Assessing DraftKings (DKNG) Valuation After Q1 2026 Growth And Predictions Expansion

DraftKings DKNG | 0.00 |

DraftKings (DKNG) just reported Q1 2026 results showing 17% revenue growth and 64% adjusted EBITDA growth, with management spotlighting the Predictions product along with heavy planned investment in that segment.

The stock’s 1 month share price return of 6.53% contrasts with a year to date share price decline of 29.59%, while the 1 year total shareholder return is down 27.93%. This suggests that short term momentum is firming after a weaker stretch, despite upbeat updates on Predictions, upcoming sports events and recent finance team changes.

If Q1 results and DraftKings’ focus on predictions have you looking across the sector, it could be a good moment to scan 61 profitable AI stocks that aren't just burning cash

With Q1 momentum, a Predictions push, and the stock trading about 30% lower year to date, the key question now is simple: Is DraftKings undervalued, or is the market already pricing in its next leg of growth?

Most Popular Narrative: 28% Undervalued

The most followed narrative pegs DraftKings' fair value at about $34.71 per share versus a last close of $25.11. This puts a spotlight on how growth, margins and the Predictions push are being modeled over the long term.

Ongoing product innovation in live betting, in-game personalization, and AI-driven trading is increasing user engagement and dynamic pricing opportunities, which should boost average revenue per user (ARPU) and improve long-term earnings potential.

Read the complete narrative. Read the complete narrative.

Want to see what sits behind that fair value gap? The narrative leans on sustained revenue expansion, a sharp step up in profitability, and a higher future earnings multiple. The mix of Predictions, iGaming and sportsbook is modeled in surprising detail.

Result: Fair Value of $34.71 (UNDERVALUED)

However, this hinges on regulatory and tax outcomes, as higher state levies and tighter rules around prediction markets are both capable of compressing margins and challenging that undervalued view.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Multiples Paint a Tougher Picture

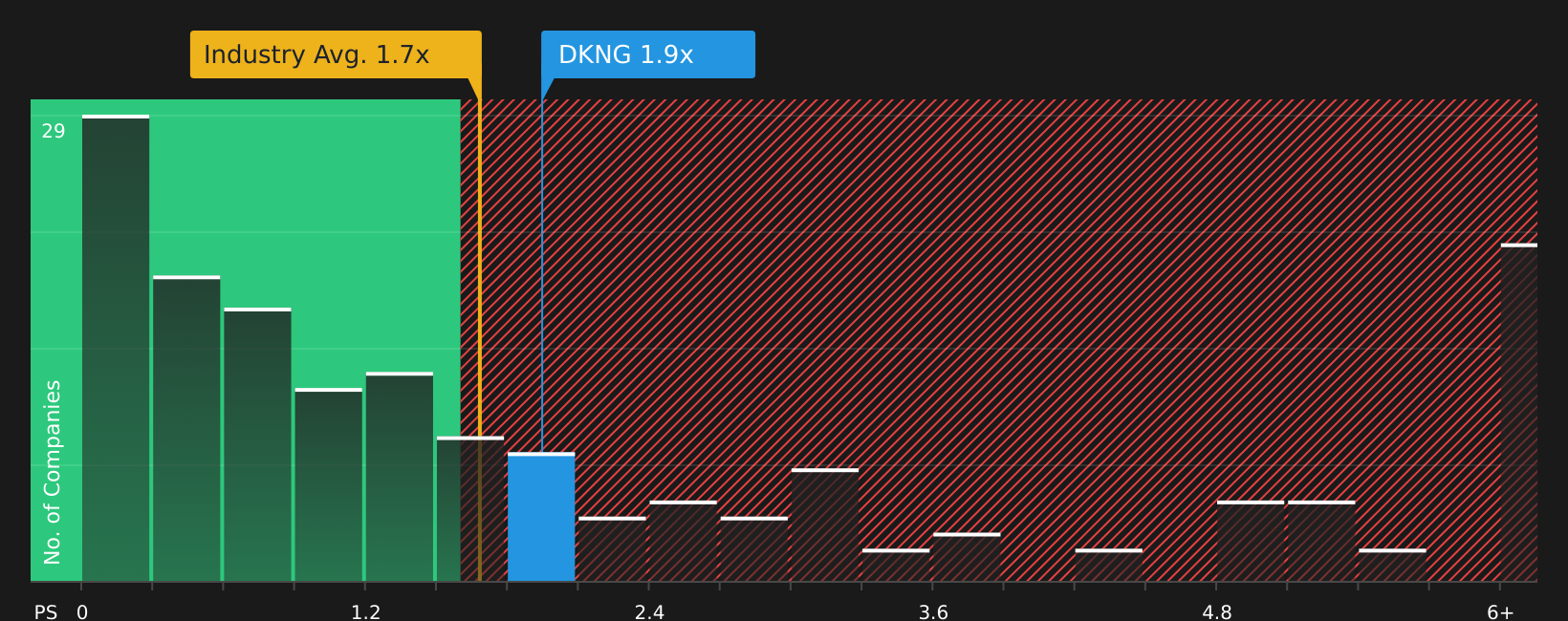

While the popular narrative points to DraftKings trading below a modeled fair value of $34.71, the simple P/S snapshot tells a harsher story. At about 2x sales, the stock is priced above both peers at 1.3x and the broader US Hospitality sector at 1.8x, even though the estimated fair ratio sits higher at 3.6x.

In plain terms, the current P/S suggests investors are already paying a premium compared with similar companies. At the same time, the fair ratio implies the market could still rerate the stock higher over time. The key question is which signal matters more for you right now: the discount to fair value or the premium to today’s peer group?

Next Steps

With mixed signals around value and expectations, the most useful step now is to review the numbers yourself and move quickly to frame your own stance using 3 key rewards and 3 important warning signs

Looking for more investment ideas?

If DraftKings has sharpened your focus, do not stop here. Widen your watchlist with a few targeted stock ideas that match your investing style.

- Spot potential turnaround stories by scanning carefully selected small caps through the 24 elite penny stocks with strong financials.

- Target quality at a measured price by reviewing companies highlighted in the 47 high quality undervalued stocks.

- Prioritize balance sheet strength and durability by checking stocks surfaced by the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.