Assessing Dyne Therapeutics (DYN) Valuation After BLA Filing For Zeleciment Rostudirsen

Dyne DYN | 0.00 |

Dyne Therapeutics (DYN) has filed a Biologics License Application with the FDA for zeleciment rostudirsen, targeting Duchenne muscular dystrophy patients eligible for exon 51 skipping, and is seeking Accelerated Approval supported by clinical efficacy and safety data.

Recent product milestones around z-rostudirsen appear to be reflected in Dyne Therapeutics' short term momentum, with a 4.15% 1 day share price return and 11.28% 7 day share price return contributing to a 61.62% 1 year total shareholder return from a US$19.33 share price starting point. The 43.93% 3 year total shareholder return suggests longer term holders have also seen meaningful gains.

If this kind of biotech news has your attention, it can be useful to scan other healthcare names using a focused screener, such as 40 healthcare AI stocks

With Dyne Therapeutics now valued at around US$3.20b and trading at US$19.33, plus no current revenue and ongoing losses, investors have to ask whether the stock is still undervalued or if the market is already pricing in future growth.

DCF Valuation: Big Gap Between Price and Cash Flow Estimate

The SWS DCF model points to a fair value of about $98.73 for Dyne Therapeutics compared with the recent $19.33 share price, which implies a large valuation gap based on projected cash generation.

The DCF model estimates what a company might be worth by projecting its future cash flows and discounting them back to today using a required return. That approach puts the focus on long term cash potential rather than current earnings, which is particularly relevant for a clinical stage biotech that is still reporting a loss of $451.707m and has no current revenue.

For Dyne Therapeutics, the DCF result effectively reflects expectations around its neuromuscular disease portfolio and the potential for revenue to emerge over time from programs like Duchenne muscular dystrophy and other indications. With analysts also forecasting strong revenue growth but continued losses over the next few years, the model relies heavily on long term cash flow potential rather than near term profitability.

Result: DCF fair value of $98.73 (UNDERVALUED)

However, investors still face key risks, including Dyne Therapeutics’ ongoing losses of $451.707m, and the uncertainty around successfully commercializing its neuromuscular pipeline.

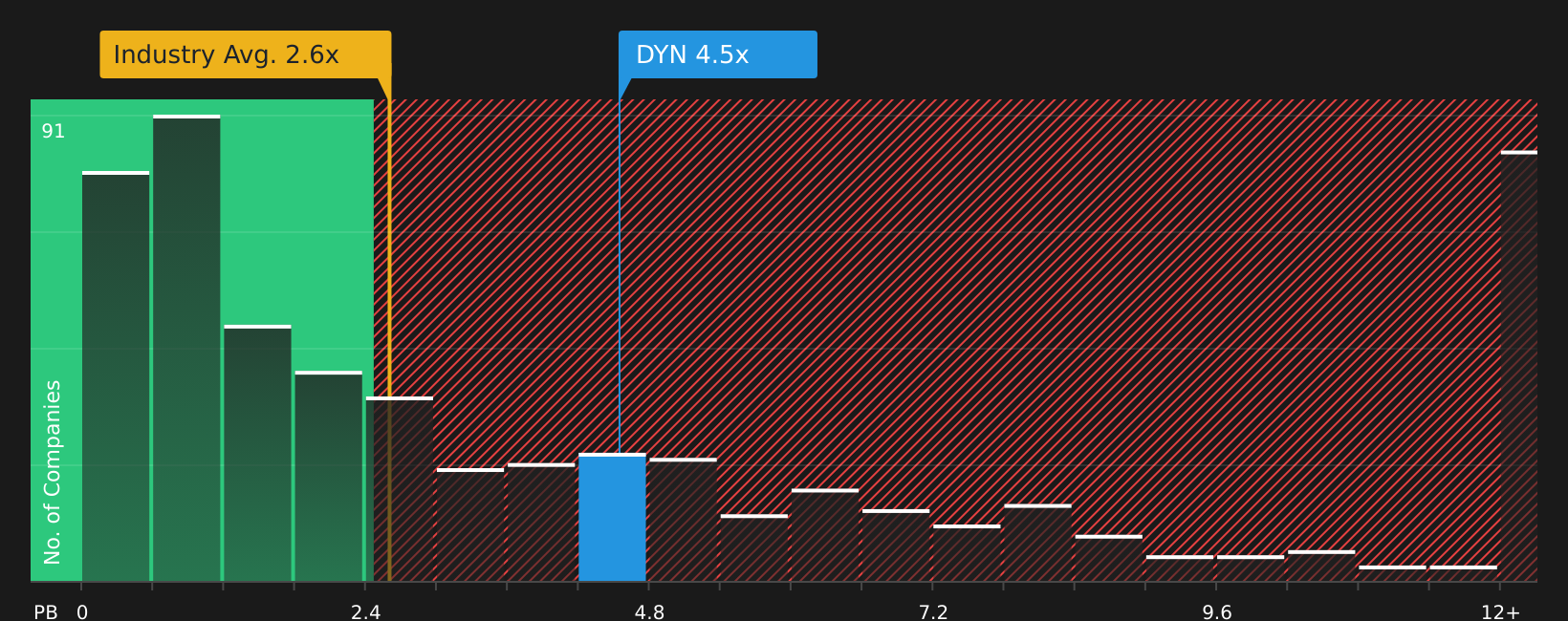

Another View: Book Value Sends A Different Signal

While the SWS DCF model points to Dyne Therapeutics looking undervalued, the $19.33 share price equates to a P/B of 3.7x, which is above the US biotechs industry average of 2.6x. That gap suggests the market is already paying a premium to the sector for Dyne’s balance sheet today.

With one method flagging undervaluation and another pointing to a premium, which signal do you trust more for a loss making biotech that is still pre revenue?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dyne Therapeutics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals from valuation and sentiment, this is the moment to look under the hood yourself and move quickly to shape your own view using the 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If you stop with a single stock, you risk missing other opportunities that might fit your goals even better, so give yourself more quality choices.

- Spot potential bargains by scanning 46 high quality undervalued stocks where solid fundamentals meet prices that may not fully reflect them yet.

- Prioritize resilience by checking 64 resilient stocks with low risk scores to see stocks that score well on financial strength and risk factors.

- Explore additional possibilities by using screener containing 22 high quality undiscovered gems to find quality companies that are not widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.