Assessing FLEX LNG (NYSE:FLNG) Valuation As DCF And Narrative Views Strongly Diverge

FLEX LNG LTD (BM) FLNG | 30.57 31.20 | +0.33% +2.06% Pre |

Why FLEX LNG (FLNG) Is Back on Investor Radars

FLEX LNG (FLNG) has caught attention after a stretch of strong share price performance, with returns over the past year and past 3 months prompting investors to reassess its recent fundamentals.

The share price has been firming up recently, with a 1-month share price return of 9.59% and a year to date share price return of 18.61%. The 1-year total shareholder return of 49.28% points to momentum that extends beyond the latest move.

If FLEX LNG has you looking at energy related ideas, you might also want to see what stands out among 85 nuclear energy infrastructure stocks as another way to broaden your watchlist.

With an intrinsic value estimate suggesting a sizable discount, yet the current share price sitting above the analyst target, the big question is whether FLNG is genuinely undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 15.9% Overvalued

At a last close of $29.26 versus a narrative fair value of $25.25, FLEX LNG screens as extended on this widely followed valuation view.

The company's multi-year contract backlog (56 years minimum, up to 85 years with options) and long-term charters secure steady revenue and earnings despite short-term market softness, positioning FLEX LNG to benefit as global LNG trade volumes are projected to rise due to new export capacity coming online, particularly from the US, Qatar, and Africa, boosting future cash flow visibility and net margin stability.

Curious what kind of earnings path and margin profile sit behind that fair value estimate, and how a different future P/E could change the story? The full narrative lays out the revenue runway, profitability shift and valuation multiple that need to line up for FLEX LNG to meet those expectations.

Result: Fair Value of $25.25 (OVERVALUED)

However, a wave of new LNG vessels and higher drydocking or environmental compliance costs could still pressure day rates and margins, and weaken the current fair value story.

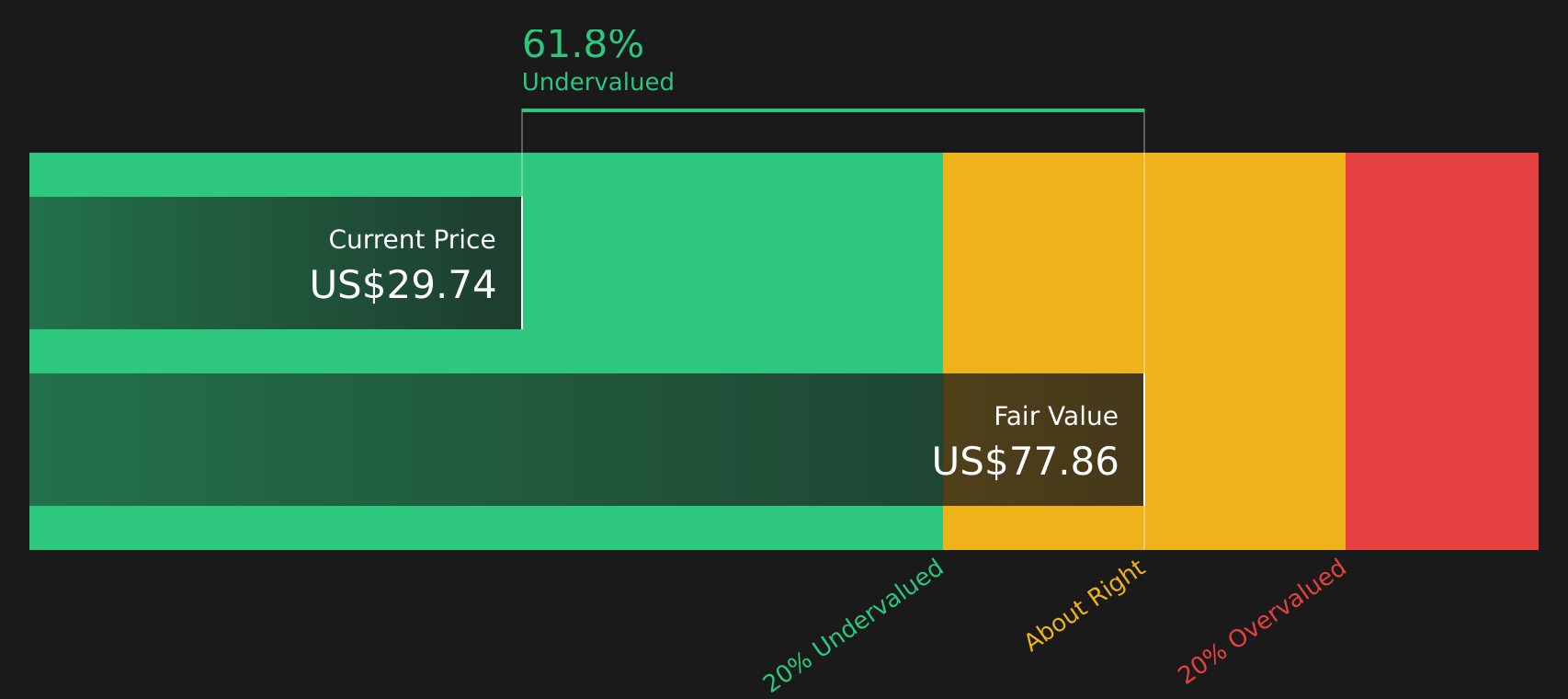

Another Angle: DCF Paints a Very Different Picture

While the narrative fair value of $25.25 suggests FLNG looks 15.9% overvalued at $29.26, our DCF model arrives at a very different result, with an estimate of $91.07. That indicates a substantial gap between price and calculated cash flow value, so which story seems more reliable?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out FLEX LNG for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The split signals in this article show there is more than one way to look at FLEX LNG. Move quickly, test the assumptions yourself, and see how 2 key rewards and 3 important warning signs stack up for your own thesis.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop with a single stock. Use the screener to uncover opportunities that fit your goals before others do.

- Target potential value opportunities by reviewing companies our screener highlights as 49 high quality undervalued stocks based on their fundamentals and pricing.

- Strengthen your income stream by checking out businesses in our list of 15 dividend fortresses that focus on higher yields.

- Dial down portfolio risk by focusing on companies filtered through our 75 resilient stocks with low risk scores that prioritize resilience and financial stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.