Assessing Flywire (FLYW) Valuation After Workday Integration Boosts Attention and Efficiency

Flywire Corp. FLYW | 11.61 | -0.26% |

Flywire (FLYW) has announced a certified integration between its payments platform and Workday Student, a leading information system for higher education institutions. The new partnership aims to simplify billing processes and improve the financial experience for students and administrators alike.

Flywire’s certified Workday partnership has fueled renewed optimism and brought the company into focus, but the market’s response has been mixed. Despite a one-day share price gain of 3.46% and a robust 18.1% advance over the last 90 days, the year-to-date share price return stands at -31.49% and the total shareholder return for the past year is -20.5%. Momentum shows signs of picking up in the short term, even as long-term total returns remain under pressure.

If this latest tech integration piques your interest, now’s a smart moment to expand your outlook and discover fast growing stocks with high insider ownership

With short-term momentum picking up and new partnerships in play, investors face a key question: is Flywire’s current valuation underestimating its growth potential, or is the market already factoring in future gains?Most Popular Narrative: 5% Undervalued

With the narrative’s fair value at $14.55 compared to a last close of $13.77, analysts see modest upside potential. Here is a key development influencing this view.

Ongoing investment in proprietary technology, AI-driven automation, and integration capabilities is yielding significant platform efficiencies (for example, 25% operational cost improvements, 90% automated payment matching, and 40% automated customer service). This supports Flywire's ability to maintain or increase net margins and deliver stronger earnings leverage as scale increases.

Can a digital payments company really deliver profit margins often seen at software titans? The narrative’s price target hinges on ambitious efficiency gains and potential margin expansion. Don’t miss the numbers and assumptions that could mean the difference between just another fintech and an earnings machine.

Result: Fair Value of $14.55 (UNDERVALUED)

However, persistent regulatory challenges and mounting competition could quickly erode Flywire’s margin gains. These factors may also limit the impact of recent international expansion.

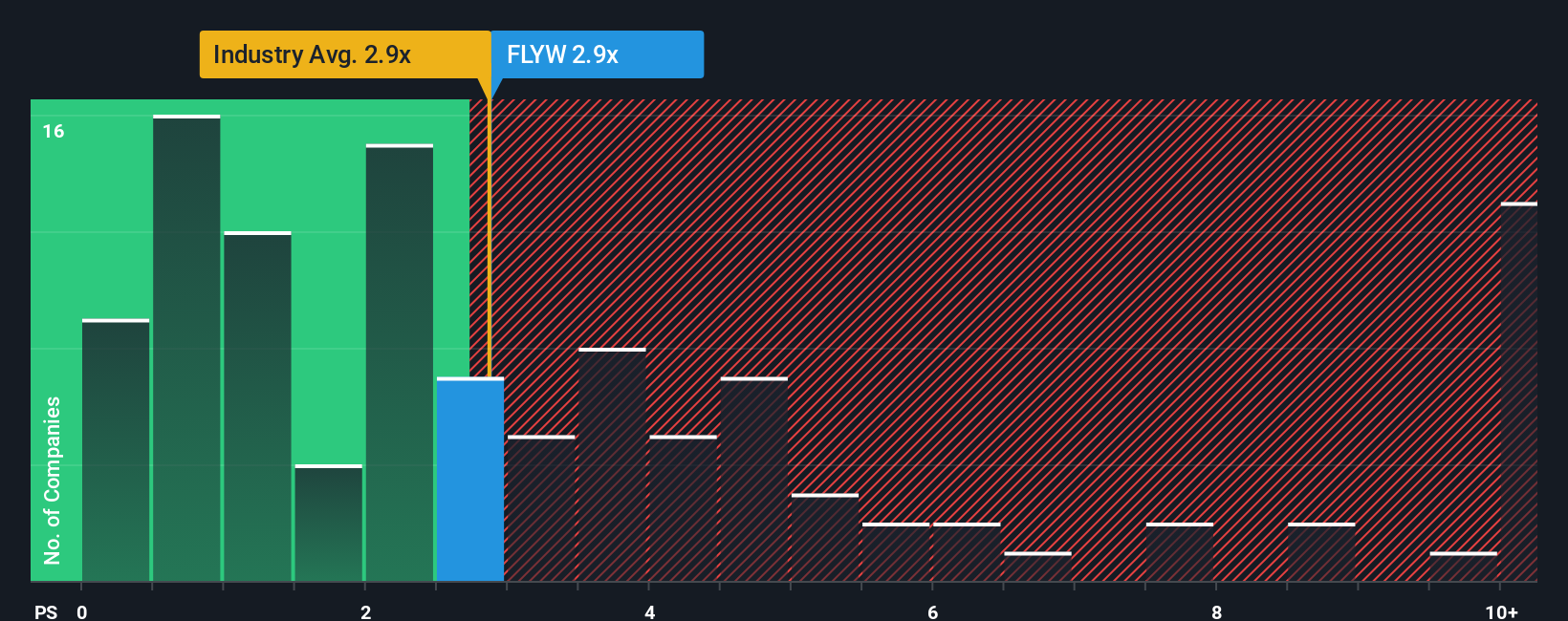

Another View: Market Multiples Suggest a Premium Price

Looking at Flywire through the lens of pricing ratios tells a different story. Its share price is 3.1 times revenue, identical to direct peers but above the US diversified finance industry average of 2.5 times and the fair ratio of 2.5 times. This means the market is already pricing in above-average growth or returns, which raises the risk if expectations are not met. Is this optimism justified or a setup for disappointment?

Build Your Own Flywire Narrative

If you want to dig deeper or have a different take on Flywire, you can assemble your own perspective in just a few minutes: Do it your way

A great starting point for your Flywire research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let opportunity pass you by. The market’s most compelling stories often start before the headlines. Act now to uncover what you could be missing.

- Spot income potential and supercharge your portfolio with regular payers by checking out these 17 dividend stocks with yields > 3% yielding over 3%.

- Capture tomorrow’s tech leaders early by browsing these 27 AI penny stocks making waves in the artificial intelligence space.

- Give your strategy a value edge by seizing these 876 undervalued stocks based on cash flows built on strong cash flow fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.