Assessing CrowdStrike (CRWD) Valuation After Analyst Upgrades And Identity Security Acquisitions

CrowdStrike CRWD | 399.12 | +1.48% |

Recent analyst upgrades and two identity focused acquisitions have put CrowdStrike Holdings (CRWD) back in focus for investors, with attention shifting from short term volatility to the evolution of its broader platform story.

At a share price of $444.62, CrowdStrike’s recent 18.12% 90 day share price pullback and 6.52% 30 day decline sit alongside a 12.03% 1 year total shareholder return and a very large 3 year total shareholder return. This suggests that longer term momentum contrasts with short term volatility as investors weigh identity focused deals, global cloud expansion and shifting risk perceptions after last year’s outage related lawsuit was dismissed.

If CrowdStrike’s recent identity and AI driven moves have your attention, it could be a moment to look across other high growth tech and cybersecurity names through high growth tech and AI stocks for additional ideas.

With the share price at $444.62, recent pullbacks, analyst upgrades and identity focused deals, the key question now is simple: is CrowdStrike still mispriced, or are markets already baking in years of future growth?

Most Popular Narrative: 16.6% Undervalued

Compared to the last close at $444.62, the most followed narrative points to a fair value of $533.26, framing CrowdStrike as meaningfully mispriced on that view.

The strategic focus on Next Gen SIEM, cloud native security, and large scale partnerships, along with CrowdStrike's expansive data capabilities for AI development, is cited as a basis for expectations of robust demand growth, which some believe can drive revenue and contract value higher in future periods.

Curious what kind of growth path would need to play out to support that gap between price and fair value? The narrative referenced here relies on assumptions of faster revenue expansion, rising margins, and a rich future earnings multiple. Interested readers can review the underlying figures behind that story and how they align with the current analyst price target range.

Result: Fair Value of $533.26 (UNDERVALUED)

However, this story can break if newer products and acquisitions fail to gain traction, or if rising competitive pressure in cloud and identity security squeezes margins.

Another View: Rich Sales Multiple Raises A Different Question

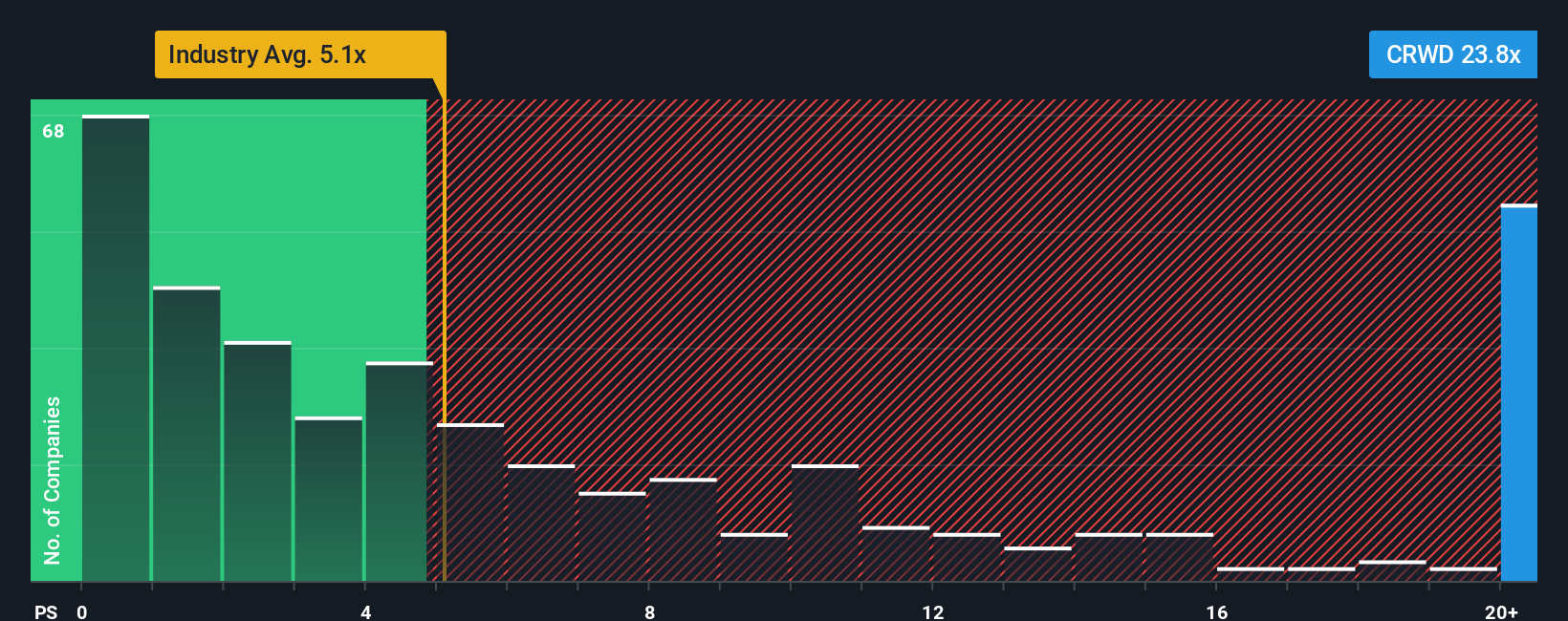

While the popular narrative points to a fair value of $533.26 and an undervalued label, the current P/S of 24.6x tells a different story. It sits well above both the US Software industry at 4.4x and peers at 10.6x, and even the fair ratio of 15.6x suggested by regression work.

That kind of gap can mean investors are already paying upfront for a lot of future execution, which leaves less room for disappointments and can increase valuation risk if expectations change. It leaves you weighing one key question: which signal do you put more weight on right now, the narrative fair value or the rich sales multiple?

Build Your Own CrowdStrike Holdings Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can quickly build a personalised view and Do it your way

A great starting point for your CrowdStrike Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If CrowdStrike has sparked fresh thinking for you, do not stop here. Widen your search now so you are not relying on a single story.

- Hunt for potential high risk high reward opportunities by checking out these 3524 penny stocks with strong financials that already clear basic financial strength filters.

- Spot companies riding the AI wave early by scanning these 24 AI penny stocks that tie real business models to artificial intelligence themes.

- Shift your attention to price and fundamentals by reviewing these 866 undervalued stocks based on cash flows that may offer more downside protection than fast growing names.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.