Assessing Entergy (ETR) Valuation After A Recent Share Price Pullback

Entergy Corporation ETR | 0.00 |

Recent share performance and business snapshot

Entergy (ETR) has drawn investor attention after a pullback in the stock, with shares down about 10% over the past month and slightly lower over the past 3 months.

Over a longer horizon, Entergy shows a 29.49% total return over the past year and very large total returns over the past 3 and 5 years, alongside annual revenue of US$13.29b and net income of US$1.78b.

At a share price of US$104.97, Entergy’s recent pullback adds to a 1 month share price return that is down 9.84%, yet the 1 year total shareholder return of 29.49% points to stronger longer term momentum.

If this recent volatility has you comparing options in the utilities space, it could be a good moment to look at power grid technology peers using our dedicated screener for 33 power grid technology and infrastructure stocks

With Entergy shares down over the past month but showing strong multi year total returns and revenue of about US$13.29b alongside net income of about US$1.78b, is this pullback a buying opportunity, or is the market already pricing in future growth?

Preferred P/E of 27x: Is it justified?

Entergy currently trades on a P/E of 27x, and at a last close of $104.97 that puts the stock at a richer valuation than many of its peers.

The P/E ratio compares the share price with earnings per share, so a higher P/E often reflects the market paying more for each dollar of current earnings. For a regulated electric utility, that usually signals expectations for relatively steady earnings and potentially moderate growth, rather than rapid expansion.

Analyst forecasts point to earnings growth of about 15.1% per year and revenue growth of about 8.4% per year, which is slower than the broader US market forecasts in both cases. Against that backdrop, a 27x P/E looks demanding compared to the estimated fair P/E of 26.6x, a level the market could move closer to if sentiment cools.

Compared with the US Electric Utilities industry average P/E of 21.3x and a peer average of 17.6x, Entergy stock is priced at a clear premium, suggesting investors are paying up relative to both its sector and closer peers for the current earnings profile.

Result: Price-to-earnings of 27x (OVERVALUED)

However, if earnings or revenue growth undershoots current forecasts, or if the utilities sector’s valuation multiples compress, that premium P/E could come under pressure.

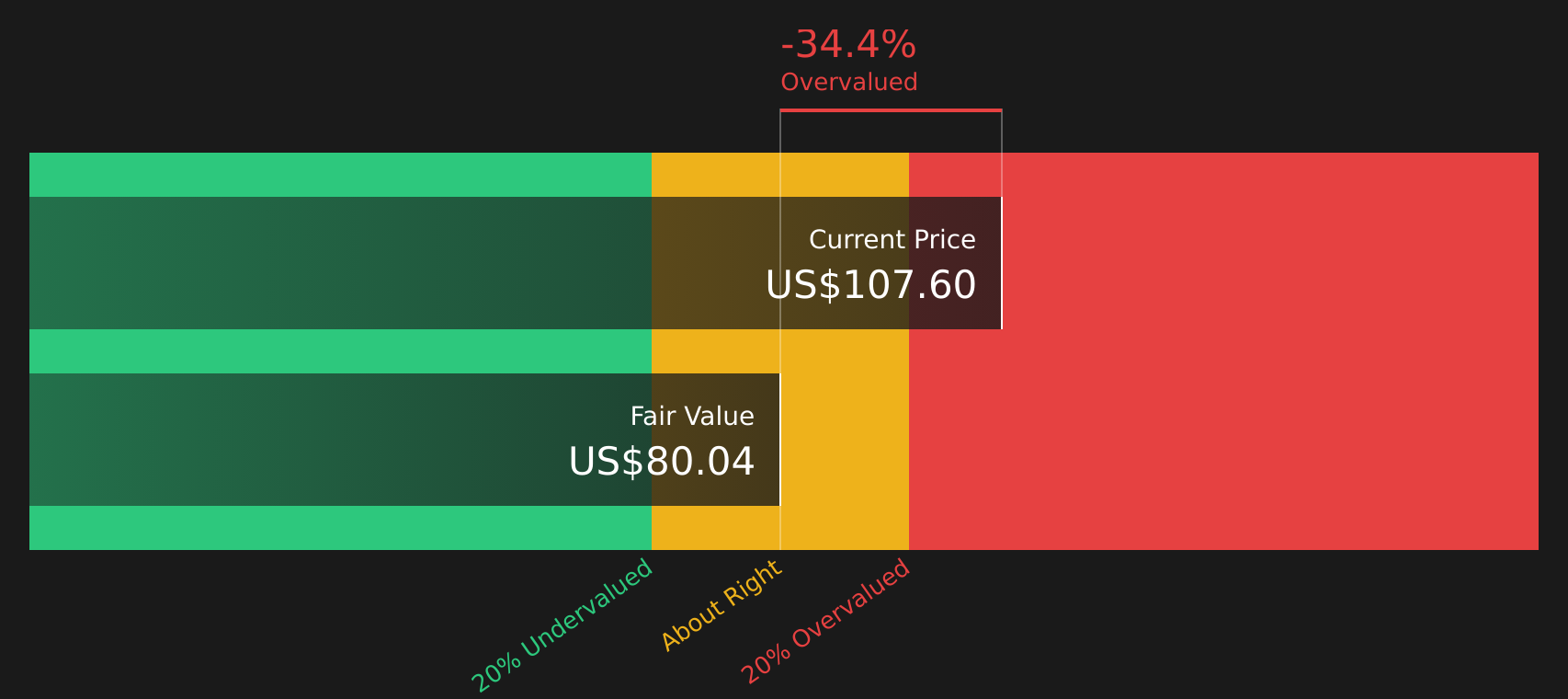

Another view on value: cash flows paint a tougher picture

While the P/E of 27x already looks full, the SWS DCF model is even more cautious, with an estimated future cash flow value of about $80.04 per share versus the current $104.97. That gap implies the stock is trading at a premium to its implied cash flows. Investors may wish to consider how much of that premium they are comfortable paying.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Entergy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment mixed between valuation concerns and long term returns, it makes sense to look at the underlying data yourself and decide how comfortable you are with the current setup. Then weigh both the potential upsides and the issues on your radar by checking out the 2 key rewards and 2 important warning signs

Ready to uncover more opportunities?

If Entergy has caught your eye, do not stop here. The utilities sector is just one corner of the market, and there are plenty of other stocks with different risk, income, and valuation profiles that could fit your goals.

- Target potential mispricing by scanning companies that look attractively valued on key fundamentals through our 47 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies offering higher yields and income focus via the 10 dividend fortresses.

- Prioritise resilience by checking companies with sturdier balance sheets and solid fundamentals using the solid balance sheet and fundamentals stocks screener (45 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.