Assessing First Solar (FSLR) Valuation After A Strong Multi‑Month Share Price Rally

First Solar, Inc. FSLR | 0.00 |

Why First Solar is on investors' radar

First Solar (FSLR) has drawn fresh attention after a strong run over the past month and past 3 months, prompting investors to reassess what the recent share performance might be pricing in.

That recent surge sits within a broader upswing, with a 30 day share price return of 43.12% and a 1 year total shareholder return of 102.47%. This suggests strong momentum rather than a short term blip.

If you are looking beyond solar and want to see what else is moving in energy related infrastructure, now is a good time to check out 33 power grid technology and infrastructure stocks

With First Solar now trading around $303 a share after a strong run and sitting at a premium to the average analyst price target, the key question is whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 3.2% Undervalued

First Solar's most followed narrative pegs fair value at $313 per share, slightly above the last close at $303. This frames the recent rally as largely in line with modeled upside rather than detached from fundamentals.

The assumed bullish price target for First Solar is $313.0, which represents up to two standard deviations above the consensus price target of $248.0. This valuation is based on what can be assumed as the expectations of First Solar's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

Curious what justifies pricing First Solar close to the high end of analyst targets? The narrative leans on faster growth, fatter margins, and a lower future earnings multiple than many peers. The precise mix of those assumptions is what really matters.

Result: Fair Value of $313 (UNDERVALUED)

However, this bullish setup still leans heavily on supportive U.S. policy and trade protection, as well as on First Solar keeping its technology ahead of fast moving rivals.

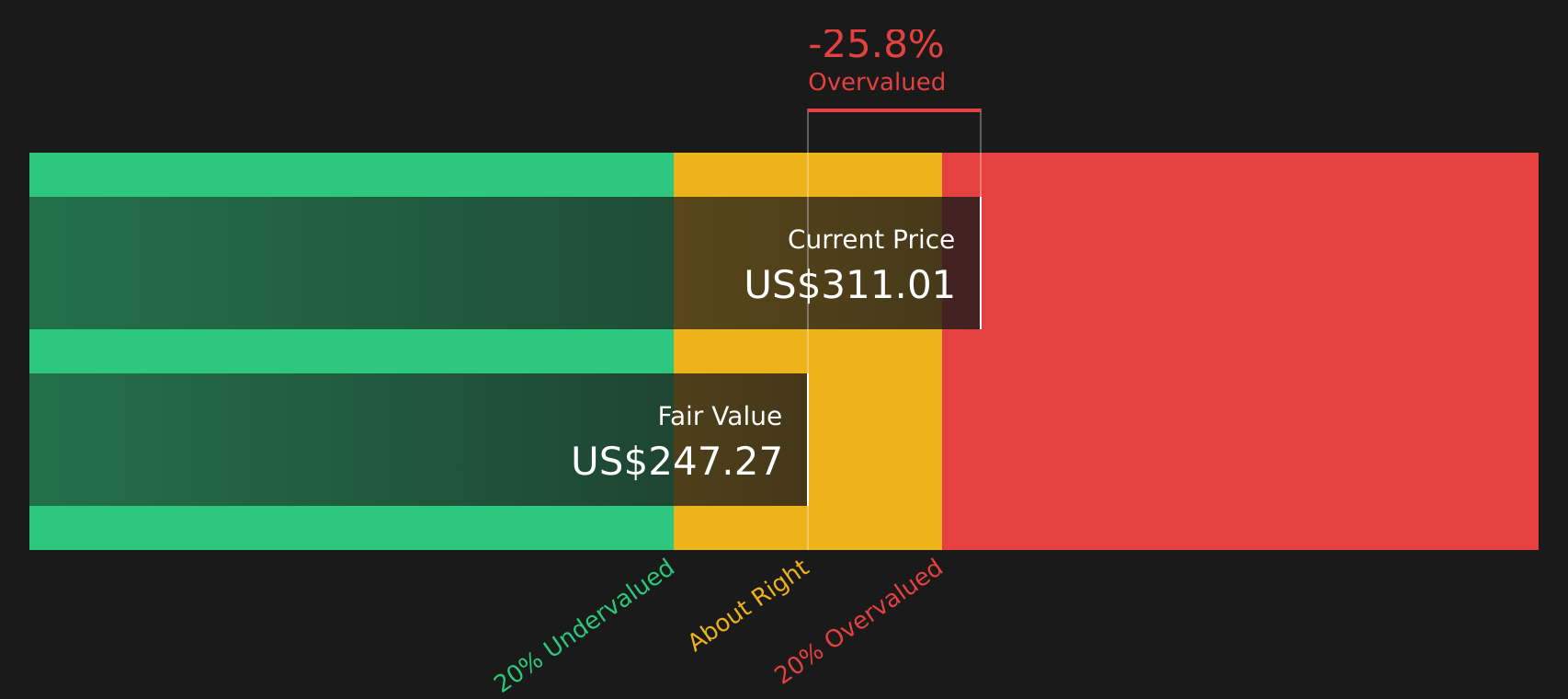

Another lens on value

While the popular narrative sees First Solar as 3.2% undervalued based on bullish assumptions, the SWS DCF model tells a different story. At a fair value estimate of $248.30 versus a $303 share price, the stock screens as overvalued on future cash flows. Which set of assumptions do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out First Solar for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between the recent rally and the valuation debate, this is a moment to move fast and test the assumptions yourself by weighing 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop at just one stock, you risk missing out on other opportunities Simply Wall St's screener can surface across quality, value, and income focused ideas.

- Target quality at a discount by scanning companies that look under-priced on fundamentals through the 47 high quality undervalued stocks.

- Prioritise resilience by filtering for businesses with stronger finances using the solid balance sheet and fundamentals stocks screener (45 results).

- Spot potential early stage opportunities by hunting through the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.