Assessing Electronic Arts (EA) Valuation As Long‑Term Returns Contrast With A High P/E Multiple

Electronic Arts Inc. EA | 203.60 | +0.01% |

Electronic Arts stock moves and recent performance context

Electronic Arts (EA) has seen mixed share performance recently, with a 1 day return of about a 1.1% decline and a similar 1.5% decline over the past week, providing context for its longer-term performance.

While the recent 1 month share price return of about a 1.5% decline suggests fading short term momentum, the 1 year total shareholder return of 66.9% and 3 year total shareholder return of 79.3% point to a much stronger longer run outcome, supported by annual revenue of US$7.3b and net income of US$885m at a share price of US$201.39.

If EA has you thinking about where the next opportunity might be, this could be a good moment to scan other high growth tech and gaming names through high growth tech and AI stocks.

With EA shares roughly flat over 3 months but up strongly over 1 and 3 years, the key question now is whether this price still leaves room for upside or whether the market is already pricing in future growth.

Most Popular Narrative: 1% Undervalued

At a last close of $201.39 versus a narrative fair value of about $202.36, the current price sits almost on top of that estimate, which is built on detailed growth, margin and discount rate assumptions.

EA's strategic focus on expanding live services and new game launches, such as Skate and Battlefield, is expected to drive revenue growth and foster player engagement. The relaunch of American Football and continued success of FC Mobile, particularly in fast-growing markets, are expected to significantly boost net bookings and player base.

Curious what kind of revenue path, margin profile and future earnings multiple support that fair value so close to today’s price? The narrative leans on a specific growth runway, a higher profitability target and a discount rate that together do the heavy lifting in this $202.36 figure, and the full breakdown shows exactly how each piece fits.

Result: Fair Value of $202.36 (ABOUT RIGHT)

However, there are still pressure points to watch, including weaker net bookings from titles like Apex Legends and sensitivity to consumer spending on gaming in general.

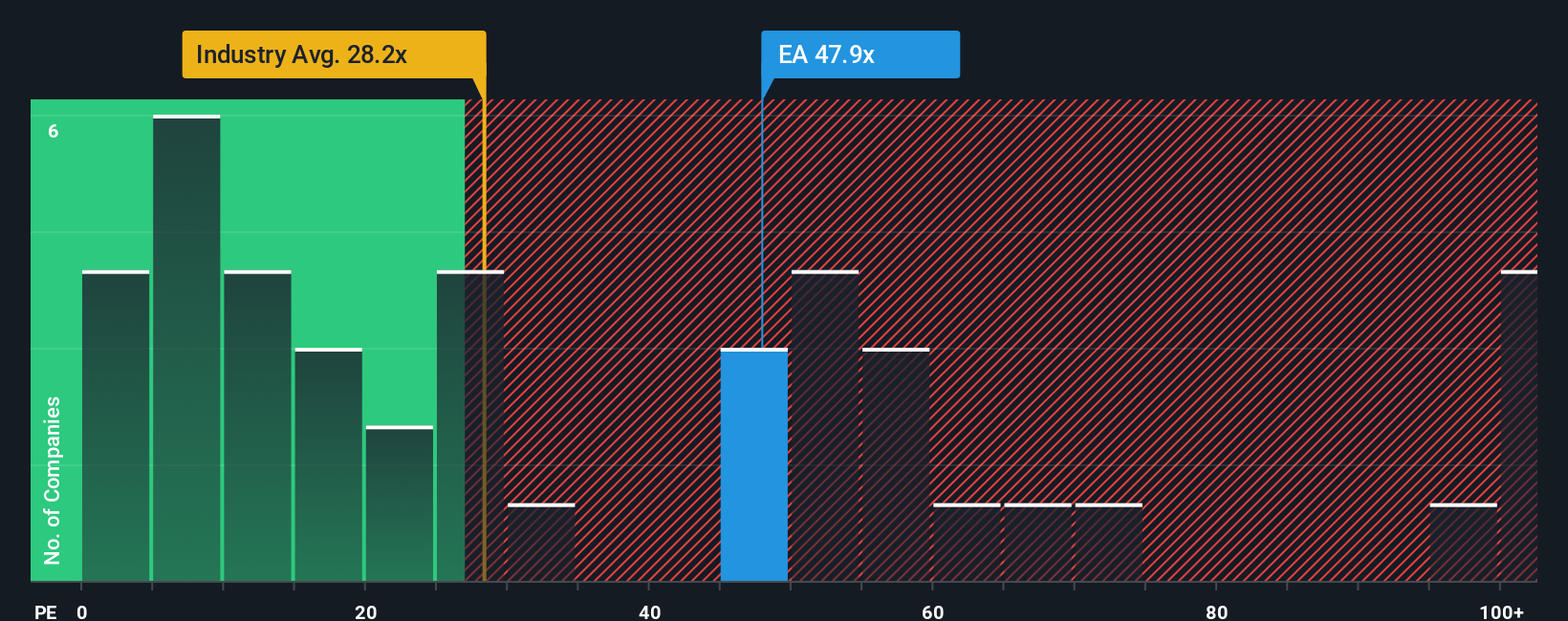

Another angle on valuation: earnings multiples look stretched

While the narrative fair value of about $202.36 suggests EA is roughly fairly priced, the earnings multiple tells a different story. The current P/E of 56.8x is about double the fair ratio of 28.2x and is also above the US Entertainment industry average of 28.5x. This points to meaningful valuation risk if sentiment cools.

Build Your Own Electronic Arts Narrative

If you see the data differently or want to stress test your own assumptions, you can build a custom EA story in just a few minutes with Do it your way.

A great starting point for your Electronic Arts research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If EA has sharpened your interest, do not stop here. The screener can help you spot other opportunities that fit the kind of portfolio you want.

- Target potential mispricing by checking out these 867 undervalued stocks based on cash flows that screen for companies trading below what their cash flows suggest.

- Explore technology-related themes by scanning these 25 AI penny stocks that focus on businesses connected to artificial intelligence.

- Enhance your income stream by reviewing these 13 dividend stocks with yields > 3% that focus on companies offering yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.