Assessing Dyne Therapeutics (DYN) Valuation After Recent Pullback And Contrasting P/B And DCF Signals

Dyne Therapeutics Inc DYN | 0.00 |

Event context and recent price performance

Dyne Therapeutics (DYN) has drawn investor attention after a recent pullback, with the stock closing at $17.29 and showing mixed performance over the past week, month and past 3 months.

That recent pullback sits against a mixed backdrop, with the share price down 15.3% over the past month but still showing an 11.3% 3 month share price return and a 46.2% 1 year total shareholder return. This suggests longer term momentum remains stronger than the latest move implies.

If Dyne’s swings have you thinking about diversification, this could be a moment to broaden your watchlist with other healthcare focused opportunities such as 32 healthcare AI stocks

With Dyne still in clinical stages, posting a net loss of $451.707 million and trading at $17.29 against a much higher analyst target, investors may question whether this represents a genuine entry point or whether potential future growth is already reflected in the current price.

Preferred Price to Book of 3.3x: Is it justified?

On simple book value terms, Dyne Therapeutics trades on a P/B of 3.3x, which sits above the wider US biotechs industry but below closer peers.

The P/B ratio compares the company’s market value to its net assets on the balance sheet, which can be a common yardstick for loss making biotechs that do not yet have meaningful revenue. For Dyne, this means investors are currently paying more than the industry average of 2.4x book value, while still paying less than the peer group average of 4.7x.

That gap cuts both ways. The premium to the broader industry suggests the market is assigning a richer valuation than many biotechs. In contrast, the discount to nearer peers points to some restraint in expectations and leaves room for the P/B multiple to move closer to whichever benchmark ultimately proves more relevant over time.

Result: Preferred multiple of Price-to-Book of 3.3x (ABOUT RIGHT)

However, investors still face meaningful risks, including Dyne’s US$451.707 million net loss and the possibility that clinical or regulatory setbacks could quickly change sentiment.

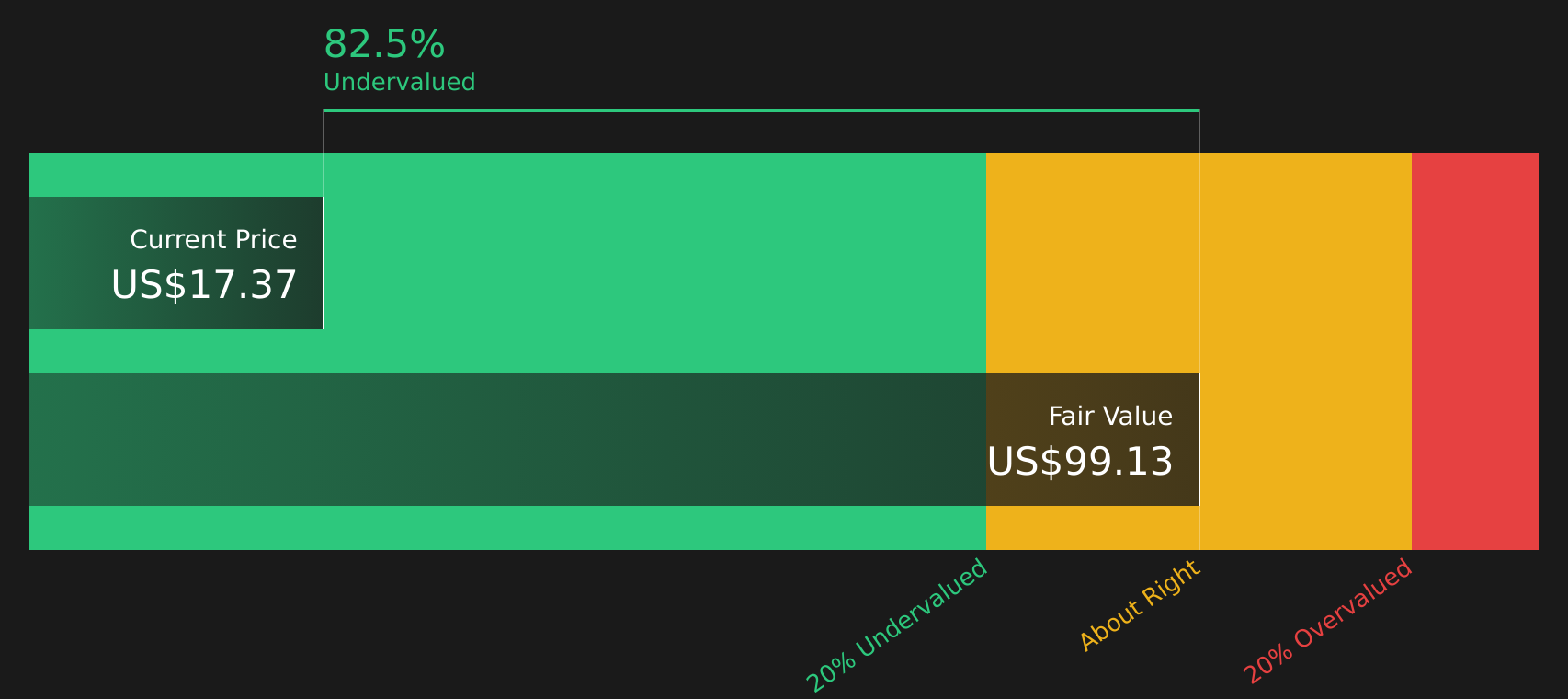

Another way to look at value

Book value tells one story, but the SWS DCF model tells another. On that view, Dyne’s share price of $17.29 sits well below an estimated future cash flow value of $105.60, which points to a very different conclusion on value. Which lens do you trust more in a pre-revenue biotech?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dyne Therapeutics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between risks and potential rewards, it makes sense to move quickly and test the numbers and disclosures yourself before views harden. To weigh both sides in one place and sharpen your own conclusion, start by reviewing the 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If Dyne has sharpened your interest in healthcare and growth stories, do not stop here. Broaden your watchlist now or risk missing the next opportunity.

- Prioritize stability by scanning companies that combine resilient financials with conservative risk profiles through the 65 resilient stocks with low risk scores.

- Hunt for potential value opportunities where quality meets attractive pricing by checking the 51 high quality undervalued stocks.

- Spot companies offering substantial income potential by reviewing the 13 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.