Assessing DXC Technology (DXC) Valuation As Shares Trade On A 7x P/E And Large DCF-Implied Discount

DXC Technology DXC | 12.66 | +0.96% |

DXC Technology stock: context and recent performance

DXC Technology (DXC) has been drawing attention after recent share price moves, prompting investors to reassess the stock’s recent returns, valuation metrics, and the company’s core IT services business.

Over the past month, DXC Technology’s share price return was about a 2% decline, while the past 3 months show roughly 12% growth, with the latest close at US$14.98. That sits alongside a 1 year total return of about a 28% decline and a 3 year total return of around a 46% decline.

Recent trading reflects that momentum has cooled somewhat, with a 1 day share price return of 3.03% compared with a 90 day share price return of 12.04% and a 1 year total shareholder return decline of 27.63%.

If the recent swings in DXC have you reassessing your watchlist, this could be a good moment to broaden your search and check out high growth tech and AI stocks.

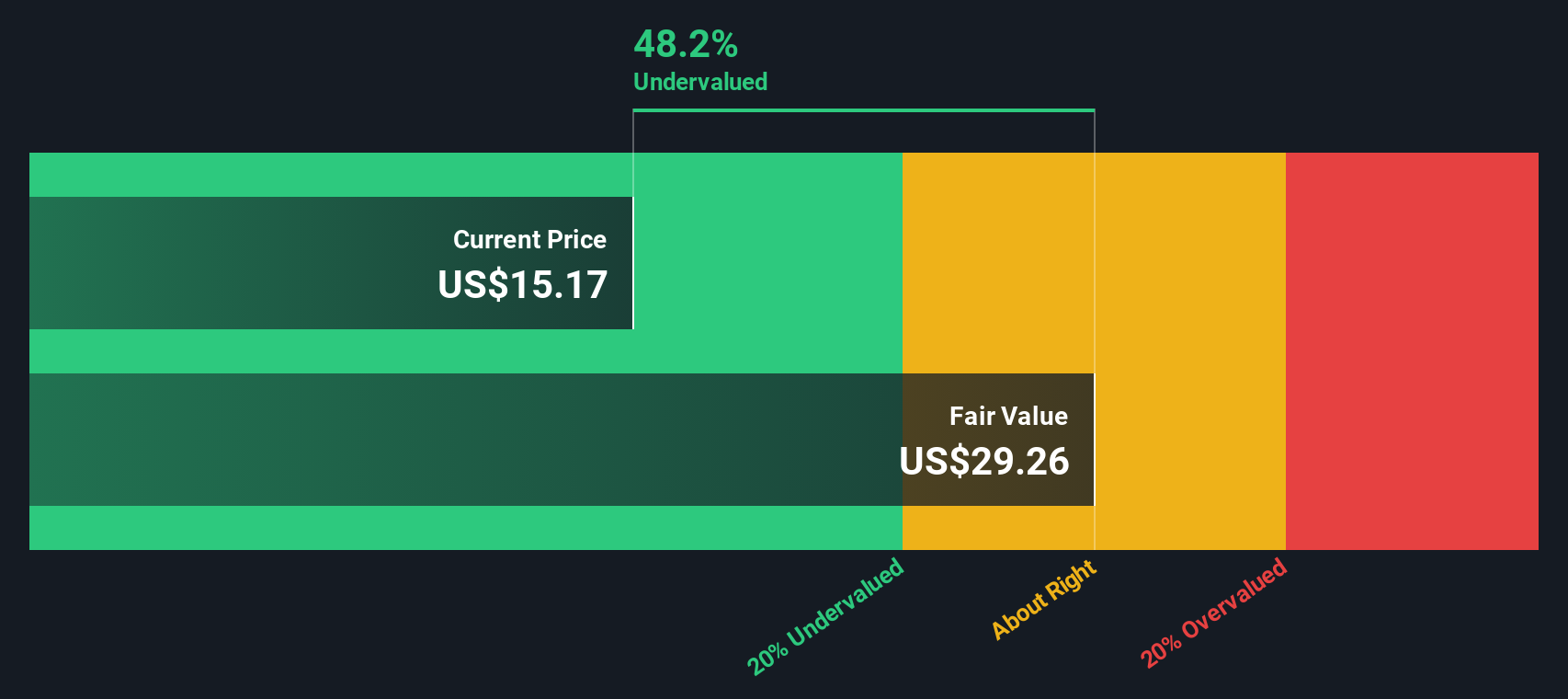

With DXC trading at US$14.98, a value score of 5 and an estimated intrinsic discount of about 49%, the key question is whether this signals a genuine opportunity or if the market already reflects its future prospects.

Price-to-Earnings of 7x: Is it justified?

At US$14.98, DXC Technology is on a P/E of 7x, which screens as good value compared with peers and the wider US IT sector.

The P/E multiple compares the share price to earnings per share, so a lower figure often suggests the market is placing a lower price on each dollar of current earnings. For an IT services company like DXC, this can reflect how investors weigh its earnings profile and outlook against other options in the sector.

DXC is described as trading at good value, with its 7x P/E sitting well below both the peer average of 18.9x and the US IT industry average of 27.4x. Against an estimated fair P/E of 18.7x, the current multiple is also well below the level that the fair ratio suggests the market could move toward if sentiment and earnings expectations aligned more closely with that benchmark.

Result: Price-to-Earnings of 7x (UNDERVALUED)

However, the weak annual revenue and net income trends, along with multi year total return declines, could indicate that operational challenges and investor confidence remain key risks.

Another view: what the SWS DCF model suggests

While the 7x P/E points to good relative value, our DCF model arrives at a fair value estimate of US$29.26 per share, compared with the current US$14.98 price. That implies DXC is trading at a very large discount, so the question is whether the cash flow assumptions hold up.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out DXC Technology for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 881 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own DXC Technology Narrative

If you see the numbers differently or simply prefer to dig into the data yourself, you can build a personalised view in just a few minutes with Do it your way.

A great starting point for your DXC Technology research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If DXC has your attention, do not stop here; broaden your watchlist with other focused ideas that could fit different goals and risk levels.

- Target income potential with these 13 dividend stocks with yields > 3% that may appeal if you prioritise regular cash returns alongside fundamental strength.

- Chase growth themes through these 23 AI penny stocks if you want exposure to companies linked to artificial intelligence trends.

- Hunt for value using these 881 undervalued stocks based on cash flows that screen for stocks trading at discounts based on cash flow estimates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.