Assessing Energy Transfer (ET) Valuation After Recent Share Price Pullback

Energy Transfer ET | 0.00 |

Why Energy Transfer is on investors’ radar today

Energy Transfer (ET) is drawing attention after its recent trading performance, with the stock down 2.3% over the past day and 3.9% over the past week, yet higher over the past month and past three months.

Despite the recent pullback, the stock’s 18.1% year to date share price return and very strong multi year total shareholder returns suggest that momentum has been building rather than fading as investors reassess both growth potential and risk.

If Energy Transfer’s recent move has you looking more broadly at infrastructure and power-related plays, this could be a good moment to check out 35 power grid technology and infrastructure stocks

With Energy Transfer’s solid recent returns, a value score of 4, and the stock trading at a discount to analyst targets and an indicated intrinsic value, you have to ask: is this a buying opportunity, or is future growth already priced in?

Most Popular Narrative: 12% Undervalued

Energy Transfer’s most followed narrative puts fair value at $22.26, above the last close of $19.60. This sets up a clear gap for investors to interrogate.

Aggressive organic growth project backlog (many expected to deliver mid-teen returns from 2026 onward) and a proven history of successful M&A provide strong forward visibility into distributable cash flow and earnings growth, likely supporting valuation re-rating over time.

Want to see what underpins that confidence in future cash flows and earnings power? The narrative leans heavily on projected revenue expansion, steadier margins, and a higher future earnings multiple than many investors might expect.

Result: Fair Value of $22.26 (UNDERVALUED)

However, investors still need to weigh project execution and regulatory setbacks on multi billion dollar pipelines, as well as the longer term risk that energy transition trends weaken asset utilization.

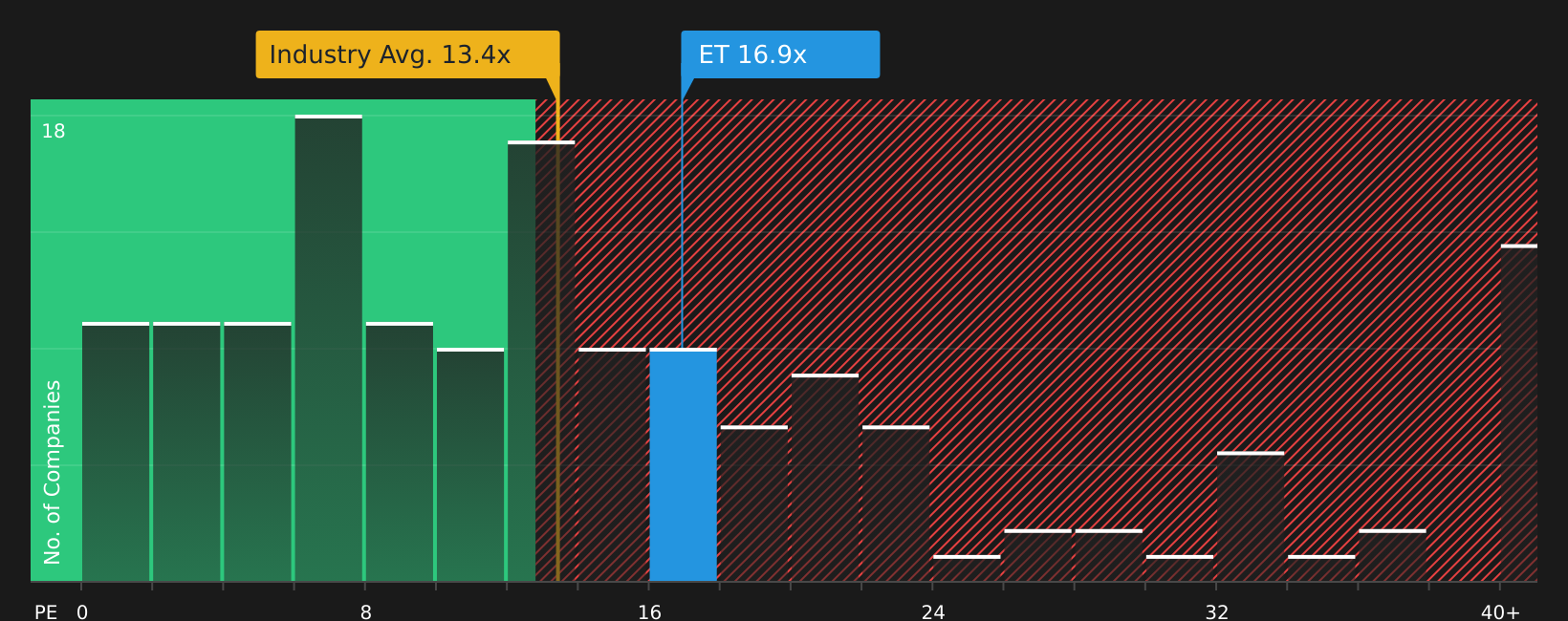

Another way to look at valuation

The narrative leans on a fair value of $22.26, yet the current P/E of 16.4x sits above the US Oil and Gas industry at 14.1x and below a fair ratio of 29.7x. That mix of premium to industry but discount to the fair ratio leaves a simple question: is the market underestimating or overestimating the risks here?

Next Steps

With sentiment looking mixed, this is a good moment to act quickly and review the numbers yourself so you can weigh the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Energy Transfer has sharpened your focus, do not stop here. Use targeted stock ideas to pressure test your thesis and widen your opportunity set.

- Target potential value opportunities by reviewing companies in the 46 high quality undervalued stocks and see how their fundamentals stack up against your current watchlist.

- Prioritize resilience by scanning the 65 resilient stocks with low risk scores so you can focus on companies with steadier risk profiles when markets turn choppy.

- Hunt for future standouts by working through the screener containing 22 high quality undiscovered gems before the broader market starts paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.