Assessing First Solar (FSLR) Valuation After Recent Pullback And Policy‑Driven Momentum

First Solar, Inc. FSLR | 0.00 |

Recent performance snapshot

First Solar (FSLR) has drawn fresh attention after a sharp pullback last week, with the stock down about 5% over the past day and 16% over the past week.

That short term weakness comes after gains of 19% over the past month and 31% over the past 3 months. The stock last closed at US$262.19, inviting closer scrutiny from investors.

For context, the recent pullback follows a strong run, with the stock showing a 30.9% 90 day share price return while the 1 year total shareholder return sits at 59.3%. This suggests momentum has cooled but longer term holders remain well ahead.

If you are looking beyond solar and energy infrastructure, this could be a good moment to size up other electrification beneficiaries through the 34 power grid technology and infrastructure stocks

After strong recent gains and a pullback from the highs, the key question now is whether First Solar’s valuation leaves any margin of safety, or if the current price already reflects most of its future growth.

Most Popular Narrative: 7.6% Overvalued

The most followed narrative puts First Solar’s fair value at about $243.59, which sits below the latest close at $262.19 and frames the recent pullback in a different light.

Recent U.S. policy changes, specifically strengthened incentives and tighter restrictions against foreign entities of concern (such as China) under the new reconciliation legislation, are boosting First Solar's competitive moat, supporting robust demand for domestically produced modules, and enabling the company to capture higher long-term contracted pricing, directly improving forward revenue visibility and gross margins.

Read the complete narrative. Read the complete narrative.

Want to see what earnings path and margin profile sit behind that fair value cut, even as policy support and backlogs stay central to the story? The most followed model leans heavily on a specific mix of moderate revenue growth, high profitability, and a lower future P/E multiple than many peers. Curious how those ingredients combine into an 11% discount rate and a fair value that still comes in below today’s price?

Result: Fair Value of $243.59 (OVERVALUED)

However, this story can shift quickly if trade policy turns less supportive or if intense pricing pressure from Asian manufacturers squeezes margins harder than analysts expect.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another way of looking at value

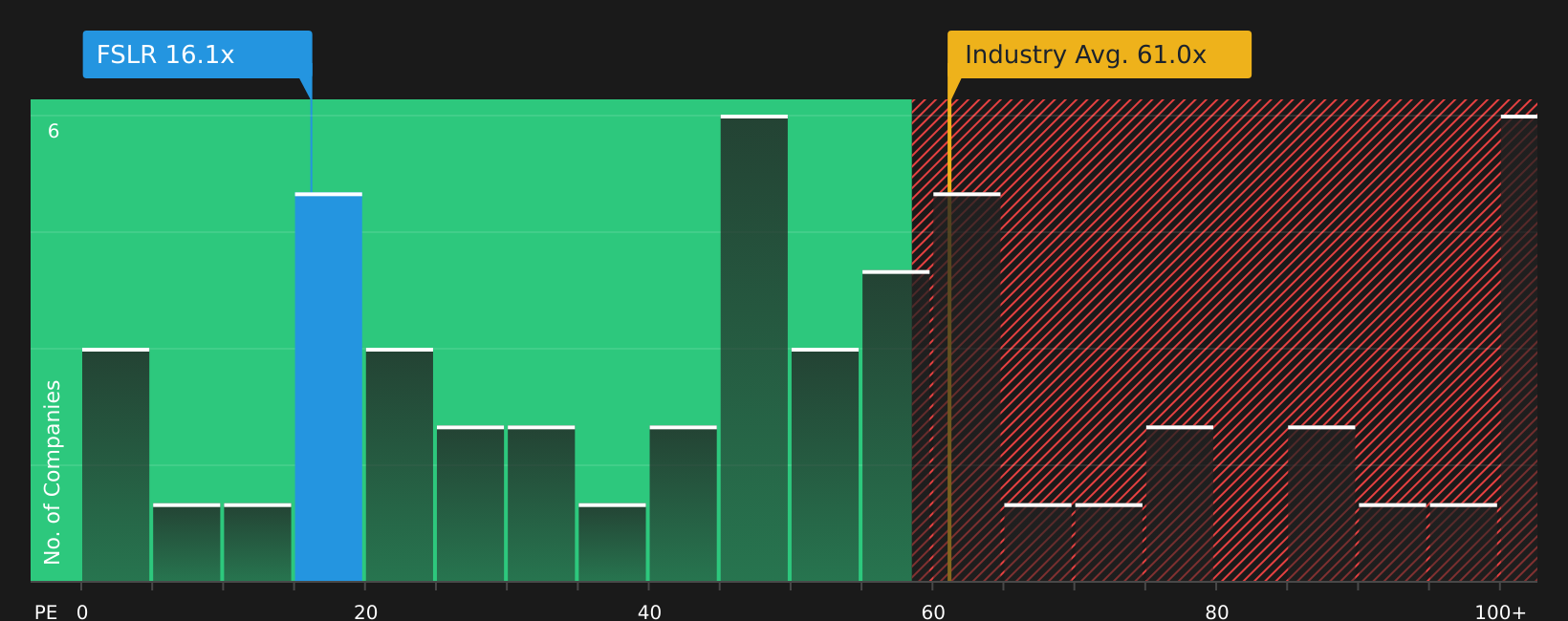

Analysts using price targets see First Solar as about 7.6% above their US$243.59 fair value estimate, with the stock at US$262.19. Yet on a P/E of 16.9x, it trades far below the US Semiconductor industry at 62.7x and a fair ratio of 43x, which points to a very different risk reward picture. Which signal do you treat as more important?

Next Steps

If this mix of optimism and caution around First Solar feels familiar, this is the moment to check the data yourself and firm up your stance. To see exactly what has investors encouraged, take a closer look at the 4 key rewards.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other compelling setups that might fit your goals even better, so widen your search before making your next move.

- Target potential mispricings by scanning for quality companies trading below their implied worth through the 46 high quality undervalued stocks

- Strengthen your focus on resilience by filtering for companies in the 63 resilient stocks with low risk scores that score well on stability and downside protection.

- Spot under-the-radar opportunities by running the screener containing 21 high quality undiscovered gems and seeing which lesser known stocks still show strong underlying fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.