UALink, ESUN and Ethernet, giving data center operators more flexibility in how they place GPUs and switch chips.

The Blue Heron launch lands after a sharp 20.99% 30 day share price decline and a 22.22% share price pullback year to date. At the same time, Credo’s 1 year total shareholder return of 44.15% and very large 3 year total shareholder return above 7x point to longer term momentum that has cooled recently as investors reassess growth expectations and risks around AI data center connectivity.

If Credo’s AI infrastructure story has your attention, this is a good moment to see what else is out there with our screener of 33 AI infrastructure stocks.

With the stock down sharply over the past month but still showing a 44.15% 1 year total return and very large 3 year gains, is Credo now on sale, or is the market already pricing in future growth?

Most Popular Narrative: 48% Undervalued

Credo’s most followed narrative pegs fair value at about $214 per share compared with the recent $111.40 close, framing a wide valuation gap that hinges on aggressive growth and profitability assumptions.

The fair value estimate has risen meaningfully to about $214 from roughly $163, reflecting stronger growth and margin assumptions. The net profit margin has improved to around 34.9% from roughly 31.8%, signaling better anticipated operating leverage and profitability.

Curious what kind of revenue surge and margin profile need to line up to support that gap? The most followed narrative leans on ambitious earnings compounding and a rich future multiple to make the numbers work. It connects those forecasts to Credo’s role in high speed AI data center build outs without assuming everything goes perfectly, but still demands a lot from future execution.

Result: Fair Value of $214 (UNDERVALUED)

However, heavy reliance on a few large cloud customers, along with the risk that AI buildouts reflect pulled forward demand, could quickly challenge those upside assumptions.

Another Angle on Credo’s Valuation

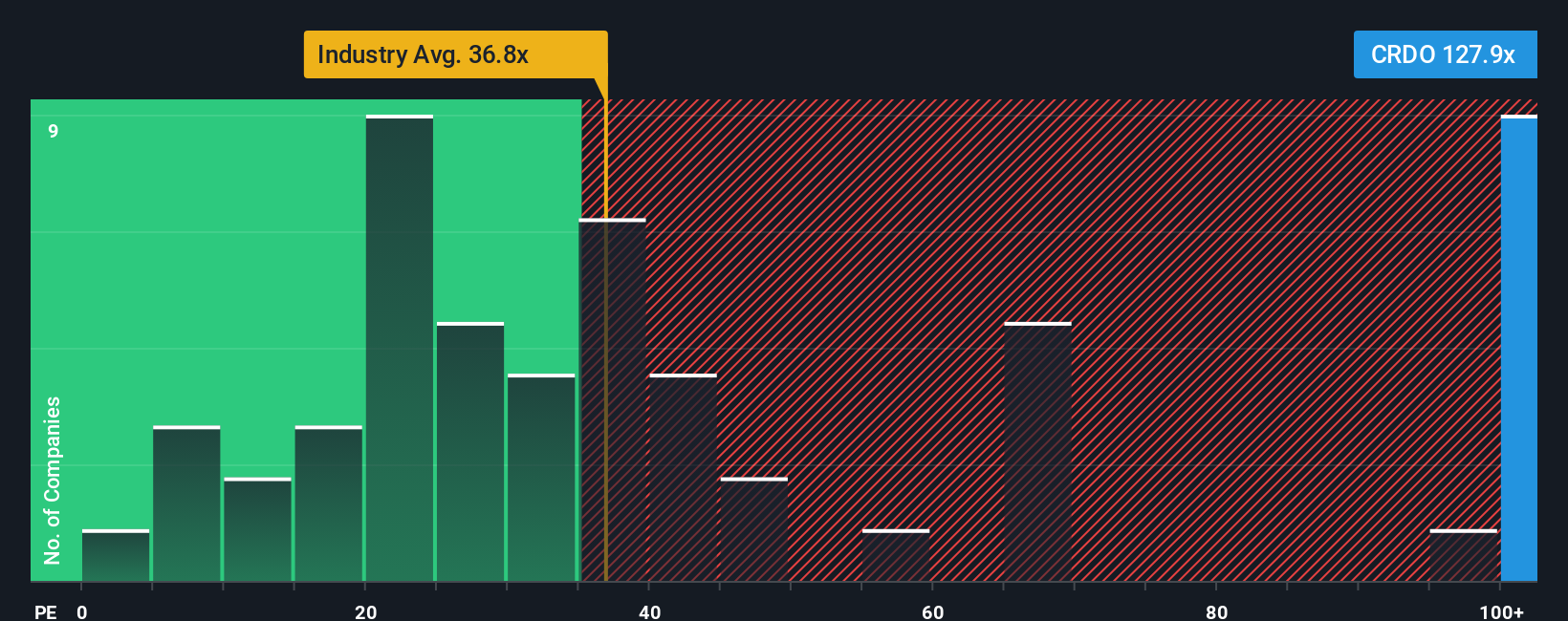

That 48% undervalued narrative leans on rich growth and margin forecasts. On simpler P/E math, though, Credo looks expensive, trading at about 94.9x earnings versus 44x for the US Semiconductor group and a fair ratio of 73.2x. If sentiment cools, the key question becomes whether the multiple compresses first.

Build Your Own Credo Technology Group Holding Narrative

If you see the story differently or just want to test your own assumptions against the data, you can build a custom view in minutes with Do it your way.

A great starting point for your Credo Technology Group Holding research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Credo has sparked fresh questions about your portfolio, do not stop here. Take a few minutes to scout other opportunities before the market moves on.

- Target potential upside by scanning 53 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their underlying business strength.

- Strengthen your income stream by reviewing 14 dividend fortresses built around higher yielding companies with consistent payout profiles.

- Sleep easier by checking 86 resilient stocks with low risk scores designed to highlight companies with more resilient risk scores and steadier business profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.