Assessing FTI Consulting After a 29% Price Drop and Soft Q1 Outlook for 2025

FTI Consulting, Inc. FCN | 176.77 | +1.67% |

If you find yourself asking whether it is the right time to make a move on FTI Consulting stock, you are not alone. This is a stock that keeps investors guessing, especially after a year that has seen its price decline by 29.0%. Short-term moves have not offered relief either, with a dip of 0.9% over the past week and a 4.7% slide in the last month. Year to date, FTI Consulting is down 15.7%, sending mixed signals about where it is headed next. Looking further back, the five-year return stands at an impressive 42.6%, a testament to the company’s long-term potential.

The market’s evolving view of professional services stocks like FTI Consulting is certainly playing a role here. Investors are adjusting their risk appetite, perhaps responding to global economic uncertainties and shifting demand for consulting expertise. These forces could help explain some of the recent volatility, though nothing major has hit headlines in a way that might radically shift fundamentals.

What about the company’s valuation? According to our scorecard, FTI Consulting earns a value score of 3 out of 6, meaning it appears undervalued in half of the standard checks we perform. That is not an all-clear signal, but it is definitely a reason to pause and dig deeper.

In the next section, we will break down the methods behind this valuation score. Stick around until the end, where we will also reveal a stronger, more nuanced way to decide if FTI Consulting’s current price is a true bargain.

Approach 1: FTI Consulting Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates what a company is worth today based on projections of its future cash flows. These projections are then discounted back to reflect their present value. This approach considers both current performance and reasonable assumptions about future growth or decline.

