Assessing Danaher (DHR) Valuation After 2025 Sales Growth But Weaker Earnings

Danaher Corporation DHR | 191.12 | +0.17% |

Danaher (DHR) has released its full year 2025 results, reporting sales of US$24.6b compared to US$23.9b a year earlier, while net income and earnings per share were lower than the prior year.

The full-year update, with sales of US$24.6b alongside lower net income and earnings per share, comes after a mixed price picture. The share price showed a 2.07% 1-day return but has declined 3.03% year to date. Over a longer horizon, total shareholder return has been modest, with a 4.93% 1-year gain and a 5-year total shareholder return of 9.34%. This suggests momentum has been relatively muted compared to shorter-term swings.

If Danaher’s latest earnings have you reassessing healthcare exposure, it could be a good moment to widen the lens and look at healthcare stocks as potential alternatives.

So with revenue at US$24.6b, earnings under some pressure and the share price drifting this year, is Danaher quietly offering value here or are markets already fully pricing in any future growth?

Most Popular Narrative: 15.8% Undervalued

Compared to Danaher’s last close at $223.42, the most followed narrative fair value of about $265.23 points to a valuation gap that hinges on some specific long term assumptions.

The sustained advancement of precision medicine and personalized therapies, including new AI-assisted diagnostic solutions and groundbreaking launches in genomics (like support for in vivo CRISPR therapies), positions Danaher's technology portfolio to capture higher-margin growth and drive long-term EBITDA expansion.

Want to see what is built into that premium for diagnostic tools and bioprocessing, and how earnings, margins and future P/E all fit together? The popular narrative lays out a detailed path for revenue, profitability and the valuation multiple that needs to hold for that fair value to make sense.

Result: Fair Value of $265.23 (UNDERVALUED)

However, this hinges on funding and policy staying supportive. Prolonged weakness in early stage biotech or further reimbursement pressure in China could quickly challenge that view.

Another View: Expensive On Earnings Ratios

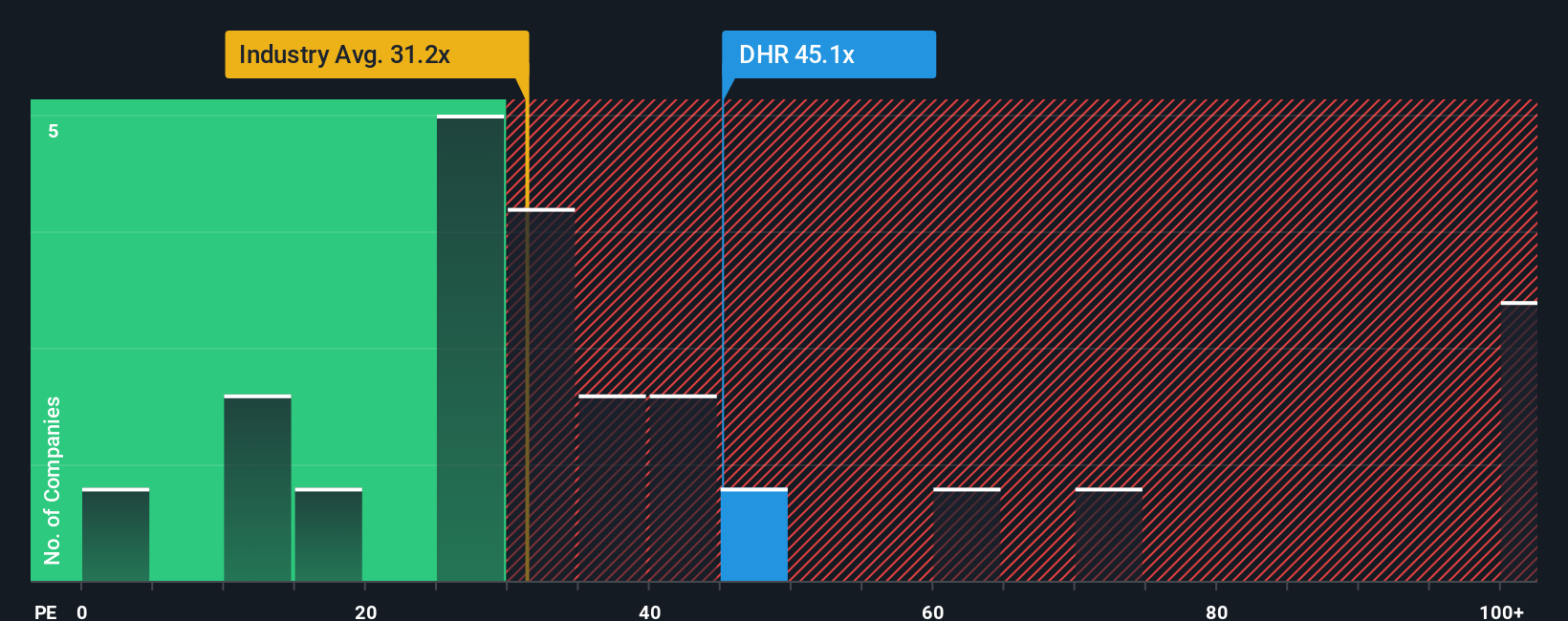

The popular narrative relies on a higher future P/E to argue Danaher looks undervalued, but today the stock trades on a P/E of 43.9x. That is above the North American Life Sciences average of 35.4x, a peer average of 31.7x, and a fair ratio of 32.2x, which points to valuation risk if sentiment cools.

With three different earnings ratios all sitting lower than where Danaher trades now, how comfortable are you paying a higher multiple on the assumption that growth and margins land exactly as modeled?

Build Your Own Danaher Narrative

If you are not fully on board with these views or prefer to stress test the assumptions using your own inputs, you can build a tailored scenario in just a few minutes with Do it your way.

A great starting point for your Danaher research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Danaher has sharpened your thinking, do not stop there. Broaden your watchlist with a few targeted stock ideas that match what you care about most.

- Target potential mispricings by scanning these 876 undervalued stocks based on cash flows that may offer a more attractive entry point based on cash flows.

- Explore developments in growth themes by checking out these 24 AI penny stocks positioned at the intersection of AI and public markets.

- Build a cash flow focused income stream by reviewing these 13 dividend stocks with yields > 3% that exceed a 3% yield threshold.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.