Assessing FTAI Aviation (FTAI) Valuation After Analyst Upgrades And Strong Earnings Momentum

FTAI Aviation Ltd. FTAI | 255.18 255.18 | -1.71% 0.00% Pre |

Recent analyst enthusiasm has pushed FTAI Aviation (FTAI) into the spotlight, with reports linking higher earnings estimates and long term prospects to the company’s revenue and earnings results.

At a share price of $240.49, FTAI Aviation has pulled back with a 14.06% 30 day share price return and 7.47% 7 day share price return, yet longer term momentum remains strong with a 1 year total shareholder return of 122.51% and a 3 year total shareholder return of more than 9x.

If FTAI’s recent run has you looking for the next opportunity, this is a good moment to scan other aviation related names through our 20 top founder-led companies

With FTAI Aviation trading at $240.49 and sitting at a reported 41% discount to some intrinsic estimates and about 40% below certain analyst price targets, you have to ask: Is there still a buying opportunity here, or is the market already pricing in future growth?

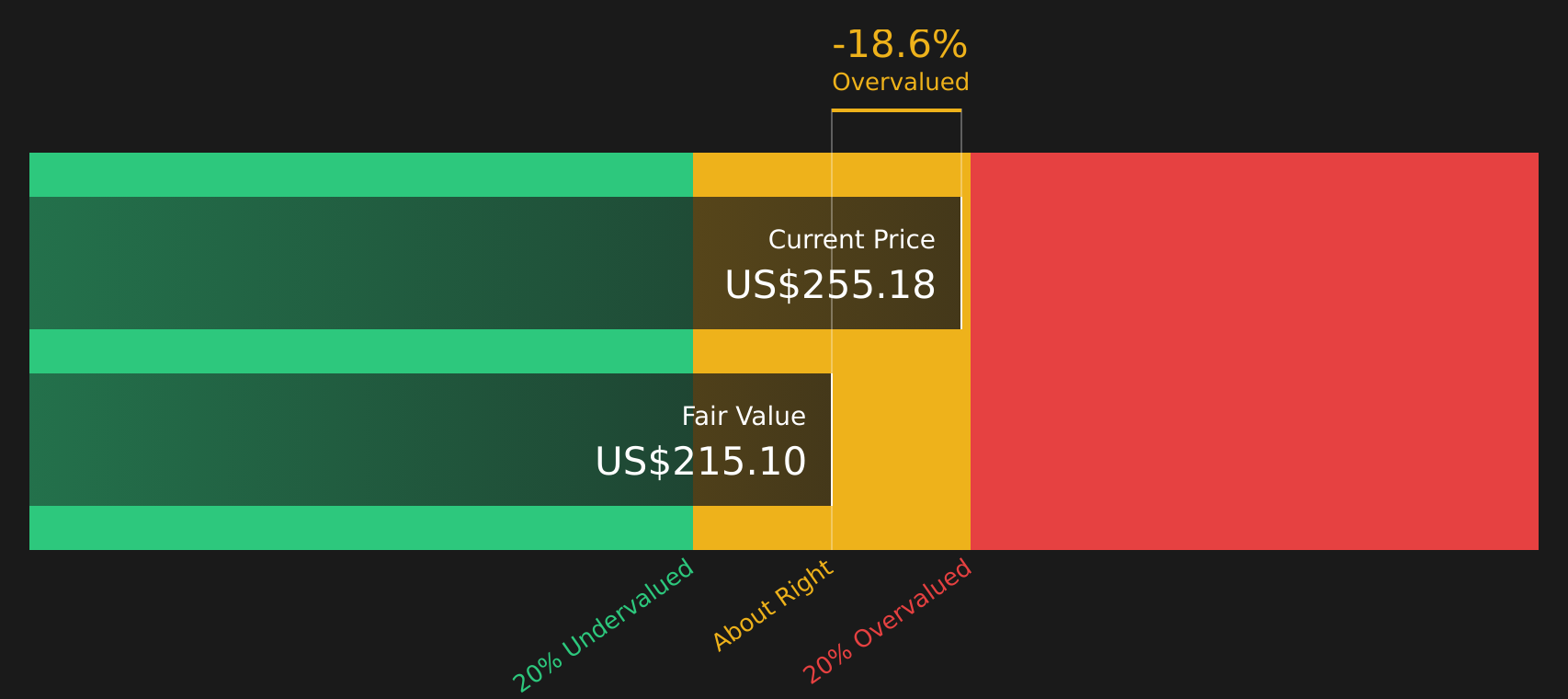

Most Popular Narrative: 35.6% Overvalued

According to Vestra’s narrative, FTAI Aviation’s fair value of $177.38 sits well below the recent $240.49 share price, putting a clear valuation gap on the table for investors to weigh.

The core of the FTAI thesis lies in its Dominant Aftermarket Position. With over 22,000 CFM56 engines in the global fleet and new engine models like the LEAP facing durability issues, the aviation industry is forced to keep older planes flying longer. This creates a "permanent tailwind" for FTAI’s MRE business. By owning the engines, the parts, and the repair shops (including the newly acquired Rome facility), FTAI captures the entire value chain. This "vertical integration" allows them to offer airlines a 20-30% cost saving compared to traditional manufacturers, making them a primary beneficiary of the current global shortage of aircraft engines.

Want to see what sits behind that premium to Vestra’s fair value? The narrative hangs on aggressive earnings expansion, heavier investment, and a future profit multiple more often linked to high growth energy tech names.

Result: Fair Value of $177.38 (OVERVALUED)

However, there are pressure points here, including execution risk around the FTAI Power rollout and the cash impact of heavy inventory and capital commitments.

Another View: Market Pricing Versus Growth Profile

Vestra’s fair value of $177.38 uses a forward P/E approach and indicates that FTAI Aviation is 35.6% overvalued. In contrast, Simply Wall St’s model presents a very different picture. Our DCF model estimates a future cash flow value of $409.27, which is above the current $240.49 share price.

This difference presents two distinct interpretations. One highlights valuation risk, while the other suggests a possible discount. The key question is which set of assumptions you find more suitable for your own framework.

Next Steps

With such a mixed set of views in play, it helps to move quickly, review the numbers for yourself, and decide where you stand with FTAI Aviation’s 4 key rewards and 3 important warning signs

Looking for more investment ideas?

If FTAI has sharpened your focus, do not stop here. Widen your net with a few targeted stock ideas that could help shape your next move.

- Target quality at a discount by checking out 49 high quality undervalued stocks that pair solid fundamentals with pricing that may appeal to value focused investors.

- Build income potential into your watchlist by scanning 15 dividend fortresses that emphasise higher yields with supporting fundamentals.

- Sleep easier at night by assessing 73 resilient stocks with low risk scores that score well on resilience and financial strength.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.