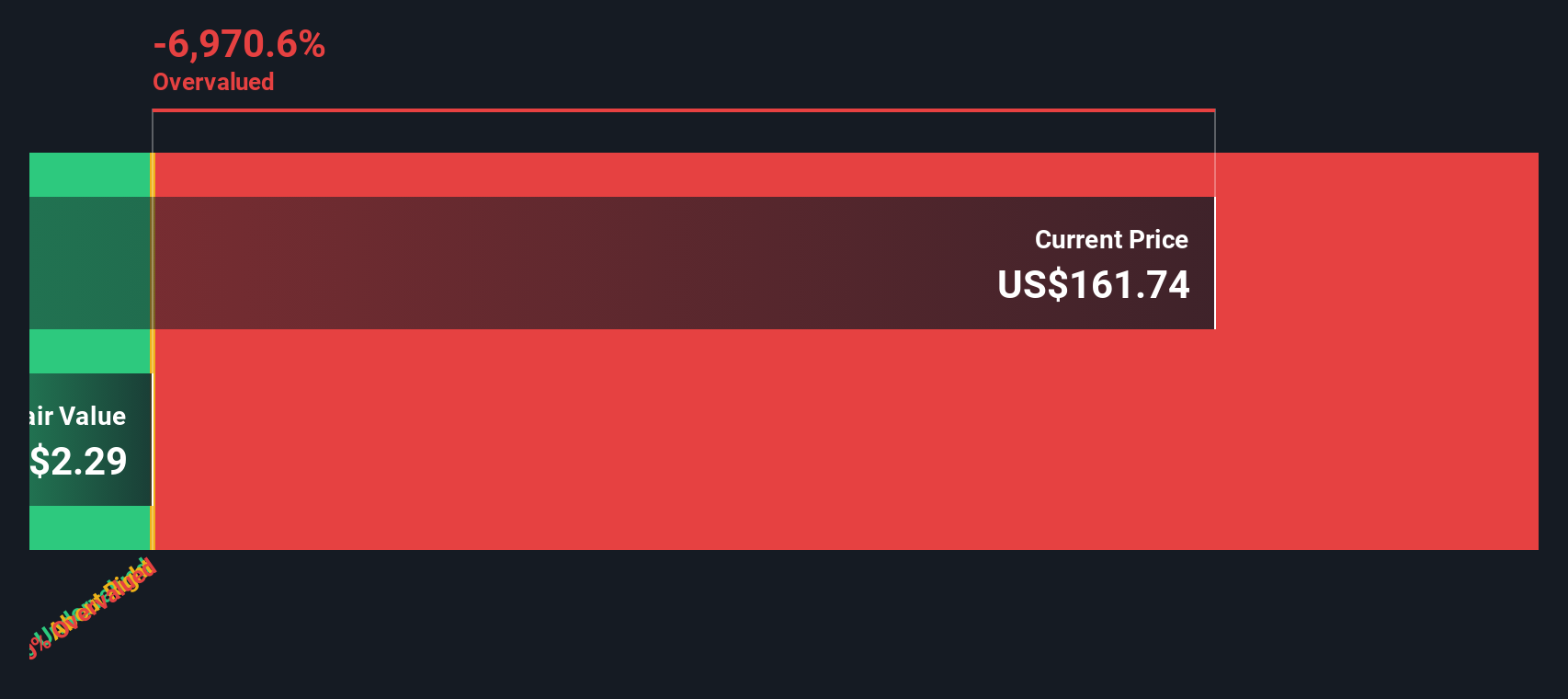

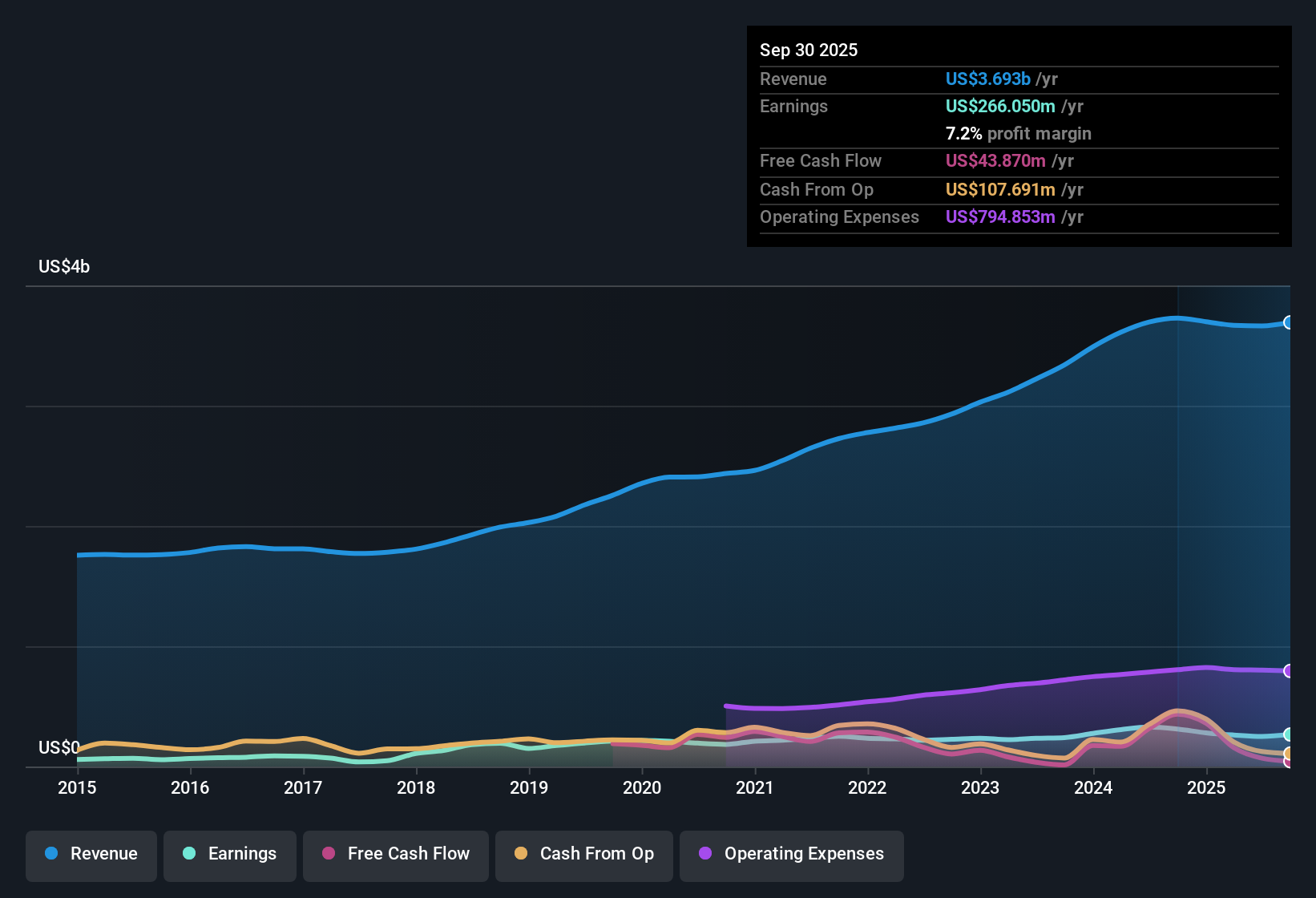

For FTI Consulting, the most recent Free Cash Flow stands at $74.0 Million. According to the two-stage DCF model, cash flows are expected to decline over the next decade, reaching approximately $2.6 Million by 2035. It is important to note that while analysts typically provide estimates for up to five years, projections past this point are extrapolated based on available trends and historical performance data.

Applying this DCF valuation, the calculated intrinsic value of FTI Consulting is $2.30 per share. When compared to the current share price, the stock trades at a hefty 6869.3% premium to this estimated fair value. This indicates that, based on projected cash flows, FTI Consulting is dramatically overvalued by this measure.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests FTI Consulting may be overvalued by 6869.3%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: FTI Consulting Price vs Earnings

