Assessing Doximity (DOCS) Valuation After Earnings Beat AI Tool Adoption And New Buyback Program

Doximity, Inc. Class A DOCS | 22.77 | -0.70% |

Doximity (DOCS) is back in focus after its latest quarter topped internal guidance. Management highlighted growing use of its AI tools by clinicians, and the company paired cautious revenue guidance with a fresh share repurchase authorization.

Despite the better than expected quarter and new AI tools, the share price has been under pressure, with a 30 day share price return of 37.2% and a 1 year total shareholder return of 66.9%, suggesting sentiment has cooled even as buybacks and product rollout shape the longer term story.

If this update on Doximity’s AI push has you thinking about the wider opportunity in healthcare technology, it could be worth checking out our screener of 26 healthcare AI stocks as a starting point for your next idea.

So with Doximity shares down sharply over the past year, ongoing buybacks and AI adoption on one side, and cautious revenue guidance on the other, is the current price a genuine opportunity or is the market already pricing in future growth?

Most Popular Narrative: 56.7% Undervalued

With Doximity last closing at $27.50 against a most followed fair value estimate of about $63.57, the current gap is wide enough that the narrative deserves a closer look, especially given how much of that assessment leans on future product engagement and margins rather than short term sentiment.

The expanded adoption of AI-powered workflow tools (Scribe, Doximity GPT, and Pathway AI) is expected to further entrench Doximity as a core clinician productivity suite, driving frequency of platform use, deeper customer retention, and ultimately higher average revenue per user (ARPU) over time, supporting long-term revenue and margin expansion.

Read the complete narrative. Read the complete narrative.

Curious what kind of revenue climb and margin profile need to hold for that valuation gap to make sense? The most followed narrative leans heavily on sustained growth, strong profitability and a future earnings multiple that assumes Doximity keeps its footing with healthcare professionals and advertisers.

Result: Fair Value of $63.57 (UNDERVALUED)

However, there are clear watchpoints, including Doximity’s dependence on pharmaceutical marketing budgets and the risk that free AI tools take longer than expected to translate into revenue.

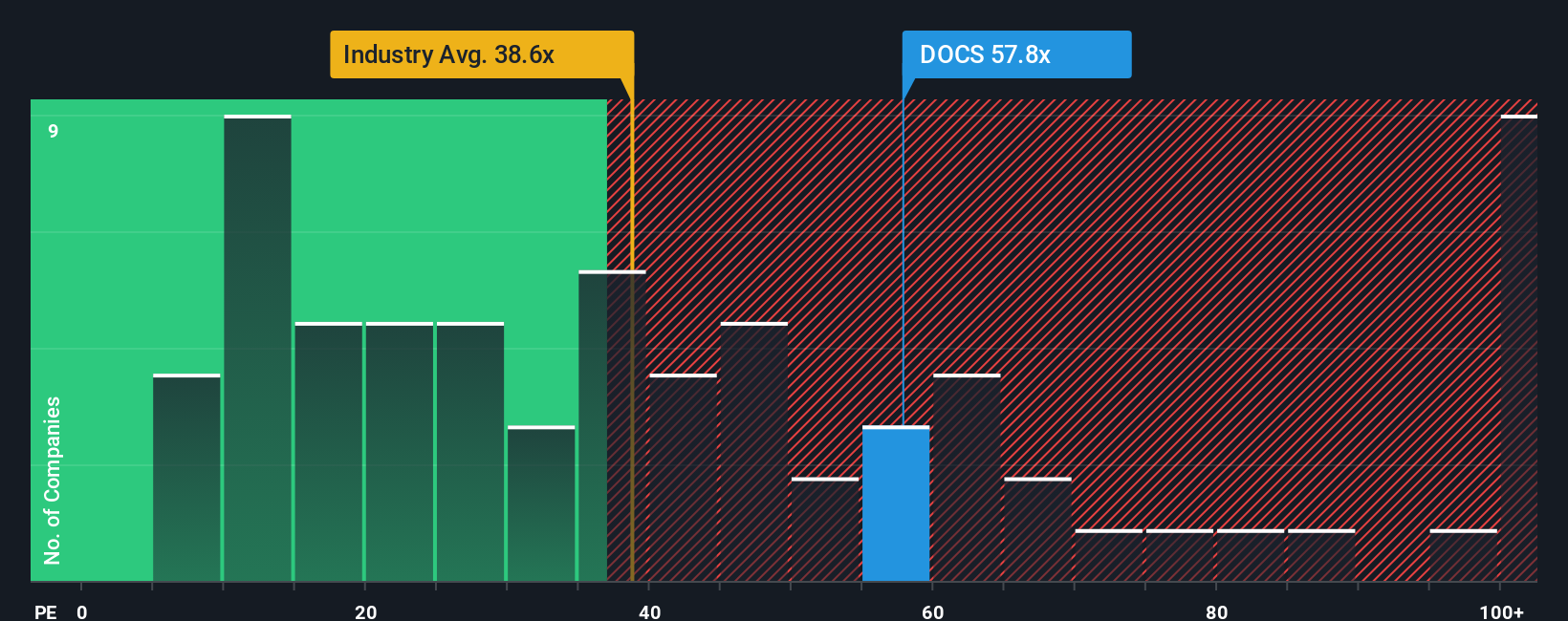

Another View: Market Multiple Sends A Mixed Signal

While the narrative fair value points to Doximity looking undervalued, the current P/E of 21.2x is slightly above its fair ratio of 20.1x, yet sits well below the Global Healthcare Services average of 29.2x and the 51.1x peer average. Is this a margin of safety or a value trap if growth cools?

See what the numbers say about this price in our valuation breakdown, then compare it to other names you follow to decide whether the current multiple really leaves enough room for error. See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Doximity Narrative

If you see the numbers differently or prefer to weigh the data yourself, you can build your own view on Doximity in just a few minutes, starting with Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Doximity.

Looking for more investment ideas?

If Doximity has sparked your interest in what else could be hiding in plain sight, do not stop here. Broaden your watchlist before the next move passes you by.

- Spot potential mispriced opportunities early by scanning our list of 52 high quality undervalued stocks that pair quality fundamentals with what may be discounted valuations.

- Lock in the potential for steady cash returns by reviewing 14 dividend fortresses that focus on higher yielding payouts supported by robust underlying businesses.

- Protect your downside first by checking out our 83 resilient stocks with low risk scores that screen for companies with sturdier financial profiles and lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.