Assessing DLocal (DLO) Valuation After Recent Share Price Strength And Contrasting Earnings Signals

DLocal Limited DLO | 12.86 | +3.38% |

What the latest move in DLocal (NasdaqGS:DLO) means for investors

DLocal (NasdaqGS:DLO) has drawn investor attention after a recent uptick in the share price, with the stock up 2.4% over the past day and 4.8% across the past week.

That short term strength sits alongside a mixed return profile. The stock has gained 4.4% over the past month but declined 5.0% over the past 3 months, which may prompt you to recheck the company’s fundamentals.

With the share price at $14.73, DLocal’s recent upward move comes after a mixed pattern, with short term share price gains alongside a weaker 3 month share price return and a positive 1 year total shareholder return of 24.23% that hints at improving sentiment toward its earnings and cash generation profile.

If DLocal’s recent moves have caught your attention, this could be a good moment to see what else is out there via fast growing stocks with high insider ownership.

With DLocal trading at $14.73, alongside a 24.23% 1 year total return, a value score of 4 and a modelled 23.37% intrinsic discount, the central question is whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 34.5% Undervalued

According to one of the most followed narratives, DLocal’s fair value sits at $22.49 per share, compared with the recent close at $14.73. This sets up a wide valuation gap that hinges on long term cash flow assumptions.

The trading narrative for dLocal (DLO), based on the DCF Valuation HatedMoats article, is that the stock is significantly undervalued. Key Trading Narrative Points:

• Verdict: Undervalued.

• Intrinsic Value (Base Case): $22.49 per share.

• Price at Time of Analysis (Nov 2025): $13.38 per share.

• Margin of Safety: Approximately 40%.

• Market Implication: The current price of $13.38 implies that the market expects dLocal's Free Cash Flow (FCF) to decline perpetually after 10 years, which the author believes is too pessimistic.

Curious how a capital light payments model plus strong return on capital and generous long term cash flow assumptions combine into that $22.49 fair value? According to cracken25, the key drivers are aggressive free cash flow resilience, rich long run margins and a premium future earnings multiple usually reserved for high growth payment platforms. Want to see exactly how those pieces fit together and how sensitive that value is to even small changes in growth or margins? The full narrative lays out every step.

Result: Fair Value of $22.49 (UNDERVALUED)

However, you also need to weigh risks like potential take rate pressure and regulatory or merchant shocks that could quickly challenge even a well-argued valuation case.

Another View: Earnings Multiple Sends a Different Signal

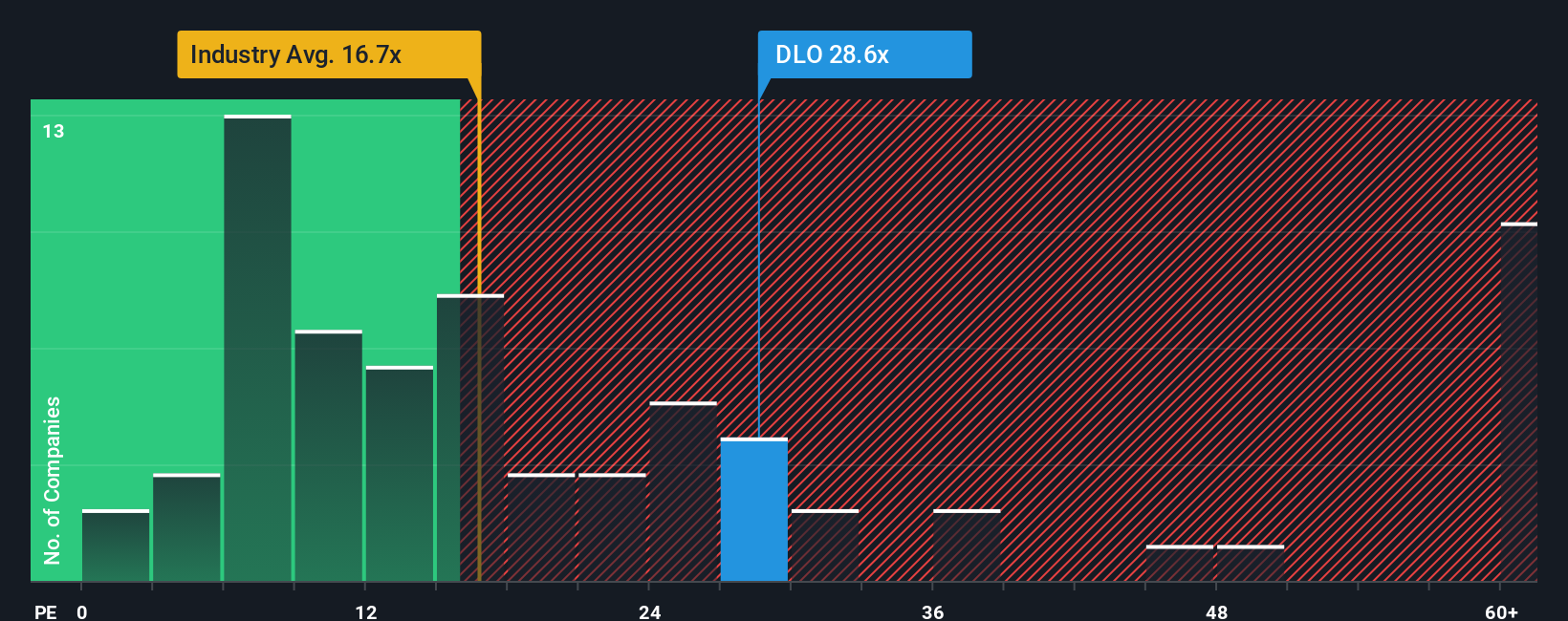

While the narrative and intrinsic value work suggest upside, the current P/E of 25.4x tells a more cautious story. It sits well above the US Diversified Financial industry at 14.6x and above a fair ratio of 21.1x, even though it is lower than the 59.9x peer average. That gap could be a risk if sentiment cools, or a sign the market is still willing to pay up for growth. Which side do you think is getting it right?

Build Your Own DLocal Narrative

If you see the numbers differently or prefer to test your own view against the market, you can build a fresh DLocal story yourself in a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding DLocal.

Looking for more investment ideas?

If DLocal has you thinking harder about pricing and potential, do not stop here. Use the Simply Wall St Screener to line up your next set of ideas.

- Spot companies that the market may be overlooking by scanning these 888 undervalued stocks based on cash flows with strong cash flow profiles and more attractive pricing.

- Tap into the next wave of computing progress by checking out these 23 quantum computing stocks that are pushing forward in this specialist space.

- Build a watchlist of income ideas by filtering for these 13 dividend stocks with yields > 3% that could support a more reliable stream of portfolio cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.