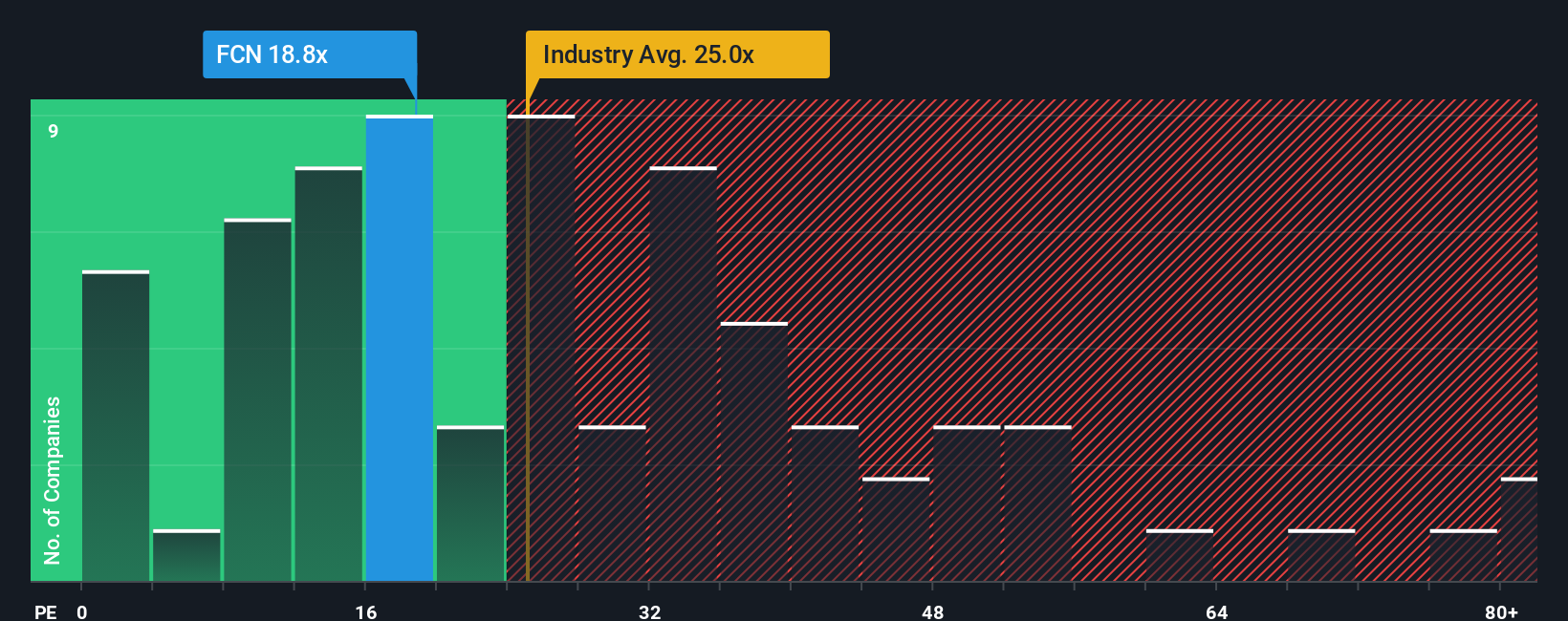

For companies like FTI Consulting that are profitable, the Price-to-Earnings (PE) ratio is widely recognized as a practical yardstick for assessing valuation. The PE ratio reflects how much investors are willing to pay for each dollar of the company's earnings, which is especially useful for understanding market confidence in established businesses with consistent profitability.

What counts as a “normal” or “fair” PE ratio depends a lot on expected future growth and perceived risk. Higher-growth companies or those with stable, predictable earnings tend to fetch premium multiples. On the other hand, companies with lower growth prospects or higher risk profiles typically trade at a discount relative to industry averages.

FTI Consulting currently trades at a PE multiple of 20.3x. This is below both the industry average of 26.8x and the peer average of 45.3x, suggesting a more modest market expectation. However, looking beyond these broad benchmarks, Simply Wall St calculates a Fair Ratio of 25.2x for FTI Consulting. The Fair Ratio is a proprietary metric tailored to each company and factors in its specific earnings growth, profit margins, risks, industry dynamics, and market capitalization. Because it is personalized, the Fair Ratio usually provides a more accurate reflection of justified value than the blunt instrument of peer or industry averages.

In this case, FTI Consulting’s current PE ratio is modestly below its Fair Ratio. The gap is more than 0.10, which signals the market may be undervaluing the stock based on the company’s fundamentals and prospects.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your FTI Consulting Narrative

Earlier we mentioned that there's an even better way to understand valuation. Let's introduce you to Narratives, a tool designed to link your unique perspective on a company directly to its financial forecasts and fair value. This approach gives your investments a story to stand behind.

A Narrative is simply your view of a company's future, which you translate into assumptions about its revenue, earnings, and margins; these in turn create your own fair value estimate reflecting your outlook.

By connecting story, forecasts, and valuation, Narratives empower you to make buy or sell decisions confidently based on how your Fair Value compares to the current market price.

This approach is simple to use and always evolving. Within Simply Wall St's Community page, millions of investors create and update their Narratives as soon as news or earnings data changes, keeping their views fresh and relevant.

For example, some investors believe that FTI Consulting's global expansion and regulatory tailwinds will lift revenue and margins well above consensus, leading them to set a Fair Value near $185 per share. Others see rising automation and competition as threats that justify a much lower Fair Value closer to $167.

Do you think there's more to the story for FTI Consulting? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.