Assessing Datadog (DDOG) Valuation As bullish Analyst Views And New Fund Interest Renew Optimism

Datadog DDOG | 120.36 | +1.42% |

Recent commentary around Datadog (DDOG) has turned more constructive as major brokerages voice bullish views, ClearBridge Investments opens a new position, and the company continues smaller acquisitions to expand its observability services.

At a share price of US$123.46, Datadog has seen a sharp 21.16% 90 day share price decline and a 12.96% 30 day share price drop, even as recent analyst commentary, fund interest and product expansion have started to rebuild confidence. At the same time, the 3 year total shareholder return of 74.50% and 5 year total shareholder return of 25.98% point to a very different longer term picture.

If Datadog’s recent swings have you looking across cloud and AI, this could be a useful moment to scan other high growth tech and AI stocks that fit your own criteria.

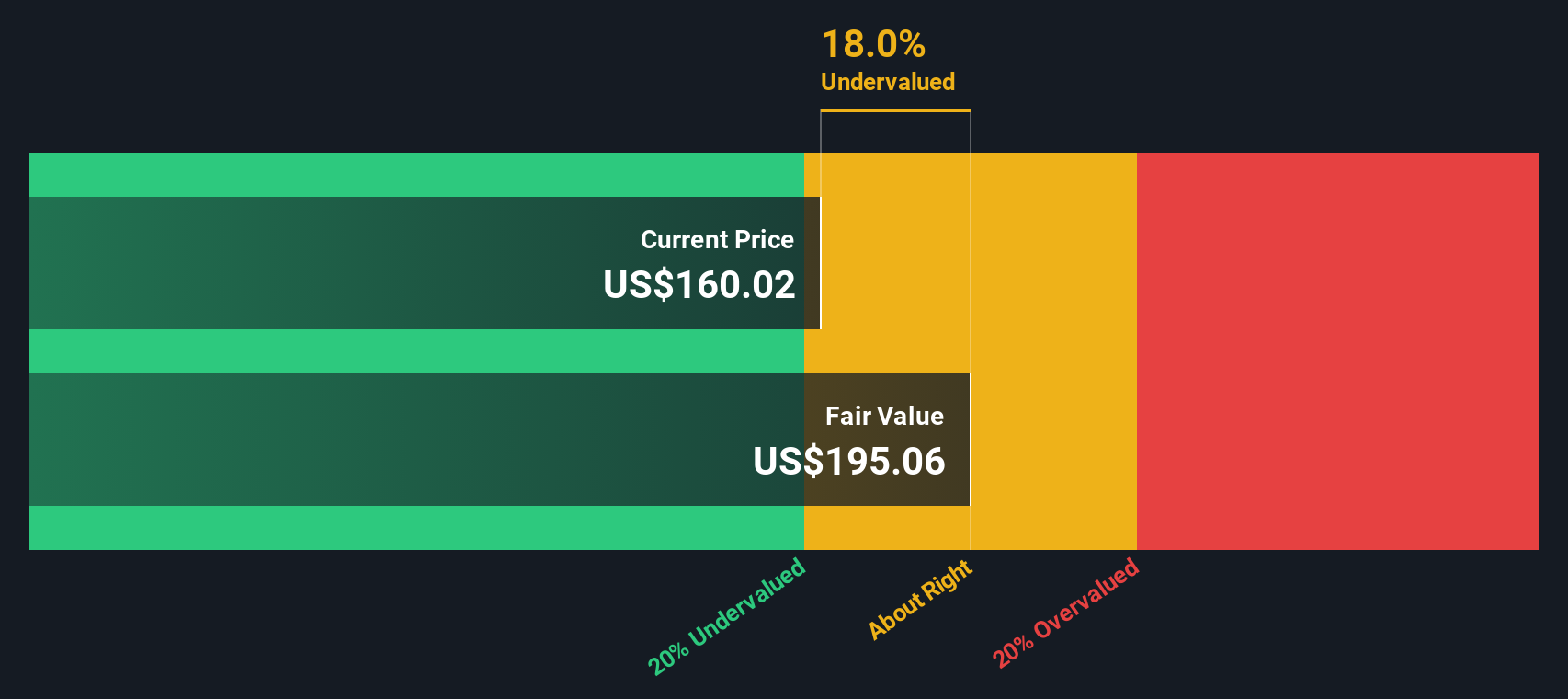

With Datadog trading at US$123.46 and sitting on a 50.47% intrinsic discount by one estimate, yet already reflecting strong growth expectations, are you looking at a genuine mispricing or a stock where future growth is fully priced in?

Price-to-Sales of 13.5x: Is it justified?

Datadog trades on a P/S ratio of 13.5x, which stands out against peers and helps explain why opinions on valuation are so mixed at US$123.46.

The P/S multiple compares the company’s market value to its annual revenue and is often used for software names where earnings can be modest or volatile. For Datadog, this focuses attention on how much revenue growth and margin progress investors expect over time.

On the one hand, Datadog is forecast to grow revenue by 15.9% per year and earnings by 32.5% per year, with earnings expected to grow significantly faster than the wider US market. On the other hand, the current P/S of 13.5x is described as expensive versus both the US Software industry average of 4.5x and a peer average of 8.8x. It also sits above an estimated fair P/S ratio of 12.3x that the market could eventually gravitate toward.

Result: Price-to-Sales of 13.5x (OVERVALUED)

However, recent 30 day and 1 year share price declines, along with the possibility that revenue and net income growth could slow from current levels, could quickly challenge the bullish thesis.

Another View: DCF Suggests the Market May Be Too Harsh

While the 13.5x P/S ratio suggests Datadog is expensive, our DCF model points in a different direction. On that view, the shares at US$123.46 trade about 50.5% below an estimated future cash flow value of US$249.27, which presents a very different risk reward picture.

If the P/S suggests caution and the DCF hints at opportunity, which signal do you pay more attention to when a stock’s growth story is still evolving?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Datadog for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Datadog Narrative

If you look at these numbers and reach a different conclusion, or just prefer to test the inputs yourself, you can build a complete story for Datadog in a few minutes with Do it your way.

A great starting point for your Datadog research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Datadog is on your radar, do not stop there. The same few minutes of effort could surface other opportunities that fit your style even better.

- Target strong cash flow value by checking out these 877 undervalued stocks based on cash flows that may trade below what their fundamentals suggest.

- Ride the AI wave with these 23 AI penny stocks that put artificial intelligence at the center of their business models.

- Tap into potential income streams through these 13 dividend stocks with yields > 3% that offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.