Assessing Ferguson (FERG) Valuation After Dividend Increase And Moore Supply Acquisition

FERGUSON PLC FERG | 235.07 | -1.67% |

Recent comments from Ferguson Enterprises (FERG) CEO Kevin Murphy put the focus on execution in a tougher market, with a 7% dividend increase and the Moore Supply Company acquisition drawing fresh attention to the stock.

The recent 18.43% 1 month share price return and 16.77% year to date share price return to $262.76 suggest momentum has picked up again. The 50.79% 1 year and 91.88% 3 year total shareholder returns show longer term investors have been well rewarded.

If Ferguson’s move has you thinking about where infrastructure and building trends might head next, it could be a good time to look at 24 power grid technology and infrastructure stocks as another angle on this theme.

With the shares at $262.76 and an intrinsic value estimate that implies about a 4.8% discount, plus a price sitting close to one analyst target, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 0.5% Overvalued

Ferguson’s fair value in the most followed narrative sits at $261.36, just below the recent $262.76 close, so the story hinges on fine margins rather than a big gap.

Ferguson's strategic investments in its HVAC business, including geographic expansion and acquisitions, are expected to drive revenue growth. The focus on dual trade conversions and the private label HVAC line, Durastar, aims to capture market share in a fragmented industry and positively impact future revenue and earnings.

Curious what kind of revenue growth, margin profile, and future P/E level need to line up to justify this valuation call? The full narrative lays out a detailed earnings path, ties it to a specific earnings per share target, and then applies a premium multiple that is above the broader trade distributors group. The tension between that higher multiple and only mid single digit growth expectations is where the real story sits. Read on if you want to see exactly how those moving parts add up to the current fair value.

Result: Fair Value of $261.36 (OVERVALUED)

However, persistent commodity driven deflation and weaker residential demand could pressure margins and test whether Ferguson’s current P/E assumptions still hold up.

Another Angle On Valuation

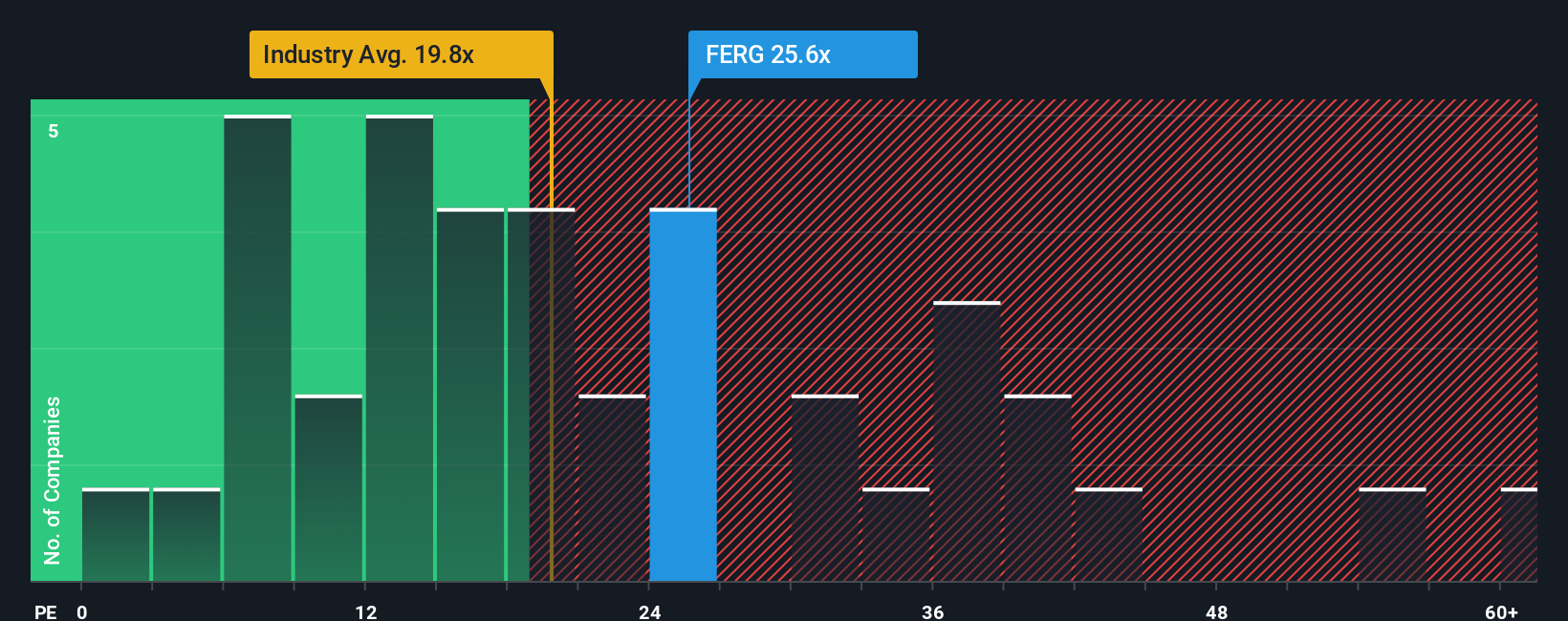

While the most popular narrative sees Ferguson as about 0.5% overvalued at $261.36, the company is also trading at a P/E of 26.3x, slightly below its own fair ratio of 31.1x but above the US Trade Distributors average of 23.7x. Is that a premium you are comfortable paying for this story?

Build Your Own Ferguson Enterprises Narrative

If you are not fully on board with this view, or you prefer to stress test the assumptions yourself, you can build a custom thesis in just a few minutes and push the data in your own direction, then hit Do it your way to put your version on record.

A great starting point for your Ferguson Enterprises research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready To Find Your Next Idea?

If Ferguson has sparked your interest, do not stop here. Broadening your watchlist with a few fresh, high quality ideas could make a real difference over time.

- Target potential value opportunities by scanning our 53 high quality undervalued stocks that pair strong fundamentals with appealing prices.

- Prioritize resilience by checking out 86 resilient stocks with low risk scores that score well on our risk filters and may suit a steadier approach.

- Spot lesser known opportunities by reviewing a screener containing 24 high quality undiscovered gems that most investors are not watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.