Assessing F5 (FFIV) Valuation After New Red Hat Kubernetes And AI Security Solutions

F5, Inc. FFIV | 0.00 |

F5 (FFIV) has drawn fresh attention after announcing new products with Red Hat that focus on Kubernetes-native application protection, AI-powered security, and IT modernization, raising questions about what this could mean for the stock.

The recent Red Hat collaboration arrives during a strong upswing, with the share price returning 16.63% over the past month and 41.29% year to date, while three year total shareholder return stands at 150.49%. This suggests momentum has been building for some time.

If the AI and Kubernetes theme behind F5's news has your attention, it may be a good moment to scan a wider field of promising AI infrastructure plays via the 42 AI infrastructure stocks.

With the stock up sharply over multiple time frames and trading slightly above the average analyst price target, the key question is whether F5 still offers upside or if markets are already pricing in much of its future growth.

Most Popular Narrative: 7.5% Overvalued

F5's most followed narrative pegs fair value at $337.40, compared with the last close of $362.58. This puts the current price above that estimate.

The ongoing shift to high-margin, recurring software and SaaS subscription revenue, along with strong renewal and expand activity from existing customers, is improving revenue visibility and predictability while supporting operating margin and EPS growth. Effective operational discipline, evident in robust cash flow, continued cost management, and targeted share repurchases, enhances the company's ability to drive EPS growth, maximize shareholder returns, and weather industry cyclicality.

It is worth considering what combination of revenue trends, margin changes, and future earnings multiple would need to align for that fair value estimate to be supported over time.

Result: Fair Value of $337.40 (OVERVALUED)

However, this depends on software adoption keeping pace and hyperscalers not squeezing out demand for third party platforms, both of which could challenge the current narrative.

Another View: Multiples Point to Limited Stretch

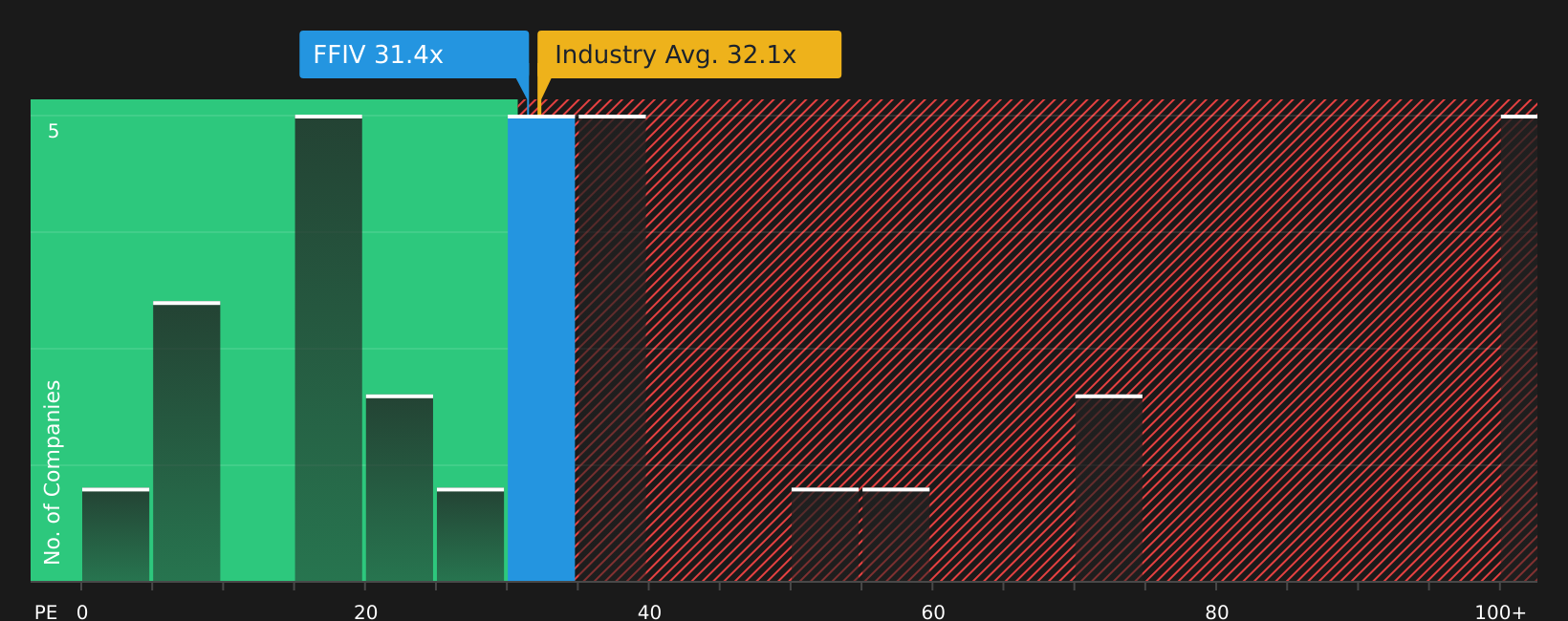

While the most popular narrative suggests F5 is 7.5% overvalued versus a $337.40 fair value, the current P/E of 28.9x looks close to the estimated fair ratio of 29.1x and far below the peer average of 107x. If the stock is in overpaying territory, the gap is not obvious here, so which signal do you trust more?

Next Steps

If the mixed signals in this article leave you unsure, take a closer look at the data and weigh the upside against the concerns. To see both sides set out clearly in one place, review the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If F5 has sharpened your interest in quality technology exposure, consider expanding your watchlist with other focused ideas that could complement your portfolio.

- Target stability by scanning companies screened for resilience and controlled risk using the 66 resilient stocks with low risk scores.

- Hunt for potential value by reviewing the 51 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect them yet.

- Spot potential future leaders early by checking the screener containing 21 high quality undiscovered gems before they attract wider market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.