Assessing Fermi (FRMI) Valuation After New US$165m Financing And 5 GW Project Matador Permit

Fermi Inc. FRMI | 0.00 |

Fermi (FRMI) has drawn fresh attention after securing a new US$165 million equipment financing and filing a 5 GW Clean Air Permit application in Texas, both tied to its large scale Project Matador campus.

Despite the news around Project Matador and fresh equipment financing, Fermi’s short term momentum has cooled. The 7 day share price return shows a 14.17% decline and the 30 day share price return shows a 47.58% decline, leaving the stock at US$6.18 and continuing a weaker year to date share price return of a 29.93% decline.

If you are looking beyond Fermi and want to see what else is setting up around the grid and power theme, this could be a good moment to scan 26 power grid technology and infrastructure stocks

With Fermi trading at US$6.18 and an analyst price target of US$28.89, plus an indicated intrinsic discount, the key question is whether the recent pullback leaves upside on the table or whether the market already reflects anticipated future growth.

DCF valuation points to a higher fair value

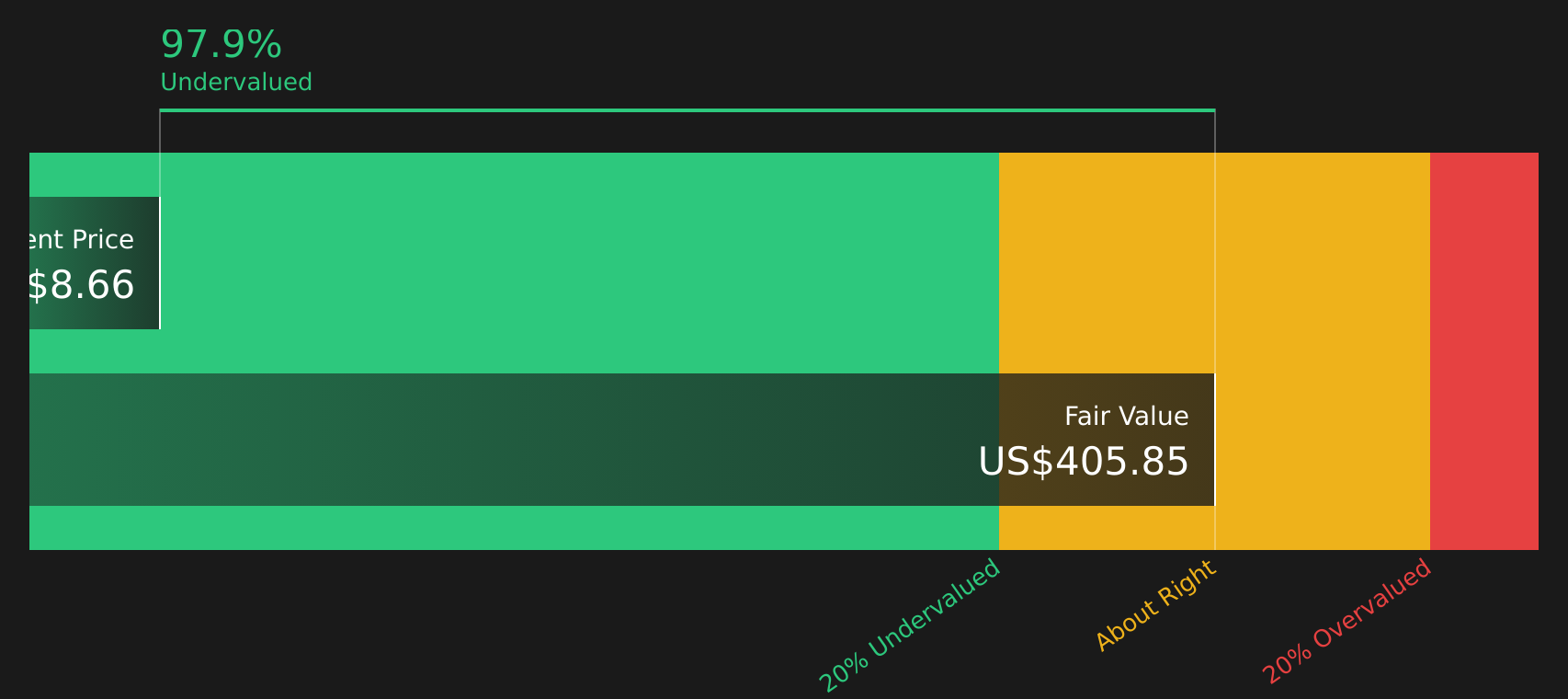

Fermi is trading at $6.18 while the SWS DCF model currently estimates the value of its future cash flows at $12.98, which points to a material gap between price and modeled value.

The DCF approach projects the cash Fermi is expected to generate in the future and then discounts those projections back to today using a required rate of return. The result is a single estimate of what those future cash flows might be worth in present dollar terms.

For a business focused on building private electric grids at gigawatt scale for artificial intelligence workloads, that kind of cash flow based view can be useful because traditional earnings metrics are often less meaningful in the early stages. With limited public history and insufficient data on past growth or margins, the model provides a structured way to compare the current $6.18 price to a $12.98 cash flow estimate without relying on short term share price moves.

Result: DCF fair value of $12.98 (UNDERVALUED)

However, the story could shift quickly if project execution slips or if financing conditions tighten, limiting access to the capital required for this build out.

Analyst targets paint a much steeper path

Analysts see a very large gap between Fermi’s current $6.18 share price and their $28.89 target, implying a multiple of more than 4x. That is a much steeper path than the SWS DCF fair value of $12.98. The question for investors is which lens to lean on when expectations are this wide.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Fermi for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 61 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of potential rewards and clear risks around Fermi can feel finely balanced, so take a moment to weigh the data yourself and decide where you stand, then review the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop at Fermi, you could miss other setups that fit your style, so put the Simply Wall Street Screener to work and compare fresh opportunities.

- Target potential mispricings by scanning 61 high quality undervalued stocks that pair quality fundamentals with compressed expectations.

- Strengthen your income watchlist by reviewing 12 dividend fortresses that focus on higher yields with supporting financials.

- Prioritise resilience by checking 67 resilient stocks with low risk scores that screen for companies with lower risk scores and steadier profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.