Assessing First Solar (FSLR) Valuation As Recent Volatility Clashes With Conflicting Fair Value Estimates

First Solar, Inc. FSLR | 0.00 |

Recent performance snapshot

First Solar (FSLR) has been on a choppy path, with the stock up about 2.4% over the past day but showing negative returns over the past week, month, and past 3 months.

At a share price of US$190.29, First Solar’s recent 30 day and 90 day share price returns of 9.44% and 29.44% declines contrast with a 49.46% 1 year total shareholder return and 120.88% 5 year total shareholder return. This suggests that long term momentum has been positive even as short term sentiment has cooled.

If this kind of volatility has you thinking about where else to put fresh capital to work, it could be worth scanning for other power grid and energy infrastructure names using the 26 power grid technology and infrastructure stocks

With First Solar trading at US$190.29 alongside double digit annual revenue and net income growth, the real question is whether the current valuation leaves upside on the table or already fully reflects expectations for future growth.

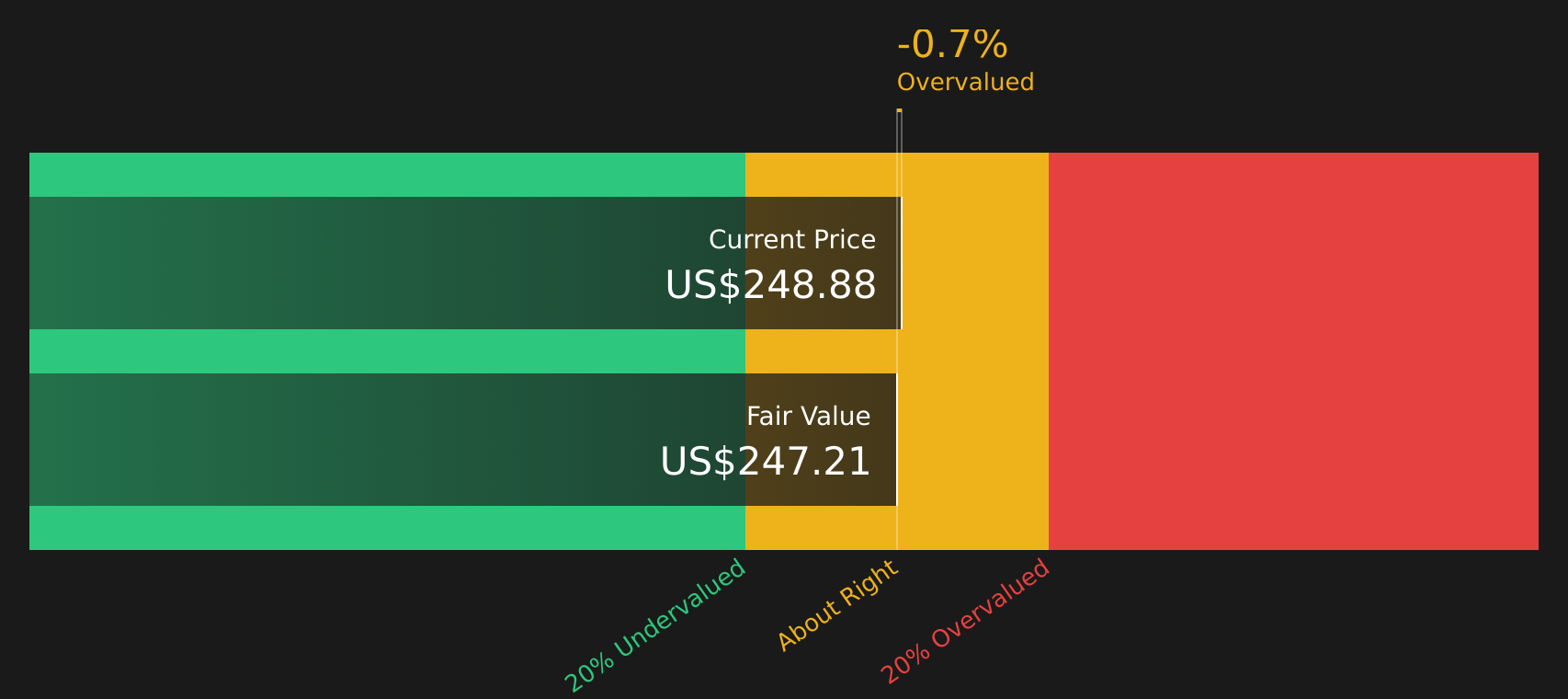

Most Popular Narrative: 22% Overvalued

Compared with First Solar’s last close at $190.29, the most followed valuation narrative pegs fair value closer to $155.98, pointing to a more conservative price view than the market.

Known for its high quality solar panels and government cooperation during the Biden administration, First Solar is a strong company when it comes to maintaining its operations and innovating on solar energy.

Our team believes that First Solar is considerably below its fair value. The current semi bear market present in the US markets caused by President Trump’s tariffs and trade war threats has caused negative sentiments in the market which overall reflected on First Solar’s stock price causing it to drop below its fair price.

This narrative leans heavily on robust margins and a future earnings multiple that points to higher long term profitability. Yet its fair value still sits well below today’s price, which raises questions about how its growth, discount rate and profitability assumptions combine to reach that conclusion.

Result: Fair Value of $155.98 (OVERVALUED)

However, sustained share price declines over the past 3 and 12 months, along with heavy reliance on the US market, could unsettle this view if sentiment or policy support shifts.

Another angle on value

That 22% overvalued narrative sits awkwardly next to the SWS DCF model, which estimates First Solar’s future cash flows at $266.93 per share versus today’s $190.29. On this view the stock screens as undervalued, so which story do you lean on when pricing risk and opportunity?

Next Steps

With mixed signals on value, sentiment and policy risk, this is a moment to move quickly. Review the underlying data and weigh both sides of the story using the 5 key rewards and 1 important warning sign

Looking for more investment ideas?

If you are weighing what to do next after assessing First Solar, it makes sense to line up a few alternatives before the next round of headlines hits.

- Target resilience first by checking companies that pass tight quality filters on balance sheet strength and fundamentals through the solid balance sheet and fundamentals stocks screener (39 results).

- Hunt for potential value by scanning companies that combine quality metrics with lower implied expectations using the 61 high quality undervalued stocks.

- Expand your watchlist with lesser known names that still score well on fundamentals via the screener containing 26 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.