Assessing EastGroup Properties (EGP) Valuation After Recent Share Price Strength And Premium P/E Multiple

EastGroup Properties, Inc. EGP | 188.41 | +0.56% |

What EastGroup Properties stock’s recent performance suggests for investors

With no single headline event setting the tone, EastGroup Properties (EGP) has been drawing attention for its recent share performance and fundamentals, prompting investors to reassess how this industrial REIT fits into their portfolios.

At a share price of $184.06, EastGroup Properties has posted a 9.01% 90 day share price return and a 22.37% 1 year total shareholder return. These recent performance figures may be relevant for investors evaluating momentum and reassessing growth potential and risk around industrial REITs.

If EastGroup’s recent gains have you thinking about where else capital might work hard, it could be a good moment to broaden your search with fast growing stocks with high insider ownership.

With shares around $184 and an implied intrinsic discount of about 15%, investors are left with a key question: Is EastGroup still trading below its underlying potential, or is the market already pricing in future growth?

Most Popular Narrative: 6.2% Undervalued

With EastGroup Properties closing at $184.06 against a narrative fair value of about $196.26, the current price sits below that modeled estimate while still reflecting strong expectations around industrial leasing and earnings.

Structural US population growth and migration to Sunbelt markets continues to underpin robust demand for modern industrial/logistics properties. This directly benefits EastGroup's core portfolio and positions the company for sustained revenue and NOI growth as these regions outpace national averages. Persistent e-commerce expansion and ongoing supply chain modernization are ensuring elevated leasing spreads and high occupancy in EastGroup's infill, last-mile logistics facilities. This supports above-average rental rate growth and drives resilient net margins.

Curious what kind of revenue runway, profit margins, and future P/E multiple are baked into that fair value? The narrative leans on punchy growth assumptions, a richer earnings multiple, and a clear timeline to tie it all together.

Result: Fair Value of $196.26 (UNDERVALUED)

However, that upbeat narrative can be challenged if slower development leasing, concentrated exposure to regions with weaker tenant health, or constrained capital access begin to pressure growth expectations.

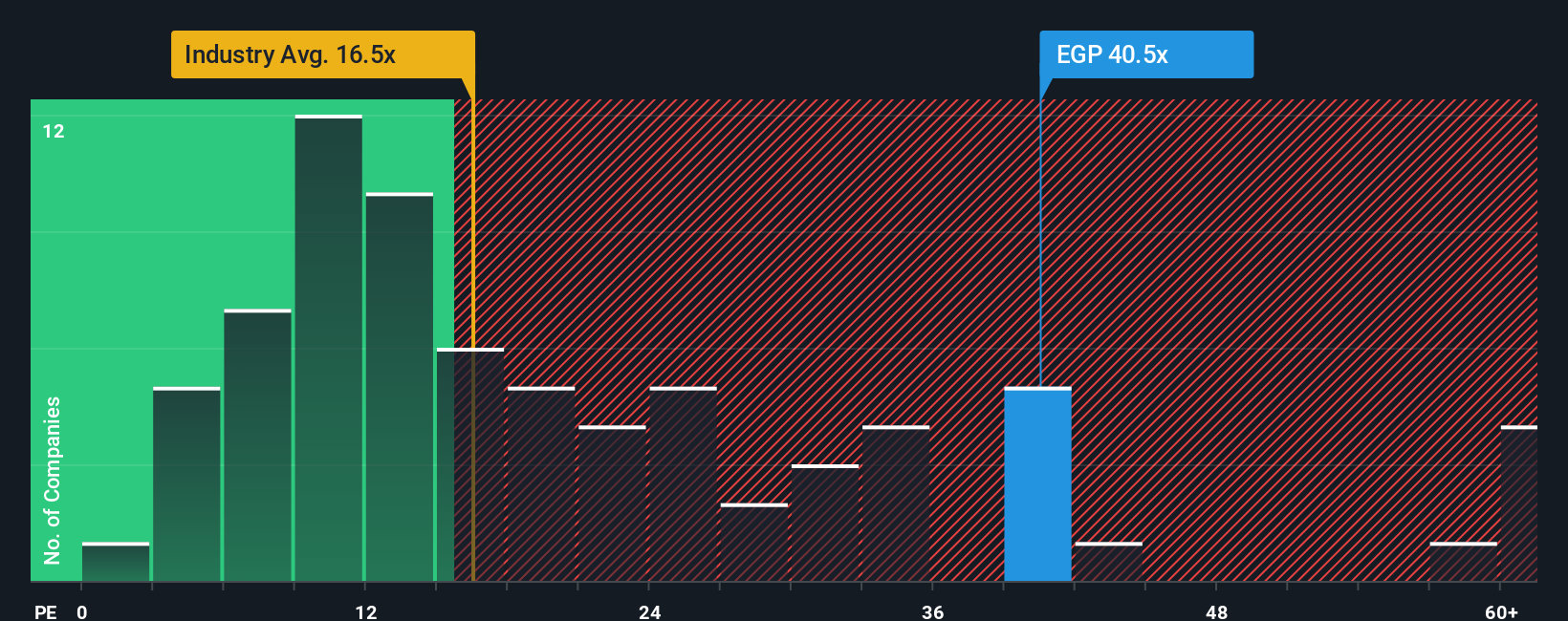

Another Take: What Earnings Multiples Are Saying

Our fair value narrative paints EastGroup Properties as 6.2% undervalued, but its earnings multiple tells a different story. At a P/E of 39.5x, the shares trade well above both the global Industrial REITs average of 17x and peer average of 27.6x. They also sit above the fair ratio of 33.9x that our regression work suggests the market could drift toward over time.

That gap points to valuation risk rather than clear-cut upside, especially if expectations cool or growth comes in softer than hoped. The question for you is simple: do you see this premium as justified staying power, or as room for the multiple to compress instead?

Build Your Own EastGroup Properties Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a custom thesis in just a few minutes with Do it your way.

A great starting point for your EastGroup Properties research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If EastGroup has sharpened your thinking, do not stop here. Your next strong idea could be waiting just a few clicks away in the Simply Wall St Screener.

- Spot potential value opportunities by scanning these 882 undervalued stocks based on cash flows that currently trade below their estimated cash flow based fair value.

- Ride major tech shifts by reviewing these 28 AI penny stocks that are tied to artificial intelligence themes and related growth stories.

- Tap into high income potential by checking out these 12 dividend stocks with yields > 3% that offer yields above 3% with the income profile you are looking for.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.